Lunisolar Calendar for March 2025 - Perpetual Calendar for March 2025

Lunisolar Calendar for March 2025 - Perpetual Calendar for March 2025

Consulting the Lunisolar Calendar helps you accurately grasp auspicious and inauspicious days, important holidays, events, and facilitates arranging work, worship, or organizing activities according to traditional customs.

Below is the complete, detailed, and latest Lunisolar Calendar for March 2025 - Perpetual Calendar for March 2025 for your reference:

Lunisolar Calendar for March 2025 - Complete, Detailed, Latest Perpetual Calendar for March 2025

Lunisolar Calendar for March 2025 - Complete, Detailed, Latest Perpetual Calendar for March 2025

Lunisolar Calendar for March 2025 - Perpetual Calendar for March 2025 (Image from the Internet)

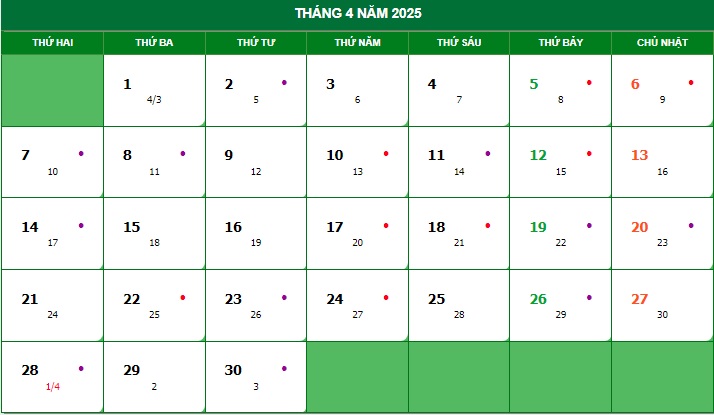

Which holidays in the 3th month of Lunisolar Calendar allow Vietnamese tax officials to rest with full pay?

Based on Article 112 of the Labor Code 2019 which stipulates holidays as follows:

Holidays

- Employees are entitled to rest with full pay on the following holidays:

a) New Year's Day: 01 day (January 1, Gregorian calendar);

b) Lunar New Year: 05 days;

c) Victory Day: 01 day (April 30, Gregorian calendar);

d) International Labor Day: 01 day (May 1, Gregorian calendar);

e) National Day: 02 days (September 2, Gregorian calendar and 01 day immediately before or after);

f) Hung Kings' Commemoration Day: 01 day (March 10, Lunisolar Calendar).

- Foreign employees working in Vietnam, in addition to the holidays prescribed in clause 1 of this Article, are entitled to an additional 01 traditional Tet holiday and 01 national day of their country.

- Annually, based on the actual conditions, the Prime Minister of the Government of Vietnam decides the specific holidays specified at points b and đ, clause 1 of this Article.

Thus, in the holidays of the lunar month of March 2025, there is the Hung Kings’ Commemoration Day (March 10, Lunisolar Calendar) which will fall on Monday, April 7, 2025, Gregorian calendar. Accordingly, tax officials will be entitled to leave and enjoy full pay on this holiday.

How to calculate benefits for Vietnamese tax officials retiring before the age when reorganizing the political system in 2025?

Based on Article 4 of Circular 1/2025/TT-BNV which stipulates the calculation of benefits for tax officials retiring before the age when reorganizing the political system as follows:

Tax officials who meet the conditions and are decided by a competent authority to retire before the statutory retirement age are entitled to immediately receive their pension according to the law on social insurance without being reduced the pension rate due to early retirement; they are also entitled to a one-time retirement allowance, an allowance for the number of years of early retirement, and an allowance based on the time of service with compulsory social insurance contributions, specifically:

(1) For cases with at least 02 years to 05 years remaining until the statutory retirement age as stipulated in point a and point c, clause 2, Article 7 of Decree 178/2024/ND-CP, the official receives the following 03 allowances:

- One-time retirement allowance for months of early retirement:

+ For those retiring within the first 12 months:

| One-time retirement allowance | = | Current monthly salary | x 1.0 x | Early retirement months |

+ For those retiring from the 13th month onwards:

| One-time retirement allowance | = | Current monthly salary | x 0.5 x | Early retirement months |

- Allowance for the number of years of early retirement: For each year of early retirement (full 12 months), 05 months of the current monthly salary is received.

| Allowance for early retirement years | = | Current monthly salary | x 5 x | Early retirement years |

- Allowance based on the time of service with compulsory social insurance contributions:

For the first 20 years of service with compulsory social insurance contributions, 5 months of the current monthly salary is received; for the remaining years (from the 21st year onwards), each year receives an allowance equal to 0.5 months of the current monthly salary.

| Allowance based on service time with compulsory social insurance contributions | = | Current monthly salary | x | 5 (for the first 20 years of service with compulsory social insurance contributions) | + | 0.5 x | Remaining service years with compulsory social insurance contributions from the 21st year onwards |

(2) For cases with more than 05 years to 10 years remaining until the statutory retirement age as stipulated in point b, clause 2, Article 7 of Decree 178/2024/ND-CP, the official receives the following 03 allowances:

- One-time retirement allowance for months of early retirement:

+ For those retiring within the first 12 months:

| One-time retirement allowance | = | Current monthly salary | x 0.9 x 60 months |

+ For those retiring from the 13th month onwards:

| One-time retirement allowance | = | Current monthly salary | x 0.45 x 60 months |

- Allowance for the number of years of early retirement: For each year of early retirement (full 12 months), 04 months of the current monthly salary is received.

| Allowance for early retirement years | = | Current monthly salary | x 4 x | Early retirement years |

- Allowance based on the time of service with compulsory social insurance contributions:

For the first 20 years of service with compulsory social insurance contributions, 5 months of the current monthly salary is received; for the remaining years (from the 21st year onwards), each year receives an allowance equal to 0.5 months of the current monthly salary.

| Allowance based on service time with compulsory social insurance contributions | = | Current monthly salary | x | 5 (for the first 20 years of service with compulsory social insurance contributions) | + | 0.5 x | Remaining service years with compulsory social insurance contributions from the 21st year onwards |

(3) For cases with less than 02 years remaining until the statutory retirement age stipulated in point d and point đ, clause 2, Article 7 of Decree 178/2024/ND-CP, the official is entitled to a one-time retirement allowance for months of early retirement calculated like those retiring within the first 12 months as follows:

| One-time retirement allowance | = | Current monthly salary | x 1.0 x | Early retirement months |

Where:

- The current monthly salary is determined as follows:

+ For those receiving salaries according to the salary scale set by the State:

The current monthly salary includes: Salary level according to rank, grade, position, title, professional title and salary allowance (including: Position allowance; seniority allowance beyond the frame; professional seniority allowance; preferential allowance according to profession; professional responsibility allowance; civil service allowance; political, mass organization work allowance, if any), specifically:

| Current monthly salary | = | Salary coefficient according to rank, grade, position, title, professional title | x | Statutory pay rate | + | Leadership position allowance coefficient (if any) | x | Statutory pay rate | + | Amount of allowances calculated based on the salary rank, grade, position, title, professional title (if any) |

The statutory pay rate to calculate the current monthly salary mentioned above is the rate prescribed by the Government of Vietnam at the time immediately preceding the month of retirement.

+ For those receiving a salary according to an amount agreed in the labor contract, the current monthly salary is the monthly salary stated in the labor contract.

- Early retirement months are the months calculated from the retirement time according to the decision of the competent authority compared with the statutory retirement age as prescribed in Appendix 1 or Appendix 2 issued with Decree 135/2020/ND-CP.

- Early retirement years are the years calculated from the retirement time according to the decision of the competent authority compared with the statutory retirement age as prescribed in Appendix 1 or Appendix 2 issued with Decree 135/2020/ND-CP and calculated according to clause 4, Article 5 of Decree 178/2024/ND-CP.