What is the declaration form for a 2% VAT reduction in Vietnam from January 01, 2025, to June 30, 2025?

What is the declaration form for a 2% VAT reduction in Vietnam from January 01, 2025, to June 30, 2025?

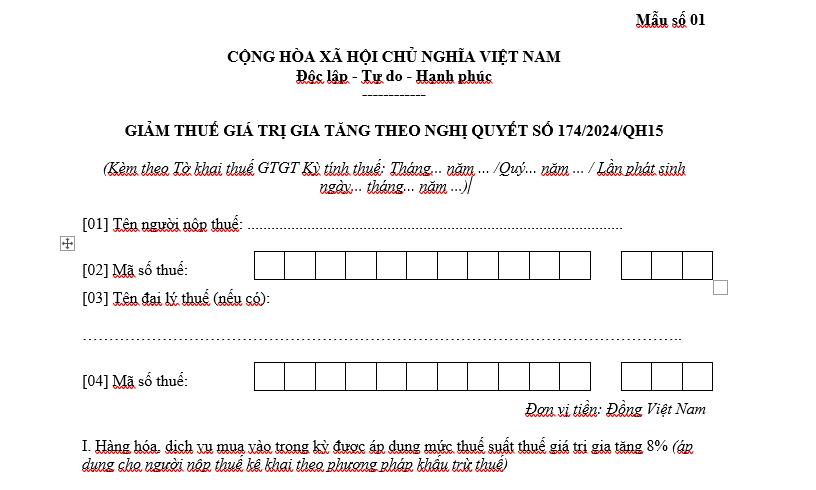

The Declaration form for a 2% VAT reduction from January 01, 2025, to June 30, 2025, is Form No. 01 issued with Decree 180/2024/ND-CP.

The Declaration form for a 2% VAT reduction is as follows:

Download the Declaration form for a 2% VAT reduction from January 01, 2025, to June 30, 2025.

What is the declaration form for a 2% VAT reduction in Vietnam from January 01, 2025, to June 30, 2025? (Image from the Internet)

What types of goods and services are entitled to a 2% VAT reduction in Vietnam according to Decree 180?

Based on Article 1 of Decree 180/2024/ND-CP, the goods and services eligible for VAT reduction for the first six months of 2025 are as follows:

- VAT reduction for groups of goods and services currently applying a 10% tax rate, excluding the following goods and services groups:

+ Telecommunications, financial activities, banking, securities, insurance, real estate businesses, metals and prefabricated metal products, mining products (excluding coal mining), coke, refined petroleum, and chemical products. Details in Appendix 1 issued with Decree 180/2024/ND-CP.

+ Products subject to special consumption tax. Details in Appendix 2 issued with Decree 180/2024/ND-CP.

+ Information technology according to the law on information technology. Details in Appendix 3 issued with Decree 180/2024/ND-CP)

+ The VAT reduction for each type of goods and services stipulated in Clause 1, Article 1 of Decree 180/2024/ND-CP is applied uniformly at the stages of importation, production, processing, and commercial business. For extracted coal sold (including cases where extracted coal is screened, classified through a closed process before being sold), it is subject to VAT reduction. Coal products in Appendix I issued with Decree 180/2024/ND-CP at stages other than extraction and sale are not eligible for VAT reduction.

- Enterprises, economic groups carrying out a closed process to sell extracted coal are also subject to VAT reduction for extracted coal.

- In cases where the goods and services mentioned in Appendices 1, 2, and 3 issued with Decree 180/2024/ND-CP are non-VAT-taxable or subject to a 5% VAT under the Law on Value-Added Tax 2008, the provisions of the law will apply, and no VAT reduction will be granted.

What is the procedure for implementing VAT reduction in Vietnam according to Decree 180?

Based on Clause 3, Article 1 of Decree 180/2024/ND-CP, the procedure for implementing VAT reduction is as follows:

- For business establishments stipulated at Point a, Clause 2, Article 1 of Decree 180/2024/ND-CP, when issuing VAT invoices for goods and services subject to VAT reduction, record “8%” in the VAT rate line; record VAT amount; total amount payable by buyer.

Based on the VAT invoice, the business establishment selling goods and services declares the output VAT, and the purchasing business establishment declares the input VAT deduction according to the reduced tax amount recorded on the VAT invoice.

- For business establishments stipulated at Point b, Clause 2, Article 1 of Decree 180/2024/ND-CP, when issuing sales invoices for goods and services subject to VAT reduction, record the full price before reduction in the "Amount column" and, in the "Total value of goods and services" line, record the amount that has had a 20% percentage point from the revenue reduced, accompanied by the note: "reduced... (amount) corresponding to 20% of the percentage point for calculating VAT according to Resolution No. 174/2024/QH15".

Who is the taxpayer for VAT under current regulations?

According to Article 3 of Circular 219/2013/TT-BTC, VAT taxpayers are defined as follows:

VAT taxpayers are organizations, individuals producing, trading goods, and services subject to VAT in Vietnam, regardless of industry, form, or type of business organization (hereinafter referred to as business establishments) and organizations and individuals importing goods, purchasing services from abroad subject to VAT (hereinafter referred to as importers), including:

- Business organizations established and registered in accordance with the Law on Enterprises, the Law on State Enterprises (now the Law on Enterprises), the Law on Cooperatives, and other specialized business laws;

- Economic organizations of political organizations, socio-political organizations, social organizations, socio-professional organizations, people's armed units, professional organizations, and other organizations;

- Foreign-invested enterprises and foreign parties participating in business cooperation under the Law on Foreign Investment in Vietnam (now the Law on Investment); foreign organizations, individuals doing business in Vietnam but not establishing a legal entity in Vietnam;

- Individuals, households, groups, independent businesses, and other subjects engaged in production, business, and import activities;

- Organizations, individuals producing, conducting business in Vietnam purchasing services (including cases of purchasing services associated with goods) from foreign organizations without a permanent base in Vietnam, foreign individuals not residing in Vietnam, the service purchaser is the taxpayer, excluding cases not required to declare, calculate and pay VAT as guided in Clause 2, Article 5 of Circular 219/2013/TT-BTC.

Regulations on permanent establishments and non-resident entities are implemented according to the laws on corporate income tax and personal income tax.

- Branches of export processing enterprises established to conduct the sale of goods and related activities at industrial zones, export processing zones, and economic zones in accordance with law.