What is the notification template of acceptance or non-acceptance of electronic documents sent by tax authorities in Vietnam?

What is the notification template of acceptance or non-acceptance of electronic documents sent by tax authorities in Vietnam?

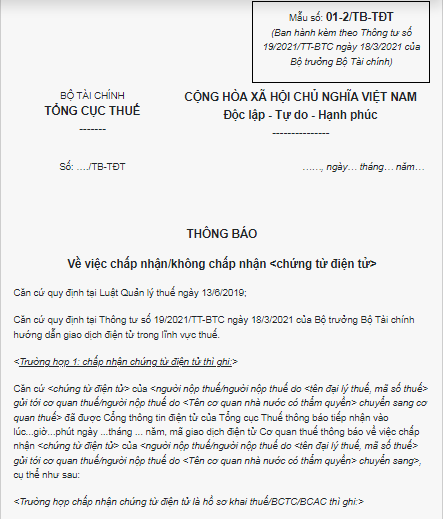

Under the list of forms/templates promulgated together with Circular No. 19/2021/TT-BTC, the tax authority will notify the acceptance or non-acceptance of electronic documents using Template 01-2/TB-TDT as follows:

>>> Download the newest notification template of acceptance or non-acceptance of electronic documents.

*Note:

- Italic text within <> is explanatory or an example.

- Choose either case 1 or 2 according to the processing result.

- “<Electronic Document>” in this form refers to one of the following applications/dossiers:

+ Taxpayer registration application <initial taxpayer registration/application for change in taxpayer registration information/suspension of operation or continuation of temporarily suspended operation before the deadline>;

+ Tax declaration dossier <tax declaration dossier/financial statement/report on invoice use/ electronic tax declaration in cases where the tax authority calculates the tax and notifies the taxpayer>;

+ Application for tax exemption or reduction;

+ Application for review/Application for confirmation of tax obligation fulfillment/document requesting handling of overpaid amounts;

+ Dosser for handling debts <Application for exemption from late payment interest/not calculating late payment interest/debt deferral/tax debt cancellation/extension of tax payment/ installment payment of tax debt>;

+ Other electronic tax dossier;

+ Dossier for determining financial obligations, tax declaration dossier/application for tax exemption or reduction according to the single-window system.

Tax Authority Notification regarding acceptance or non-acceptance of electronic documents - Which Form? (Image from the Internet)

What is the relationship between T-VAN service providers and taxpayers in Vietnam?

Under Article 45 Circular No. 19/2021/TT-BTC, the relationship between T-VAN service providers and taxpayers is as follows:

Relationship between of t-van service providers and taxpayers

The relationship between a T-VAN service provider and a taxpayer is determined on the basis of the T-VAN service contract.

1. The T-VAN service provider shall:

a) Publish the operating method and service quality on its website.

b) Provide transmission services and complete the format of e-documents to facilitate exchange of information between taxpayers and tax authorities.

c) Transmit and receive e-documents punctually and completely under agreements with other parties.

d) Retain result of every transmission and receipt; retain e-documents before transactions are successfully done.

dd) Ensure connection, security, integration of information, and provide other utilities for other participants in the exchange of e-documents.

e) Give taxpayers and tax authorities ten days' notice of the date of a system outage for maintenance days and take measures for protecting taxpayers’ interests.

g) Send e-tax dossiers of taxpayers to tax authorities and transfer results of processing of e-tax dossiers by tax authorities to taxpayers on schedule as prescribed in this Circular, in the case of sending dossiers against regulations resulting late submission of dossiers, be responsible to taxpayers as prescribed by law.

h) Provide compensation for taxpayers under regulations of law and civil contracts between 2 parties in case the taxpayer suffers any damage through the T-VAN service provider's fault.

2. The taxpayer shall:

a) Adhere to terms and conditions of the contract with the T-VAN service provider.

b) Enable the T-VAN service provider to implement system safety and security measures.

c) Take legal responsibility for their e-tax dossiers.

Thus, the relationship between T-VAN service providers and taxpayers is determined on the basis of the T-VAN service contract.

What is the relationship between T-VAN service providers and tax authorities in Vietnam?

Under Article 46 Circular No. 19/2021/TT-BTC, the relationship between T-VAN service providers and tax authorities is as follows:

Every T-VAN service providers must comply with the technical requirements and standards for connection with the GDT’s web portal during provision of T-VAN services.

- Every T-VAN service provider shall:

+ Reserve the right to provide T-VAN services to taxpayers from the date on which the GDT publish the list of T-VAN service providers on its web portal.

+ Send e-tax declaration dossiers to the GDT’s web portal at least once every hour from the receipt of e-tax declaration dossiers from taxpayers; other e-documents must be immediately sent to tax authorities.

+ Send results of processing of e-tax dossiers by tax authorities to taxpayers after receiving results from the GDT’s web portal.

+ Provide sufficient information and data for tax authorities at their request as prescribed by law.

+ Comply with applicable regulations of law on telecommunications, Internet, and technical and professional regulations imposed by competent authorities.

+ Establish a channel to connect with the GDT’s web portal to implement T-VAN services in a manner that ensures continuity, safety and security. Proactively resolve difficulties that arise during the provision of T-VAN services and report those related to the GDT’s web portal to tax authorities for resolving in cooperation.

Notify taxpayers and tax authorities of errors of the web portal of the T-VAN service provider as prescribed in Article 9 of this Circular.

+ Submit reports on provision of T-VAN services to GDT under the signed agreement.

- Every tax authority shall:

+ Reserve the right to carry out site inspection according to the criteria prescribed in Clause 2 Article 41 hereof if during the provision of services by every T-VAN service provider the tax authority receives feedback from individuals and units concerned; or finds that the T-VAN service provider fails to satisfy the technical standards published by GDT or violates any terms or conditions of the signed agreement or violates any regulations of law on e-transactions.

+ Establish, maintain and ensure connection between the GDT’s web portal and the T-VAN service providers’ information exchange systems.

+ Inspect the operation of every T-VAN service provider to ensure their service quality and operation comply with regulations.

+ Provide assistance in tax operations in order for T-VAN service providers to conduct transactions in transmission and receipt between taxpayers and tax authorities; cooperate with T-VAN service providers in providing training to taxpayers; assist in resolving difficulties that arise during the provision of T-VAN services; provide standard forms and formats to T-VAN service providers in order for them to provide services.

+ Send its notifications, decisions and documents mentioned in this Circular to T-VAN service providers’ information exchange systems in order for them to send them to taxpayers.