What is the latest Import and Export Tariff Schedule of Vietnam 2024? Who are the subjects of application of Decree 26 on Import and Export Tariff of Vietnam?

What is the latest Import and Export Tariff Schedule of Vietnam 2024?

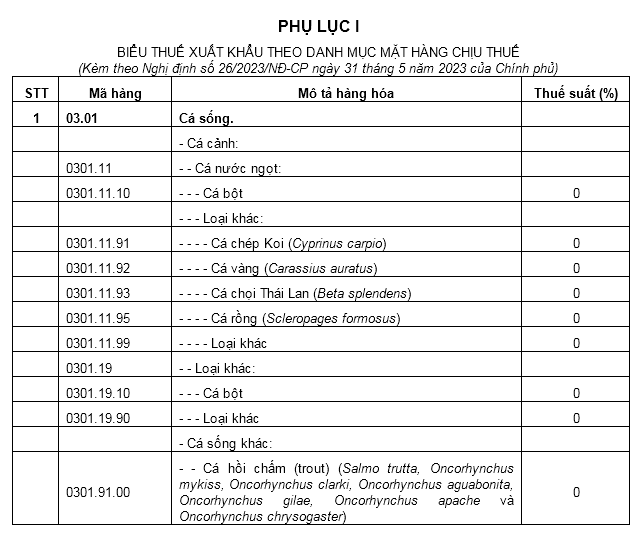

According to Appendix 1 issued together with Decree 26/2023/ND-CP, it includes the commodity code (item code), description of goods, and export tax rates specified for each group of goods and goods subject to export tax.

In case exported goods are not listed in the Export Tariff, the customs declarant shall declare the corresponding 8-digit code of the exported goods according to the preferential import tariff provided in Section 1 of Appendix 2 issued together with Decree 26/2023/ND-CP and is not required to declare the tax rate on the export goods declaration form.

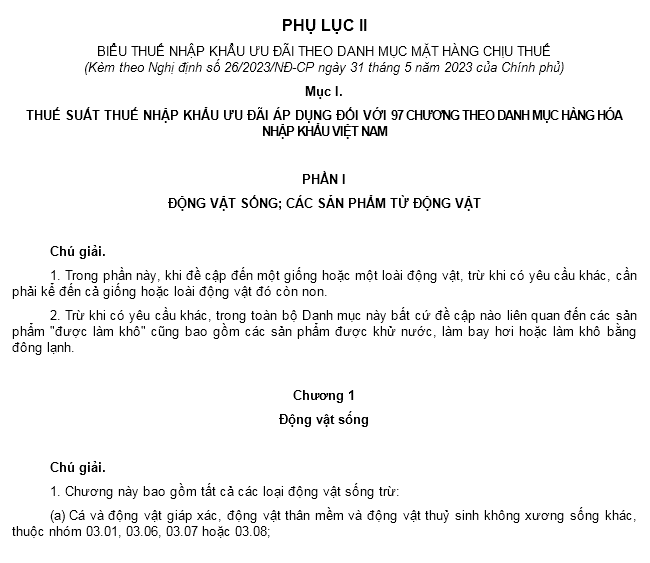

According to Appendix 2 issued together with Decree 26/2023/ND-CP, it includes:

- Section 1: Regulations on preferential import tax rates for 97 chapters according to the Vietnam Export and Import Commodity List.

- Section 2: Lists of goods and preferential import tax rates for certain Goods under Chapter 98 as follows:

>>> Download Complete Excel File of Schedule of Import and Export Tariffs 2024.

*Note: The complete Excel file of the Schedule of Import and Export Tariffs 2024 is for reference purposes only./.

What is the latest Import and Export Tariff Schedule of Vietnam 2024? Who are the subjects of application of Decree 26 on Import and Export Tariff of Vietnam? (Image from the Internet)

Who are the subjects of application of Decree 26 on Import and Export Tariff of Vietnam?

Based on Article 2 of Decree 26/2023/ND-CP, the subjects of application of Decree 26 on Import and Export Tariff are:

[1] Taxpayers as prescribed by the Law on Export and Import Tax.

[2] Customs authorities, customs officials.

[3] Organizations and individuals with rights and obligations related to exported and imported goods.

How is the Export Tariff according to the List of Taxable Goods under Decree 26?

Based on Article 4 of Decree 26/2023/ND-CP, the export tariff according to the List of Taxable Goods under Decree 26 is as follows:

- The export tariff according to the List of Taxable Goods specified in Appendix I issued together with this Decree includes the commodity code (item code), description of goods, and export tax rates specified for each group of goods and goods subject to export tax.

In case exported goods are not listed in the Export Tariff, the customs declarant shall declare the corresponding 8-digit code of the exported goods according to the preferential import tariff provided in Section I of Appendix II issued together with this Decree and is not required to declare the tax rate on the export goods declaration form.

- Export Goods in group with STT 211 in the Export Tariff meet both of the following conditions:

+ Condition 1: Materials, raw materials, and semi-finished products (collectively referred to as goods) not belonging to the groups with STT from 01 to STT 210 in the Export Tariff.

+ Condition 2: Directly processed from the main material being natural resources and minerals with the total value of natural resources, minerals plus energy costs accounting for 51% or more of the production cost of the product.

The determination of the total value of natural resources, minerals plus energy costs accounting for 51% or more of the production cost of the product is implemented in accordance with Decree 100/2016/ND-CP (if applicable).

Exported goods under the exclusion cases stipulated in Clause 1, Article 1 of Decree 146/2017/ND-CP are not included in group with STT 211 of the Export Tariff issued together with this Decree.

- Codes and export tax rates for Goods in group with serial number 211:

For Goods detailed by 8-digit codes and goods descriptions of groups 25.23, 27.06, 27.07, 27.08, 68.01, 68.02, 68.03 at STT 211 of the Export Tariff, the customs declarant declares the export tax rate corresponding to that item code specified at STT 211.

In cases where the export tax rate is not declared as prescribed for the group with STT 211, the taxpayer must submit a List of the Proportion of Values of Natural Resources, Minerals plus Energy Costs in the Cost of Goods production according to Form No. 14 in Appendix II issued with this Decree at the time of customs clearance to prove that the declared goods have a total value of natural resources, minerals plus energy costs less than 51% of the production cost.

In cases where the taxpayer is a trading enterprise purchasing goods from a manufacturing enterprise or another trading enterprise for export, but does not declare the export tax rate as prescribed for the group with STT 211, the taxpayer bases the declaration on the information provided by the manufacturing enterprise according to Form No. 14 in Appendix II mentioned above to prove the ratio of natural resources, minerals plus energy costs under 51% of the product's cost. The taxpayer is responsible before the law for the accuracy of the declaration.

For export Goods in the group with STT 211 but not yet specifically detailed by 8-digit codes and meeting the conditions specified in Clause 2 of this Article, the customs declarant declares exported goods according to the 8-digit code specified in Section I of Appendix II about the preferential import tariff issued together with this Decree and declares the export tax rate as 5%.