Vietnam: What is Form 10-MST according to Circular 86? Where to download Form 10-MST?

What is Form 10-MST according to Circular 86? Where to download Form 10-MST?

Based on Clause 1, Article 8 of Circular 86/2024/TT-BTC, the following regulations are stipulated:

Issuance of Certificate of Taxpayer Registration and Notification of Tax Code

The Certificate of Taxpayer Registration and Notification of Tax Code are issued to organizations registering their taxpayer status directly with the tax authority as prescribed in Clause 1, Clause 2, Article 34 of the Law on Tax Administration and the following regulations:

- The “Certificate of Taxpayer Registration” Form No. 10-MST issued with this Circular is granted by the tax authority to organizations not covered under Clause 2 of this Article.

...

Based on Clause 1, Article 23 of Circular 86/2024/TT-BTC, the regulation is as follows:

Handling the Initial Taxpayer Registration Dossier and Issuing the Certificate of Taxpayer Registration, Notification of Tax Code

- For taxpayer registration dossiers as prescribed in Clause 1, Article 22 of this Circular

...

a) In the case where the dossier is complete and the individual's information matches the data in the National Population Database:

...

a.2) For the taxpayer registration dossier of households, individuals doing business as stipulated in Point a, Clause 1, Article 22 of this Circular, the tax authority issues the “Certificate of Taxpayer Registration” Form No. 10-MST attached with this Circular to the household, individual doing business within 3 working days from the date the tax authority receives the complete dossier from the taxpayer.

...

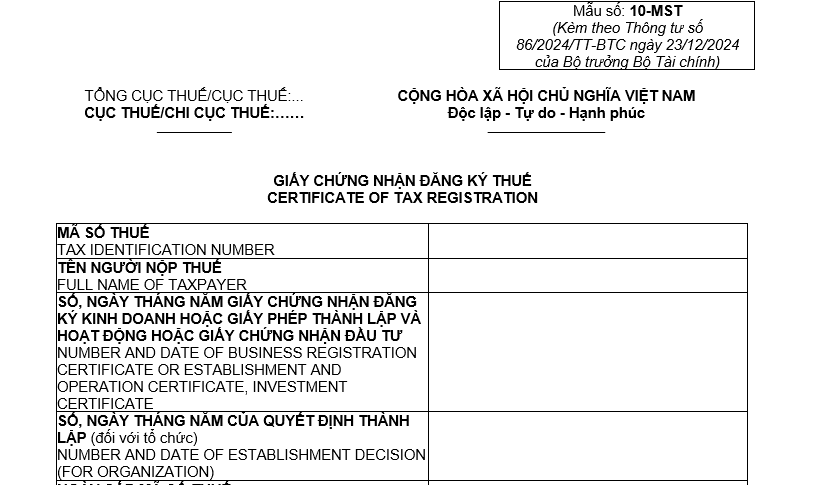

Thus, Form No. 10-MST according to Circular 86 is a Certificate of Taxpayer Registration applicable to organizations, households, and individuals doing business.

Form 10-MST Certificate of Taxpayer Registration as per Circular 86 is shown below:

Download Form 10-MST Certificate of Taxpayer Registration.

Vietnam: What is Form 10-MST according to Circular 86? Where to download Form 10-MST? (Image from the Internet)

What information does the Certificate of Taxpayer Registration include?

According to Clause 1, Article 34 of the Law on Tax Administration 2019, the information contained in the Certificate of Taxpayer Registration includes:

- Name of the taxpayer;

- Tax code;

- Number, date, month, year of the business registration certificate or establishment, operation license or investment registration certificate for organizations, individuals doing business; number, date, month, year of the establishment decision for organizations not required to register business; information from the ID card, citizen's identification card, or passport for individuals not required to register business;

- Direct tax authority management.

In which cases does the tax authority notify the taxpayer's tax code instead of issuing a Certificate of Taxpayer Registration?

According to Clause 2, Article 34 of the Law on Tax Administration 2019, the regulation is as follows:

Issuance of Certificate of Taxpayer Registration

- The tax authority issues the Certificate of Taxpayer Registration to the taxpayer within 3 working days from receiving the complete taxpayer registration dossier as prescribed. The information in the Certificate of Taxpayer Registration includes:

a) Name of the taxpayer;

b) Tax code;

c) Number, date, month, year of the business registration certificate or establishment, operation license or investment registration certificate for organizations, individuals doing business; number, date, month, year of the establishment decision for organizations not required to register business; information from the ID card, citizen's identity card, or passport for individuals not required to register business;

d) Direct tax authority management.

2. The tax authority notifies the taxpayer's tax code instead of issuing a Certificate of Taxpayer Registration in the following cases:

a) Individuals authorize organizations, individuals to pay income taxes on behalf of themselves and their dependents;

b) Individuals register for taxpayer status through a tax declaration dossier;

c) Organizations and individuals register for taxpayer status to deduct and pay taxes on behalf;

d) Individuals register taxpayer status for dependents.

...

Thus, the tax authority notifies the taxpayer's tax code instead of issuing a Certificate of Taxpayer Registration in the following cases:

(1) Individuals authorize organizations, individuals to pay income taxes on behalf of themselves and their dependents;

(2) Individuals register for taxpayer status through a tax declaration dossier;

(3) Organizations and individuals register for taxpayer status to deduct and pay taxes on behalf;

(4) Individuals register taxpayer status for dependents.

What are the regulations on reissuing the Certificate of Taxpayer Registration?

Based on Article 9 of Circular 86/2024/TT-BTC, the regulations for reissuing the Certificate of Taxpayer Registration are as follows:

The Certificate of Taxpayer Registration and Notification of Tax Code are reissued according to Clause 3, Article 34 of the Law on Tax Administration 2019 and the following regulations:

- In case of loss, tear, deterioration, or burning of the Certificate of Taxpayer Registration, the taxpayer sends a Request for Reissuance of the Certificate of Taxpayer Registration Form No. 13-MST attached with Circular 86/2024/TT-BTC to the direct managing tax authority.

- The tax authority reissues the Certificate of Taxpayer Registration via the electronic portal of the General Department of Taxation within 2 working days from the date of receiving the complete dossiers as prescribed. If the taxpayer registers to receive results directly at the tax authority or via postal service, the tax authority is responsible for sending the results via the one-stop-shop division of the tax authority or via public postal service to the address registered by the taxpayer.