What are guidelines for logging in on the thuedientu gdt gov vn portal in 2025?

What are guidelines for logging in on the thuedientu gdt gov vn portal in 2025?

Below is the latest guide to logging in on the thuedientu gdt gov vn portal for 2025 as follows:

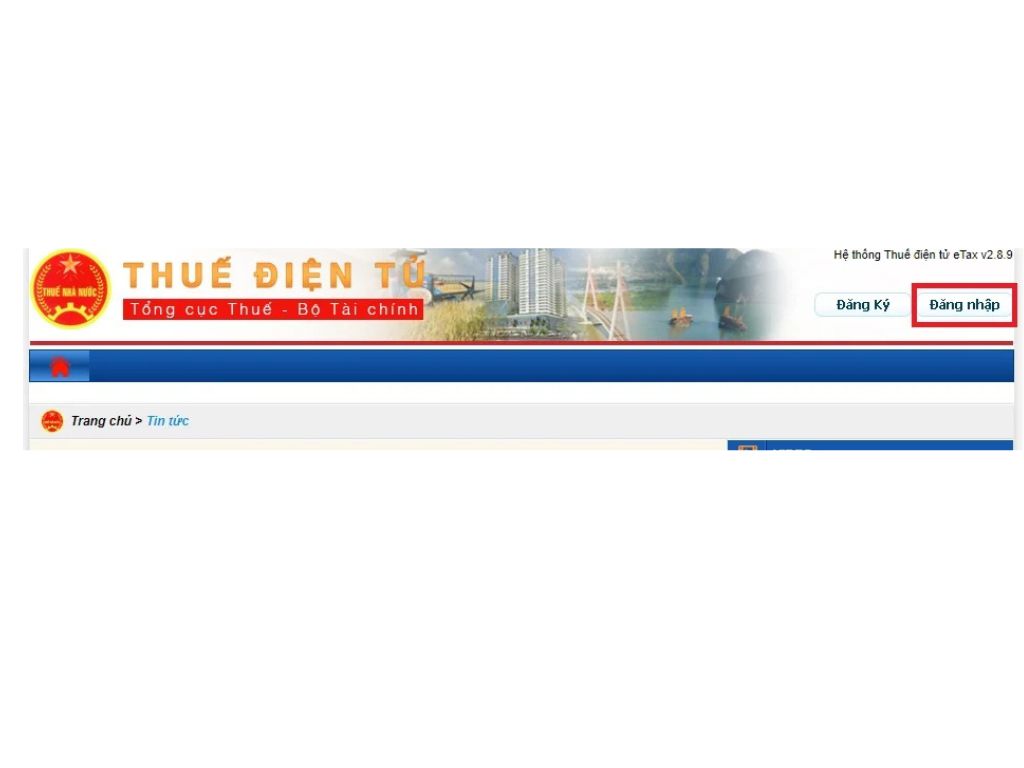

Step 1: Taxpayers access the website:

http://thuedientu.gdt.gov.vn

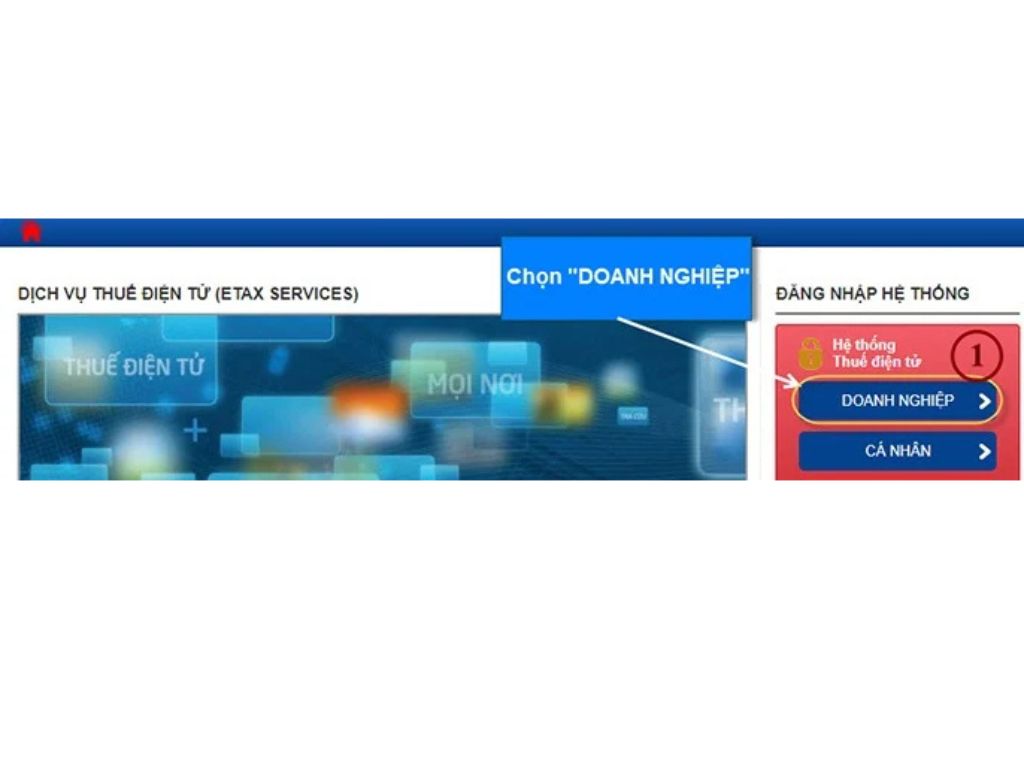

Step 2: Select "Enterprise", then continue to select "Log In"

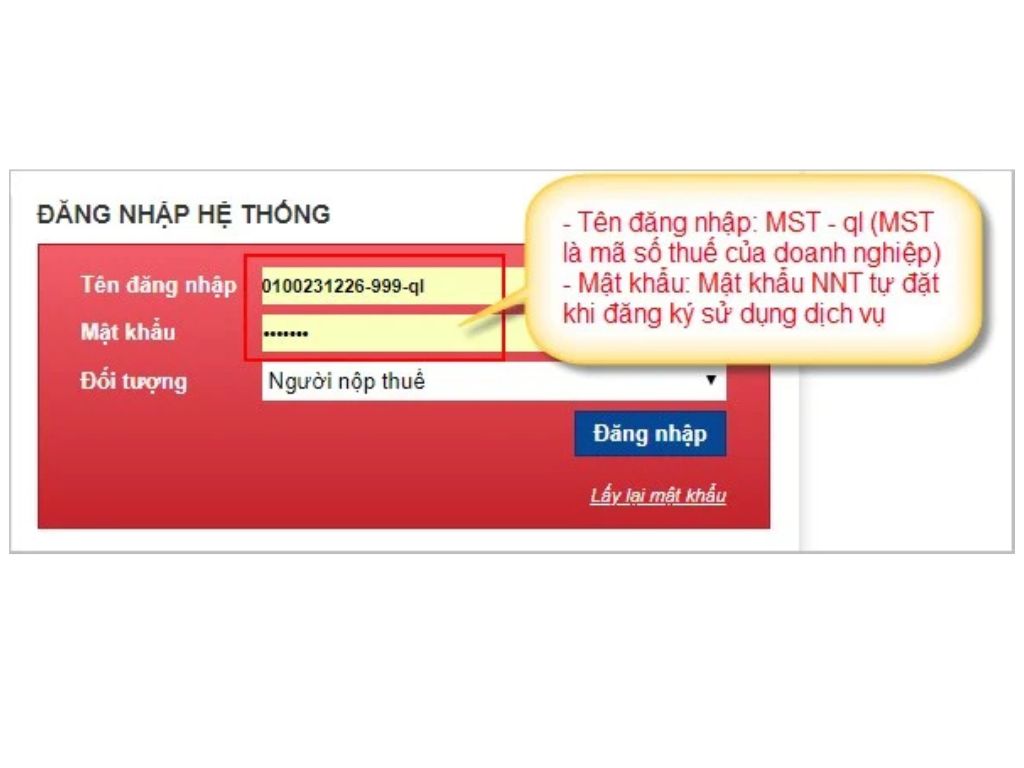

Step 3: Enter the system login information

- Username: MST-ql (MST: Tax Identification Number of the Enterprise; QL: case-insensitive)

- Password: The password set by the taxpayer during the registration for service use

The username must exist in the system and the password must match the one in the system. If the username and password are incorrect, the system will issue a warning.

Step 4. Press the "Log In" button

The system will display the Etax home interface, providing full functionalities on the system:

- Account Management

- Enterprise Management

- Tax Declaration

- Tax Payment

- Lookup

What are guidelines for logging in on the thuedientu gdt gov vn portal in 2025? (Image from Internet)

How to register for e-tax transaction methods in Vietnam?

Pursuant to Clause 3, Article 4 of Circular 19/2021/TT-BTC regarding the registration for the use of e-tax transaction methods as follows:

- Taxpayers conducting e-tax transactions through the General Department of Taxation's Portal must register for e-tax transactions as prescribed in Article 10 of Circular 19/2021/TT-BTC.

- Taxpayers conducting e-tax transactions through the National Public Service Portal or the Ministry of Finance’s Portal connected with the General Department of Taxation's Portal must register as guided by the managing agency of the system.

- Taxpayers conducting e-tax transactions through other competent state agencies connected with the General Department of Taxation's Portal must register following the guidelines of the competent state agency.

- Taxpayers conducting e-tax transactions through T-VAN service providers accepted by the General Department of Taxation connected with the General Department of Taxation's Portal must register for e-tax transactions as prescribed in Article 42 of Circular 19/2021/TT-BTC.

Within the same time period, taxpayers may only choose to register and perform one of the tax administrative procedures prescribed at point a Clause 1 Article 1 of Circular 19/2021/TT-BTC through the General Department of Taxation's Portal, the National Public Service Portal, the Ministry of Finance's Portal, or a T-VAN Service Provider (except for the cases mentioned in Article 9 of Circular 19/2021/TT-BTC).

- Taxpayers choosing the method of e-tax payment through electronic payment services provided by banks or payment service intermediaries must register as guided by the bank or payment service intermediary.

- Taxpayers who have registered for transactions with the tax authorities via electronic means must conduct transactions with the tax authorities in the scope prescribed at Clause 1 Article 1 of Circular 19/2021/TT-BTC by electronic means, except for the cases regulated in Article 9 of Circular 19/2021/TT-BTC.

How to determine the time for e-tax payment in Vietnam?

Based on Clause 1, Article 8 of Circular 19/2021/TT-BTC regarding the time for e-tax payment as follows:

Method for Determining the Time of e-tax Filing, e-tax Payment of Taxpayers, and the Time Tax Authorities Send Notifications, Decisions, Documents to Taxpayers

1. Time of e-tax Filing, e-tax Payment

a) Taxpayers can perform e-tax transactions 24 hours a day (from 00:00:00 to 23:59:59) and 7 days a week, including weekends, public holidays, and Tet. The time taxpayers file is considered within the day if the file is successfully signed within the time from 00:00:00 to 23:59:59 of the day.

b) The point in time for confirming the submission of the e-tax file is determined as follows:

b.1) For e-taxpayer registration files: it is the day the system of the tax authority receives the file and is recorded on the e-taxpayer Registration File Receipt Notification sent by the tax authority to the taxpayer (according to form No. 01-1/TB-TDT issued with this Circular).

b.2) For tax declaration files (except for tax declaration files in cases where the tax authority calculates the tax, notifies the tax payment according to the provisions of Article 13 Decree No. 126/2020/ND-CP): it is the day the system of the tax authority receives the file and is recorded on the e-tax Declaration File Receipt Notification sent by the tax authority to the taxpayer (according to form No. 01-1/TB-TDT issued with this Circular) if the tax declaration file is accepted by the tax authority in the e-tax Declaration File Acceptance Notification sent by the tax authority to the taxpayer (according to form No. 01-2/TB-TDT issued with this Circular).

Specifically for tax declaration files including accompanying documents submitted directly or sent by post: The time for confirming the submission of the tax declaration file is calculated according to the day the taxpayer completes the filing in accordance with regulations.

....

Thus, it can be seen that the determination of the time for e-tax payment is within the day if the file is successfully signed within the 24-hour period.