What is the List for diplomatic agents eligible for VAT refund in Vietnam (Form No. 01-3b/HT)?

Who is a diplomatic agent?

Pursuant to the provisions of Article 1 Vienna Convention of April 19, 1961 on Diplomatic Relations, a diplomatic agents is explained as the head of a representative agency or a diplomatic agent of the representative agency.

What is the List for diplomatic agents eligible for VAT refund in Vietnam (Form No. 01-3b/HT)? (Image from the Internet)

Vietnam: What documents must be prepared to apply for a VAT refund for individuals eligible for diplomatic immunity?

Pursuant to the provisions of Article 28 Circular 80/2021/TT-BTC (amended by Article 2 Circular 13/2023/TT-BTC), the dossier for applying for a VAT refund for individuals eligible for diplomatic immunity includes the following components:

VAT Refund Application Dossier

The VAT refund application dossier as per the tax law (excluding cases of VAT refund under an international treaty or uncredited input VAT upon ownership transfer, corporate conversion, merger, consolidation, division, separation, dissolution, bankruptcy, termination of activities as per Articles 30 and 31 of this Circular) includes:

1. A request for reimbursement from the state budget using form No. 01/HT issued with Appendix I of this Circular.

2. Related documents according to the refund case. Specifically:

a) In case of a tax refund for investment projects:

a.1) A copy of the Investment Registration Certificate or Investment Certificate or Investment License in cases requiring the procedure to obtain an investment registration certificate;

a.2) For projects with construction works: A copy of the Land Use Rights Certificate or land allocation decision or land lease contract from the competent authority; construction permit;

a.3) A copy of the charter capital contribution documents;

a.4) For investments in business sectors and trades subject to conditions during the investment phase, as stipulated by investment laws, specialized laws where the competent state authority has issued the business license for conditional business lines as per Clause 3 Article 1 of Decree No. 49/2022/ND-CP dated July 29, 2022, of the Government of Vietnam: A copy of one of the licenses or certificates or written confirmation/approval for conditional business lines.

...

e) In the case of a VAT refund for diplomatic immunity:

e.1) A list of VAT on goods and services purchased for use by the diplomatic representative agency as per form No. 01-3a/HT issued with Appendix I of this Circular, confirmed by the State Protocol Department under the Ministry of Foreign Affairs that the input costs are eligible for diplomatic exemption status to qualify for a refund.

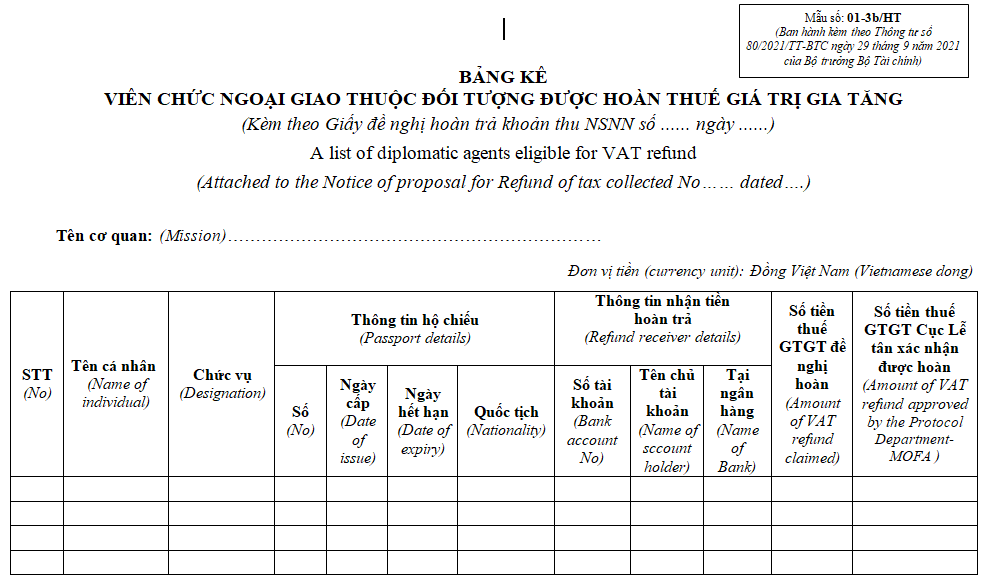

e.2) A list of VAT Refund-Eligible diplomatic agents as per form No. 01-3b/HT issued with Appendix I of this Circular.

g) Refund for commercial banks appointed as VAT refund agents for departing clients:

A list of VAT refund receipts for foreigners exiting the country as per form No. 01-4/HT issued with Appendix I of this Circular.

h) In case of VAT refund by decision of a competent authority according to law: Decision of the competent authority.

Thus, the dossier for applying for a VAT refund for individuals eligible for diplomatic immunity includes the following components:

- A list of VAT on goods and services purchased for use by the diplomatic representative agency according to Form No. 01-3a/HT issued with Appendix I Circular 80/2021/TT-BTC, confirmed by the State Protocol Department under the Ministry of Foreign Affairs regarding the applicability of diplomatic exemption for reimbursement.

- A list of VAT Refund-Eligible diplomatic agents according to Form No. 01-3b/HT issued with Appendix I Circular 80/2021/TT-BTC.

What is the List for diplomatic agents eligible for VAT refund in Vietnam (Form No. 01-3b/HT)?

The Sample List for diplomatic agents eligible for VAT refund is implemented according to Form No. 01-3b/HT issued with Appendix I Circular 80/2021/TT-BTC.

DOWNLOAD >>> Sample List for diplomatic agents eligible for VAT refund (Form No. 01-3b/HT)

Moreover, according to Official Dispatch 7108/BTC-TCT of 2022 regarding VAT refunds for individuals eligible for diplomatic immunity, it is instructed regarding the declaration of the "List of VAT Refund-Eligible diplomatic agents" as follows:

The Ministry of Foreign Affairs (State Protocol Department) is requested to guide diplomatic representative agencies to declare information on diplomatic or official identification cards in the "Passport Information" column when making declarations for the "List of VAT Refund-Eligible diplomatic agents" (Form No. 01-3b/HT) issued with Appendix 1 Circular 80/2021/TT-BTC.