Is there a reduction in excise tax when the taxpayer is affected by natural disasters in Vietnam? What are cases where excise tax is refunded?

Is there a reduction in excise tax when the taxpayer is affected by natural disasters in Vietnam?

According to Clause 1, Article 52 of Circular 80/2021/TT-BTC, the tax authority announces or decides on tax exemption or reduction in the following cases:

- Exemption from personal income tax for incomes as stipulated in Clauses 1, 2, 3, 4, 5, and 6 of Article 4 of the Law on Personal Income Tax;

- Tax reduction as prescribed for individuals, business households, and business individuals facing difficulties due to natural disasters, fires, accidents, or serious illnesses affecting tax payment abilities;

- Reduction of excise tax for taxpayers producing goods subject to excise tax encountering difficulties due to natural disasters or unexpected accidents according to the law on excise tax;

- Exemption and reduction of resource tax for taxpayers who encounter natural disasters, fires, or unexpected accidents causing losses to declared and taxed resources;

- Exemption and reduction of non-agricultural land use tax;

- Exemption and reduction of agricultural land use tax as per the Law on Agricultural Land Use Tax and Resolutions of the National Assembly;

- Exemption and reduction of land rent, water surface rent, land levy;

- Exemption from registration fees.

Taxpayers will receive a reduction in the excise tax for those producing goods subject to this tax and who face difficulties due to sudden natural disasters, as per the law on excise tax.

Thus, it can be seen that a reduction in excise tax is granted for taxpayers producing goods when they face unexpected natural disasters according to the law on excise tax.

Is there a reduction in excise tax when the taxpayer is affected by natural disasters in Vietnam? What are cases where excise tax is refunded? (Image from the Internet)

What conditions are required for excise tax deduction in Vietnam?

Pursuant to Clause 3, Article 7 of Decree 108/2015/ND-CP (amended by Clause 3, Article 1 of Decree 14/2019/ND-CP), the conditions for excise tax deduction are specifically stipulated as follows:

(1) For cases of importing materials subject to excise tax to produce goods subject to excise tax, and importing goods subject to excise tax, the documentation for tax deduction is the tax payment document for excise tax at the import stage.

(2) For cases of purchasing materials directly from domestic manufacturers:

- The sales contract must indicate that the goods are produced directly by the selling establishment; a copy of the Business Registration Certificate of the selling establishment (signed and stamped by the selling establishment).

- Bank payment documents.

- The document for deduction of excise tax is the value-added tax invoice upon purchase.

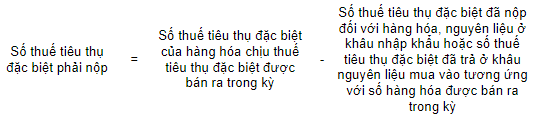

The excise tax that the purchasing unit has paid for materials is calculated as the tax calculation price multiplied by the excise tax rate; wherein:

The deduction of excise tax is done during the excise tax declaration, and the payable excise tax is determined using the following formula:

Note: In cases where it is not possible to determine accurately the amount of excise tax paid (or incurred) for the number of materials corresponding to the products consumed in the period, previous period data can be used to calculate the deductible excise tax, and this will be finalized at the end of the quarter or end of the year.

In all cases, the maximum deductible excise tax does not exceed the excise tax calculated on the materials as per the technical-economic standards of the product.

What are cases eligible for excise tax refund in Vietnam?

According to Clause 4, Article 7 of Circular 195/2015/TT-BTC as follows:

Tax Refund

...

4. Cases of excise tax refund:

a) Tax refund according to the decision of the competent authority as stipulated by law.

b) Tax refund under an international agreement to which the Socialist Republic of Vietnam is a member.

c) Tax refund in cases where the amount of excise tax paid exceeds the amount of excise tax to be paid as prescribed.

The procedures, dossiers, sequence, and authority to resolve excise tax refunds as prescribed in Clauses 3 and 4 of this Article are implemented according to the Law on Tax Administration and guiding documents.

Thus, excise tax can be refunded in the following cases:

- Tax refund according to the decision of the competent authority as stipulated by law.

- Tax refund under an international agreement to which the Socialist Republic of Vietnam is a member.

- Tax refund in cases where the amount of excise tax paid exceeds the amount to be paid as prescribed.