What are the environmental protection tax rates for gasoline, oil, and lubricants in Vietnam in 2024?

What are the environmental protection tax rates for gasoline, oil, and lubricants in Vietnam in 2024?

First of all, based on Article 3 of the Environmental Protection Tax Law 2010, the taxable objects are defined as follows:

Taxable Objects

1. Gasoline, oil, and lubricants, including:

a) Gasoline, excluding ethanol;

b) Jet fuel;

c) Diesel oil;

d) Kerosene;

dd) Fuel oil;

e) Lubricating oil;

g) Lubricants.

2. Coal, including:

a) Lignite;

b) Anthracite coal;

c) Fat coal;

d) Other types of coal.

3. Hydro-chloro-fluoro-carbon (HCFC) solution.

4. Plastic bags subject to tax.

5. Herbicides restricted from use.

6. Termite pesticides restricted from use.

7. Forest product preservatives restricted from use.

8. Warehouse disinfectants restricted from use.

9. In cases where it is deemed necessary to supplement other taxable objects, the Standing Committee of the National Assembly shall consider and prescribe them.

the Government of Vietnam stipulates the details of this Article.

Gasoline, oil, and lubricants fall within the scope of environmental protection tax as prescribed.

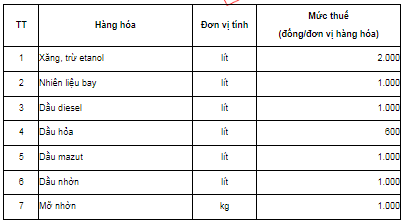

Additionally, the environmental protection tax rate for gasoline, oil, and lubricant from January 1, 2024, to December 31, 2024, is stipulated in Article 1 of Resolution 42/2023/UBTVQH15 as follows:

*Note: The environmental protection tax rate for gasoline, oil, and lubricants from January 1, 2025, shall continue to be implemented in accordance with Section I, Clause 1, Article 1 of Resolution 579/2018/UBTVQH14 dated September 26, 2018, of the Standing Committee of the National Assembly on the Environmental Protection Tax Schedule.

What are the environmental protection tax rates for gasoline, oil, and lubricants in Vietnam in 2024? (Image from the Internet)

What are declaration form for the environmental protection tax when trading gasoline, oil, and lubricants in Vietnam?

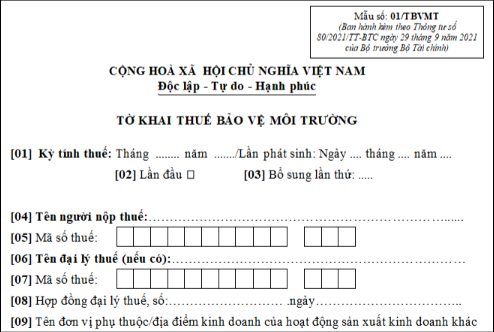

The environmental protection tax declaration form for trading gasoline, oil, and lubricants is prescribed in Clause 3, Article 16 of Circular 80/2021/TT-BTC. To be specific:

Tax Declaration, Calculation, Allocation, and Payment of Environmental Protection Tax

...

3. Tax declaration and payment:

a) For gasoline and oil:

Dependent units of key traders or dependent units of subsidiaries of key traders operating in provinces different from where key traders or their subsidiaries are headquartered and do not account for tax purposes separately for environmental protection tax, then key traders or their subsidiaries shall declare environmental protection tax and submit tax declaration dossiers using Form No. 01/TBVMT, and the appendix of tax allocation for environmental protection to localities where the revenue source is enjoyed for gasoline and oil using Form No. 01-2/TBVMT attached to Appendix II of this Circular to the directly managing tax authority; and pay the apportioned tax amount to the provinces where dependent units are headquartered according to Clause 4, Article 12 of this Circular.

b) For domestically mined and consumed coal:

Enterprises engaged in domestic coal mining and consumption by managing and assigning to subsidiaries or dependent units for mining, processing, and consumption shall declare tax for the total environmental protection tax arising from mined coal and submit tax declaration dossiers using Form No. 01/TBVMT, and the appendix of environmental protection tax determination to localities where the revenue source is enjoyed for coal using Form No. 01-1/TBVMT attached to Appendix II of this Circular to the directly managing tax authority; and pay the apportioned tax amount to the provinces where coal mining companies are headquartered according to Clause 4, Article 12 of this Circular.

According to the above regulations, the environmental protection tax declaration form for trading gasoline, oil, and lubricants is Form No. 01/TBVMT issued with Circular 80/2021/TT-BTC as follows:

>>> Download Latest environmental protection tax declaration form for trading gasoline, oil, and lubricants in 2024.

When is the time for calculating environmental protection tax when importing gasoline, oil, and lubricants in Vietnam?

According to Article 9 of the Environmental Protection Tax Law 2010, the time for calculating environmental protection tax when importing gasoline, oil, and lubricants is defined as follows:

Tax Calculation Time

1. For goods manufactured for sale, exchange, or gift, the tax calculation time is the time of transferring ownership or usage rights of the goods.

2. For goods manufactured for internal use, the tax calculation time is the time of putting the goods into use.

3. For imported goods, the tax calculation time is the time of customs declaration registration.

4. For gasoline and oil manufactured or imported for sale, the tax calculation time is the time when key gasoline and oil traders sell the goods.

Thus, according to the above regulations, the time for calculating environmental protection tax when importing gasoline, oil, and lubricants is the time of customs declaration registration.