Vietnam: PIT finalization declaration form (Form No. 05/QTT-TNCN) applicable to the latest salary and wage payer?

- What is the PIT finalization declaration form applicable to entities paying taxable income from wages and wages according to the latest Vietnam regulations?

- Do the subjects paying wages and wages have to make PIT finalization for employees or not in Vietnam?

- What does the PIT finalization dossier for organizations and individuals paying wages and wages include in Vietnam?

What is the PIT finalization declaration form applicable to entities paying taxable income from wages and wages according to the latest Vietnam regulations?

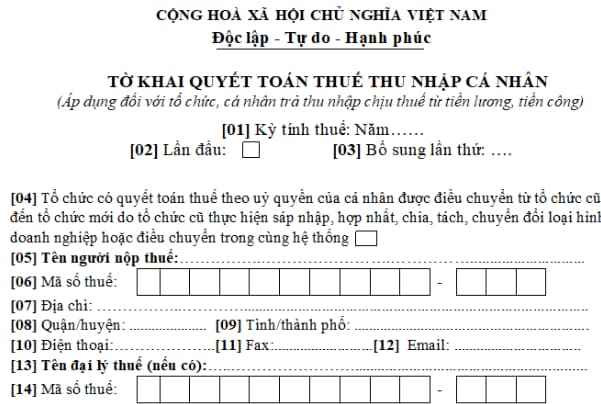

Currently, the Personal Income Tax Finalization Form (applicable to organizations and individuals paying taxable income from wages and wages) is specified in Form No. 05/QTT-TNCN issued together with Circular 80/2021/TT-BTC, as follows:

Download the Personal Income Tax Finalization Form (applicable to organizations and individuals paying taxable income from wages and wages): here

Vietnam: PIT finalization declaration form (Form No. 05/QTT-TNCN) applicable to the latest salary and wage payer?

Do the subjects paying wages and wages have to make PIT finalization for employees or not in Vietnam?

Pursuant to the provisions of Point d Clause 6 Article 8 of Decree 126/2020/ND-CP stipulates:

Article 8. Taxes declared monthly, quarterly, annually, separately; tax finalization

…

6. The following taxes and amounts shall be declared annually and finalized when an enterprise is dissolved, shuts down, terminates a contract or undergoes rearrangement. In case of conversion (except equitized state-owned enterprises) where the enterprise after conversion inherits all tax obligations of the enterprise before conversion, tax shall be finalized at the end of the year instead of the issuance date of the decision on conversion. Tax shall be finalized at the end of the year):

…

d) Personal income tax for salary payers; salary earners that authorize salary payers to finalize tax on their behalf; salary earners that finalize tax themselves. To be specific:

d.1) Salary payers shall finalize tax on behalf of authorizing individuals, whether tax is deducted or not. Tax finalization is not required if an individual does not earn any income. In case an employee is re-assigned to a new organization after the old organization is acquired, consolidated, divided or converted, or to a new organization that is in the same system as the old organization, the new organization shall finalize tax as authorized by such employee, including the income paid by the old organization, and collect documents about deduction of personal income tax issued by the old organization to the employee (if any).

Thus, currently, the following subjects must finalize PIT including: organizations and individuals paying wages and wages; authorize PIT finalization and individuals directly settle with tax authorities.

In particular, organizations and individuals paying income from wages and wages are responsible for declaring tax finalization and finalization on behalf of authorized individuals paid by income-paying organizations and individuals, regardless of whether tax deductions arise or not.

What does the PIT finalization dossier for organizations and individuals paying wages and wages include in Vietnam?

Pursuant to Clause b of Subsection 9.9 Section 9 of Appendix I promulgated together with Decree 126/2020/ND-CP, PIT finalization dossiers for organizations and individuals paying wages and wages include

- PIT calculation theory declaration according to form 05/QTT-TNCN.

- Appendix of detailed list of individuals subject to tax according to the progressive schedule of each section according to form No. 05-1/BK-QTT-TNCN.

- Appendix of personal details subject to tax at the full tax rate according to form No. 05-2/BK-QTT-TNCN.

- Appendix detailing dependents of family deduction according to form No. 05-3/BK-QTT-TNCN.

LawNet