What do the supplementary documents to the tax declaration dossier in Vietnam include?

What do the supplementary documents to the tax declaration dossier in Vietnam include?

According to the provisions of Article 47 of the Law on Tax Administration 2019, the supplementary documents to the tax declaration dossier include:

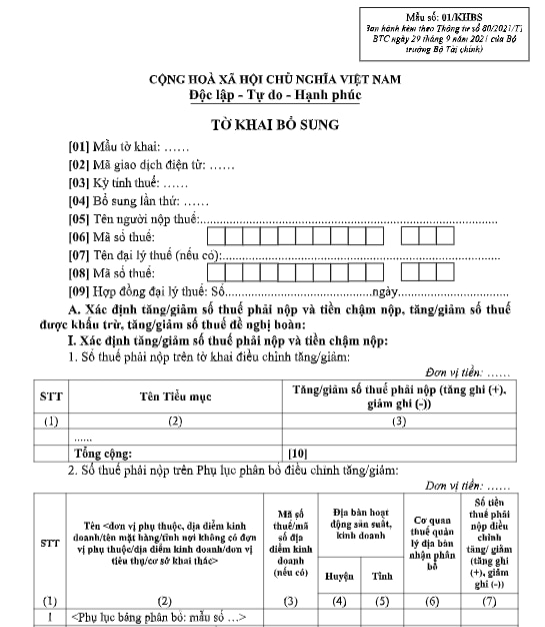

(1) Supplementary declaration form according to Form 01/KHBS issued together with Circular 80/2021/TT-BTC:

Download the supplementary declaration form here

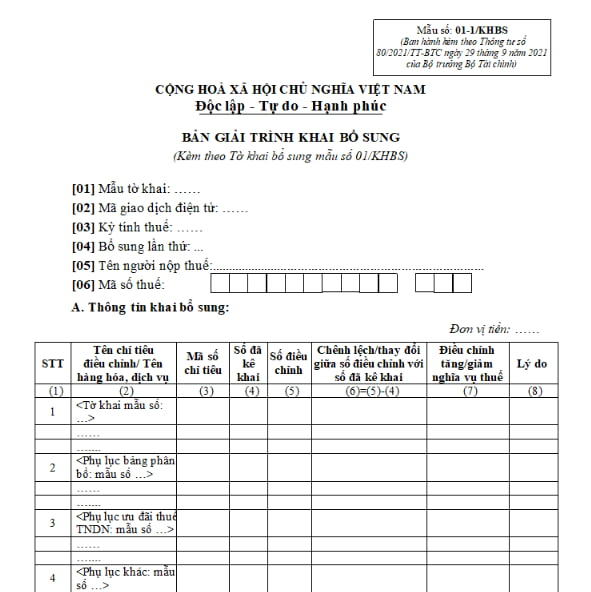

(2) The explanation for the supplementation and relevant documents.

The explanation for the supplementation made in Form 01-1/KHBS as stipulated in Appendix II issued together with Circular 80/2021/TT-BTC is as follows:

Download the explanation for the supplementation here

What do the supplementary documents to the tax declaration dossier in Vietnam include? (Image from Internet)

What entities are required to submit supplementary documents to the tax declaration dossier in Vietnam?

Under Article 47 of the Law on Tax Administration 2019, entities required to submit supplementary documents to the tax declaration dossier are specified as follows:

- In case the tax declaration dossier submitted to the tax authority is erroneous or inadequate, supplementary documents may be provided within 10 years from the deadline for submission of the erroneous or inadequate tax declaration dossier but before the tax authority or a competent authority announces a decision on tax document examination.

- When the tax authority or competent authority has announced the decision on tax inspection or tax audit on the taxpayer’s premises, the taxpayer is still allowed to provide supplementary documents; the tax authority shall impose administrative penalties for the violations specified in Article 142 and 143 of the Law on Tax Administration 2019.

- After the tax authority or competent authority issues a conclusion or tax decision when the inspection is done, the taxpayer may provide supplementary tax documents if they increase the tax payable or reduce the deductible tax, exempted tax or refundable tax, and shall face administrative penalties for the violations specified in Article 142 and Article 143 of Law on Tax Administration 2019;

If the supplementation leads to a decrease in the tax payable or an increase in the deductible tax, exempted tax or refundable tax, the taxpayer shall follow procedures for filing tax-related complaints.

What is the guidance for tax dossier supplementation if the tax declaration dossier is found erroneous in Vietnam?

According to Clause 4, Article 7 of Decree 126/2020/ND-CP, the taxpayer may submit supplementary documents if the tax declaration dossier is found erroneous with specific guidelines as follows:

- If the supplementation does not lead to a change in tax obligations, only a written explanation and relevant declaration is required while a supplementary tax return is not required.

If the annual tax finalization dossier has not been submitted, the taxpayer shall provide supplementary tax documents of the erroneous month or quarter and include the rectification in the annual tax finalization dossier.

If the annual tax finalization dossier has been submitted, only supplementation to the annual tax finalization dossier is required. In case of supplementation of the income payer’s terminal personal income tax return, the erroneous monthly or quarterly tax return shall also be supplemented.

- If the supplementation leads to an increase in the amount of tax payable or decrease in the amount of refundable tax, the arrears or excessively refunded tax plus late payment interest (if any) shall be paid to state budget.

If the supplementation only increases or decreases the deductible VAT which will be carried forward, it must be included in the current tax period. The taxpayer may only increase the refundable VAT if the tax declaration dossier of the next period and the application for tax refund is not submitted.

What are the methods of receiving tax declaration dossiers by tax authorities in Vietnam?

According to Article 48 of the Law on Tax Administration 2019, the responsibilities of tax authorities for receiving tax declaration dossiers are as follows:

Responsibilities of tax authorities for receiving tax declaration dossiers

1. Tax authorities shall receive tax declaration dossiers submitted by taxpayers:

a) in person at the tax authorities;

b) by post;

c) electronically through online portals or tax authorities.

2. Receiving authorities shall send notices of receipt of tax declaration dossiers; inform the taxpayer within 03 working days from the date of receipt if the tax declaration dossier submitted is not legitimate, not adequate or not valid.

Thus, tax authorities shall receive tax declaration dossiers submitted by taxpayers:

- in person at the tax authorities;

- by post;

- electronically through online portals or tax authorities.