What is the payment table for consignment goods in Vietnam according to Circular 200? Does a business entity with commission revenue from agency activities have to pay VAT in Vietnam?

What is the payment table for consignment goods in Vietnam according to Circular 200?

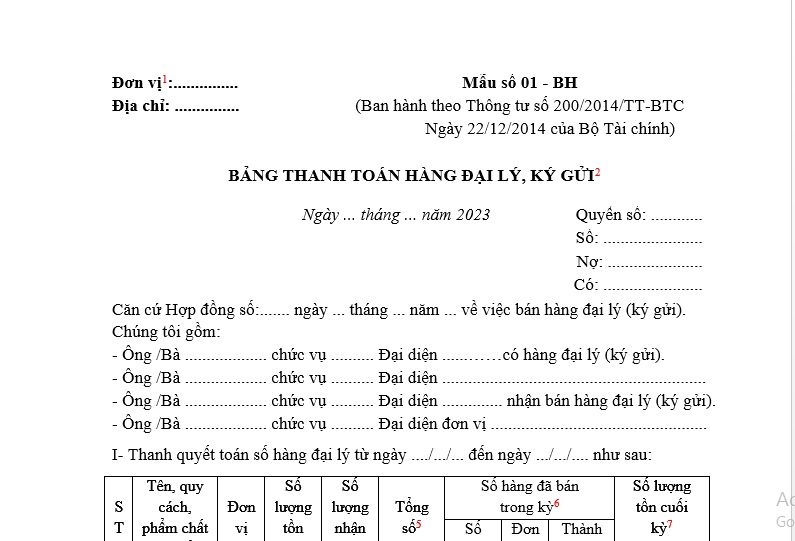

The payment table for consignment goods is applied according to Form No. 01-BH issued with Circular 200/2014/TT-BTC.

Form No. 01-BH Payment Table for Consignment Goods according to Circular 200 is structured as follows:

Form No. 01-BH Payment Table for Consignment Goods according to Circular 200... Download

Below is the guidance on filling out Form No. 01-BH Payment Table for Consignment Goods according to Circular 200:

(1) Clearly record the name, address, or stamp of the enterprise receiving consignment goods using this table.

(2) - The payment table for consignment goods reflects the payment status of consignment goods between the enterprise with the goods and the enterprise receiving the consignment goods, acting as a document for payment and accounting records.

- The payment table for consignment goods is made in triplicate by the party receiving the consignment. After completion, the drafter signs and submits for review to the chief accountants of both parties and for approval by the directors of both sides, with one copy retained at the point of creation (planning department or supply department), one copy kept in the accounting department for payment and accounting records, and one copy sent to the consigning party.

(3) Record the quantity of goods remaining at the end of the previous period.

(4) Record the quantity of consignment goods received this period.

(5) Record the total quantity of consignment goods received up to the end of this period, including unsold goods from the previous period and goods received this period (column 3 = column 1 + column 2).

(6) Record the quantity, unit price, and amount of goods sold that must be settled this period. The settlement price is the price stated in the consignment sales contract between the consigning and receiving parties.

(7) Record the quantity of unsold consignment goods (at counters or warehouses) as of the payment table dates (column 7 = column 3 – column 4).

(8) Record the total payable amount generated this period.

(9) Record the amount owed by the consignment sales party to the consigning party at the time of this settlement.

(10) Record the amount the consignment sales party must settle with the consigning party generated up to this period (Section III = Section II + column 6 of Section I).

(11) Record the amount the consigning party must settle with the consignment sales party for taxes paid on behalf, commissions, other expenses, ...(if any).

(12) Record the amount the consignment sales party pays to the consigning party this period (clearly stating cash and check amounts).

(13) Record the amount still owed by the consignment sales party to the consigning party at the time of settlement (Section VI = Section III - Section IV - Section V).

What is the payment table for consignment goods in Vietnam according to Circular 200? (Image from Internet)

Does a business entity with commission revenue from agency activities have to pay VAT in Vietnam?

According to point 7 Article 5 of Circular 219/2013/TT-BTC (supplemented by point 1 Article 3 of Circular 119/2014/TT-BTC and Article 1 of Circular 193/2015/TT-BTC) regulations on cases not required to declare and pay VAT are as follows:

Cases not required to declare and pay VAT

...

- Other cases:

A business entity is not required to declare and pay tax in the following cases:

...

đ) Revenue from goods and services sold through agency and commission received from agency activities at the agreed price between the agency and the principal in postal, telecommunications, lottery ticket sales, airline ticket sales, cars, trains, ships; international transport agencies; agencies in the aviation and maritime sectors that are subject to a 0% VAT rate; insurance agency sales.

e) Revenue from goods, services, and agency commission from agency activities for selling goods and services not subject to VAT

...

In addition, according to Official Dispatch 70307/CTHN-TTHT of 2023 the Hanoi Tax Department provides guidance on VAT declaration and payment as follows:

In the case that a Company has commission revenue from agency activities at the agreed price between the agency and the principal in postal, telecommunications services, it falls under the cases not required to declare and pay tax as prescribed at Clause 7 Article 5 of Circular 219/2013/TT-BTC.

Thus, if a business entity earns commission revenue from agency activities at the agreed price between the agency and the principal in postal, telecommunications services, it is not required to pay VAT.

From July 01, 2025, when is the time to determine VAT for services in Vietnam?

Based on Clause 1 Article 8 of the Law on Value-Added Tax 2024 regarding the time to determine VAT as follows:

Time to determine value-added tax

- The time to determine value-added tax is regulated as follows:

a) For goods, it is the time of transfer of ownership or right to use the goods to the buyer or the time of invoice issuance, regardless of whether the money has been collected.

b) For services, it is the time of completion of service provision or the time of issuing service provision invoices, regardless of whether the money has been collected.

...

Therefore, the time to determine VAT for services is the time of completion of service provision or the time of issuing service provision invoices, regardless of whether the money has been collected.