What is the ranking of the Vietnam National Football Team after the Victory at the AFF Cup? Is the 33-billion VND reward for Vietnam National Football Team taxable?

What is the ranking of the Vietnam National Football Team after the Victory at the AFF Cup?

After the historic victory at the AFF Cup 2024, the Vietnam national football team has risen to the 112th position on the FIFA rankings. This is an important step forward, marking a significant development of Vietnamese football on the international stage.

According to Football Rankings, solely the victory in the second leg of the finals helped the Vietnam national football team gain an additional 2.77 points on the FIFA rankings. Summarizing the AFF Cup 2024 campaign, the Vietnam team earned a total of 10.22 points, ascending to the 112th position globally. The rankings will be officially announced by FIFA on its homepage in the upcoming days.

When FIFA publishes the official rankings in February 2025, the Vietnam team could continue to improve their ranking if the opponents positioned above them lose points due to poor performance.

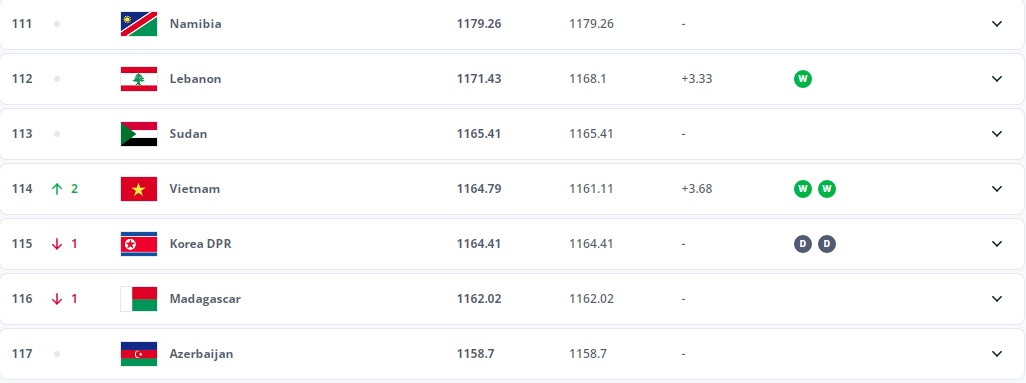

Below is the ranking of the Vietnam national football team as announced on the FIFA homepage in December 2024:

Ranking of the Vietnam national football team in December 2024

See the detailed ranking of the Vietnam national football team on the official FIFA homepage: https://inside.fifa.com/fifa-world-ranking/men

Note: Information is for reference only!

What is the ranking of the Vietnam National Football Team after the Victory at the AFF Cup? (Image from Internet)

Is the 33-billion VND reward for Vietnam National Football Team taxable?

The 33-billion VND reward of the Vietnam national team will include various amounts from different sources such as rewards from the tournament for the championship title; rewards from organizations, individuals for the team or individual players, etc. Accordingly, the personal income tax (PIT) computation for these types of rewards is as follows:

(1) Rewards from national and international competitions recognized by the Vietnamese government:

According to point e, clause 2, Article 2 of Circular 111/2013/TT-BTC, regulations on taxable income for PIT are as follows:

Taxable Income

...

- Income from wages and salaries

...

e) Cash rewards or non-cash rewards in all forms, including rewards in securities, except for the following rewards:

e.1) Rewards accompanying titles bestowed by the State, including rewards accompanying emulation titles, awards according to the law on emulation and commendation, specifically:

e.1.1) Rewards accompanying emulation titles such as National Emulation Soldier; Emulation Soldier of Ministry, central agencies, unions, provinces, cities directly under central authority; basic level Emulation Soldier, Advanced Laborer, Advanced Soldier.

e.1.2) Rewards accompanying forms of commendation.

e.1.3) Rewards accompanying titles bestowed by the State.

e.1.4) Rewards accompanying awards from associations, organizations belonging to political organizations, political-social organizations, social organizations, social-professional organizations of central authority and local government awarded in accordance with their statutes and laws on emulation and commendation.

e.1.5) Rewards accompanying the Ho Chi Minh Prize, the State Prize.

e.1.6) Rewards accompanying commemorative medals, badges.

e.1.7) Rewards accompanying commendation certificates, certificates of merit.

The authority to issue commendation decisions and the amount of money accompanying the emulation titles, commendation forms must comply with the emulation and commendation laws.

e.2) Rewards accompanying national awards, international awards recognized by the Vietnamese government.

e.3) Rewards for technical innovations, inventions recognized by a competent State agency.

e.4) Rewards for discovering and reporting violations of the law to a competent State agency.

...

Thus, the Vietnam national football team, when participating in the national level tournament AFF Cup 2024 and achieving the championship title, the rewards accompanying titles, medals are considered rewards accompanying national awards, international awards recognized by the Vietnamese government. Therefore, the rewards that the Vietnam national football team receives along with the championship title, medals will not be subject to personal income tax.

Additionally, the General Department of Taxation issued Official Dispatch 1324/TCT-TNCN in 2018 regarding personal income tax on other rewards received by the Vietnam national football team. Specifically as follows:

(2) Rewards from other organizations, individuals:

For rewards from other organizations, individuals such as rewards from economic corporations, banks, businesses, organizations or individuals for the team or individual players, coaches, if considered as wages, salaries or implemented under financial regulations on expenses and rewards of the Vietnam Football Federation, it will be counted as taxable personal income as regulated in clause 10, Article 2 of Circular 111/2013/TT-BTC.

Furthermore, according to Official Dispatch 1324/TCT-TNCN in 2018, the General Department of Taxation also states that tax deductions will be implemented according to the partially progressive tax scale or 10% deduction for income from 2 million VND/occasion and above, depending on the labor contract of the players, coaches, and team members. At the end of the year, individuals will complete tax finalization according to regulations.

(3) Gifts that are assets requiring registration of ownership or use:

If an individual receives a gift in the form of securities, capital shares in economic organizations, real estate or other assets requiring registration of ownership, use rights, they must pay personal income tax on the income from receiving gifts as per clause 10, Article 2 of Circular 111/2013/TT-BTC of the Ministry of Finance and implement tax calculations, declarations, and payment according to Article 16 of Circular 111/2013/TT-BTC and clause 6, Article 16 of Circular 156/2013/TT-BTC of the Ministry of Finance.

Thus, the payment of personal income tax on the total 33-billion reward of the Vietnam national football team depends on the source and nature of the received rewards.

What are regulations on personal income tax period in Vietnam?

Based on Article 7 of the Law on Personal Income Tax 2007 as amended by clause 3, Article 1 of the Amended Law on Personal Income Tax 2012, the personal income tax period is regulated as follows:

- For resident individuals, the period is regulated as follows:

+ The yearly tax period applies to income from business; income from wages and salaries;

+ The tax period per occurrence of income applies to income from capital investment; income from capital transfer, except for income from securities transfer; income from real estate transfer; income from winning prizes; income from royalties; income from franchise; income from inheritance; income from gifts;

+ The tax period per transaction or annually for income from securities transfer.

- For non-resident individuals, the tax period is per occurrence of income for all taxable income.