What is the duty-free allowance book template - Template No. 02h1 applicable to diplomatic organizations in Vietnam?

What is the duty-free allowance book template - Template No. 02h1 applicable to diplomatic organizations in Vietnam?

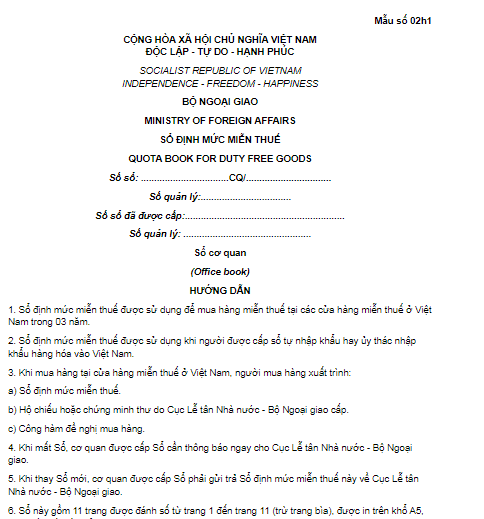

Under Appendix 7 of the forms/templates for tax exemption, tax reduction, tax refund, and non-taxation issued together with Decree 18/2021/ND-CP, the duty-free allowance book template - Template No. 02h1 applicable to diplomatic organizations in Vietnam is specified as follows:

Download the duty-free allowance book template - Template No. 02h1 applicable to diplomatic organizations in Vietnam

What is the duty-free allowance book template - Template No. 02h1 applicable to diplomatic organizations in Vietnam? (Image from the Internet)

What are the procedures for issuing a duty-free allowance book in Vietnam?

Under Clause 8, Article 5 of Decree 134/2016/ND-CP, the procedures for issuing a duty-free allowance book are in Vietnam as follows:

Procedures for issuance of duty-free allowance book or increase of allowance therein

- Application submitted by an organization shall include the following documents:

The written request for issuance of the issuance of the duty-free allowance book or allowance increase (Form No. 01 or Form No. 01a in Appendix VII hereof: 01 original copy;

Notice of the establishment of the representative agency in Vietnam after the duty-free allowance book is issued for the first time: 01 photocopy;

Documents proving completion of re-export, destruction or transfer of the goods in case the entity specified in Point a, Point b Clause 1 of this Article requests additional allowance on automobiles or motorcycles to the duty-free allowance book: 01 photocopy;

The international treaty or agreement between Vietnam’s government and the foreign non-governmental organization which specifies the categories and allowance on duty-free goods: 01 photocopy;

The Prime Minister’s decision on duty exemption if the international treaty or agreement between Vietnam’s government and the foreign non-governmental organization does not specify the categories and allowance on duty-free goods (for the organizations specified in Point c, Point d Clause 1 of this Article): 01 photocopy.

- Application submitted by an individual shall include the following documents:

The written request for issuance of the issuance of the duty-free allowance book or allowance increase (Form No. 02 or Form No 02i in Appendix VII hereof: 01 original copy;

The ID card issued by the Ministry of Foreign Affairs (for the individuals specified in Point a, Point b Clause 1 of this Article: 01 photocopy;

Documents proving completion of re-export, destruction or transfer of the goods in case the entity specified in Point a, Point b Clause 1 of this Article requests additional allowance for automobiles or motorcycles to the duty-free allowance book: 01 photocopy;

The work permit or a legally equivalent document issued by a competent authority if the applicant is a member of an international organization or non-governmental organization (for persons mentioned in Point d Clause 1 of this Article): 01 photocopy;

The international treaty or agreement between Vietnam’s government and the foreign non-governmental organization which specifies the categories and allowance on duty-free goods: 01 photocopy;

The Prime Minister’s decision on duty exemption if the international treaty or agreement between Vietnam’s government and the foreign non-governmental organization does not specify the categories and allowance on duty-free goods (for the entities specified in Point c, Point d Clause 1 of this Article): 01 photocopy.

Which authorities have the power to issue duty-free allowance books in Vietnam?

According to point c of Clause 8 in Article 5 of Decree 134/2016/ND-CP, the procedures for issuing a duty-free allowance book are in Vietnam as follows:

Power to issue the duty-free allowance book or increase allowance therein

Directorate of State Protocol – The Ministry of Foreign Affairs or an agency authorized by the Ministry of Foreign Affairs shall issue duty-free allowance books using Form No. 02h1 or Form No. 02h2 or Form No. 02h3 in pl VII hereof to the entities specified in Point a and Point b Clause 1 of this Article within 05 working days from the day on which adequate documents are received.

Customs Departments of provinces, inter-provinces and central-affiliated cities (hereinafter referred to as “provinces”) where the organizations mentioned in Point c and Point d Clause 1 of this Article are located shall issue duty-free allowance books using Form No. 02h4 or Form No. 02h5 in Appendix VII hereof to the organizations and individuals mentioned in Point c and Point d Clause 1 of this Article within 05 working days from the day on which adequate documents are received.

The Ministry of Foreign Affairs shall monitor and issue duty-free allowance book to the entities granted diplomatic immunity and privileges mentioned in Point c Clause 1 of this Article if they have been issued with duty-free allowance books by the Ministry of Foreign Affairs before the effective date of this Decree.

After a duty-free allowance book is issued, the issuing authority mentioned in this Point shall update General Department of Customs with information in the duty-free allowance book via the National Single-window Information Portal.

Therefore, depending on the authority, the following authorities will have the power to issue the duty-free allowance book:

Directorate of State Protocol – The Ministry of Foreign Affairs or an agency authorized by the Ministry of Foreign Affairs; the Customs Departments of provinces; the Ministry of Foreign Affairs.

- What entities may buy duty-free goods without any restriction in terms of quantity in Vietnam?

- How is the e-tax payment time determined in Vietnam?

- How many times can an e-transaction verification code be used in Vietnam?

- Who is eligible for deadline extension for land rent payment in Vietnam in 2024 under Decree 64?

- What are responsibilities of the tax authority in organizing an electronic tax information system for e-tax transactions in Vietnam?

- Is the chief of the inter-commune tax team a member of the tax advisory council of a commune in Vietnam?

- Cases eligible for deadline extension of terminal tax declaration dossier in Vietnam

- What are the conditions for representatives of household businesses and individual businesses to participate in the tax advisory council of a commune in Vietnam?

- Who is the president of the tax advisory council of a commune in Vietnam?

- Vietnam: May e-tax transactions be carried out at 11 PM?