Who is considered a dependant for personal exemptions in Vietnam?

Who is considered a dependant for personal exemptions in Vietnam?

Pursuant to Article 9 of Circular 111/2013/TT-BTC (provisions related to personal income tax for business individuals are annulled by Clause 6, Article 25 of Circular 92/2015/TT-BTC), clear regulations on dependants are as follows:

Deductions

Deductions as guided in this Article are amounts deducted from the taxable income of individuals before determining the taxable income from salary, wages, and business income. Specifically:

- Personal exemptions

...

d) dependants include:

d.1) Children: biological children, legally adopted children, illegitimate children, stepchildren of the wife, stepchildren of the husband, specifically including:

d.1.1) Children under 18 years old (calculated cumulatively by month).

Example 10: Mr. H’s child was born on July 25, 2014, thus counted as a dependant from July 2014.

d.1.2) Children 18 years old and older who are disabled and incapable of working.

d.1.3) Children studying in Vietnam or abroad at university, college, vocational school, including children 18 years and older still in high school (counting the time from June to September of Grade 12 awaiting university exam results) with no income or average monthly income from all sources not exceeding 1,000,000 VND.

d.2) Spouse of the taxpayer meeting the conditions at point đ, clause 1, of this Article.

d.3) Biological parents; parents-in-law; stepparents; legally adoptive parents of the taxpayer meeting the conditions at point đ, clause 1, of this Article.

d.4) Other individuals without support, directly nurtured by the taxpayer and meeting the conditions at point đ, clause 1, of this Article, including:

d.4.1) Siblings of the taxpayer.

d.4.2) Paternal or maternal grandparents; aunts, uncles of the taxpayer.

d.4.3) Nephews and nieces of the taxpayer including: children of the taxpayer’s siblings.

d.4.4) Other individuals directly nurtured by the taxpayer as stipulated by law.

đ) Individuals considered as dependants according to the guidance at points d.2, d.3, d.4, of point d, clause 1, of this Article must meet the following conditions:

đ.1) For individuals within working age, all of the following conditions must be met:

đ.1.1) Disabled, incapable of working.

đ.1.2) No income or average monthly income from all sources not exceeding 1,000,000 VND.

đ.2) For individuals beyond working age, they must have no income or average monthly income from all sources not exceeding 1,000,000 VND.

e) Disabled individuals, incapable of working, as guided at point đ.1.1, point đ, clause 1, of this Article, are those subject to laws on disabled persons and individuals with diseases that render them incapable of working (such as AIDS, cancer, chronic kidney failure, etc.).

...

Thus, employees are entitled to personal exemptions for the following dependants:

- Children: biological children, legally adopted children, illegitimate children, stepchildren of the wife, stepchildren of the husband, specifically including:

+ Children under 18 years old (calculated cumulatively by month).

+ Children 18 years old and older who are disabled and incapable of working.

+ Children studying in Vietnam or abroad at university, college, vocational school, including children 18 years and older still in high school (counting the time from June to September of Grade 12 awaiting university exam results) with no income or average monthly income from all sources not exceeding 1,000,000 VND.

- Spouse of the taxpayer meeting the conditions at point đ, clause 1, of Article 9 of Circular 111/2013/TT-BTC.

- Biological parents; parents-in-law; stepparents; legally adoptive parents of the taxpayer meeting the conditions at point đ, clause 1, of Article 9 of Circular 111/2013/TT-BTC.

- Other individuals without support, directly nurtured by the taxpayer and meeting the conditions at point đ, clause 1, of Article 9 of Circular 111/2013/TT-BTC:

+ Siblings of the taxpayer.

+ Paternal or maternal grandparents; aunts, uncles of the taxpayer.

+ Nephews and nieces of the taxpayer including children of the taxpayer’s siblings.

+ Other individuals directly nurtured by the taxpayer as stipulated by law.

- Individuals considered as dependants according to the guidance at points d.2, d.3, d.4, point d, clause 1, of Article 9 Circular 111/2013/TT-BTC

+ For individuals within working age, all of the following conditions must be met:

+ Disabled, incapable of working.

+ No income or average monthly income from all sources not exceeding 1,000,000 VND.

+ For individuals beyond working age, they must have no income or average monthly income from all sources not exceeding 1,000,000 VND.

- Disabled individuals, incapable of working, as guided at point đ.1.1, point đ, clause 1, Article 9 Circular 111/2013/TT-BTC are those subject to laws on disabled persons and individuals with diseases that render them incapable of working (such as AIDS, cancer, chronic kidney failure, etc.).

Who is considered a dependant for personal exemptions in Vietnam? (Image from the Internet)

What Is the current level of personal exemption in Vietnam?

Pursuant to Article 1 of Resolution 954/2020/UBTVQH14:

Level of personal exemption

Adjust the level of personal exemption specified in clause 1, Article 19 of the Law on Personal Income Tax No. 04/2007/QH12, as amended and supplemented by Law No. 26/2012/QH13 as follows:

- Deduction for the taxpayer: 11 million VND/month (132 million VND/year);

- Deduction for each dependant: 4.4 million VND/month.

Thus, the current level of personal exemptions is as follows:

- Taxpayer: 11 million VND/month (132 million VND/year);

- For each dependant: 4.4 million VND/month.

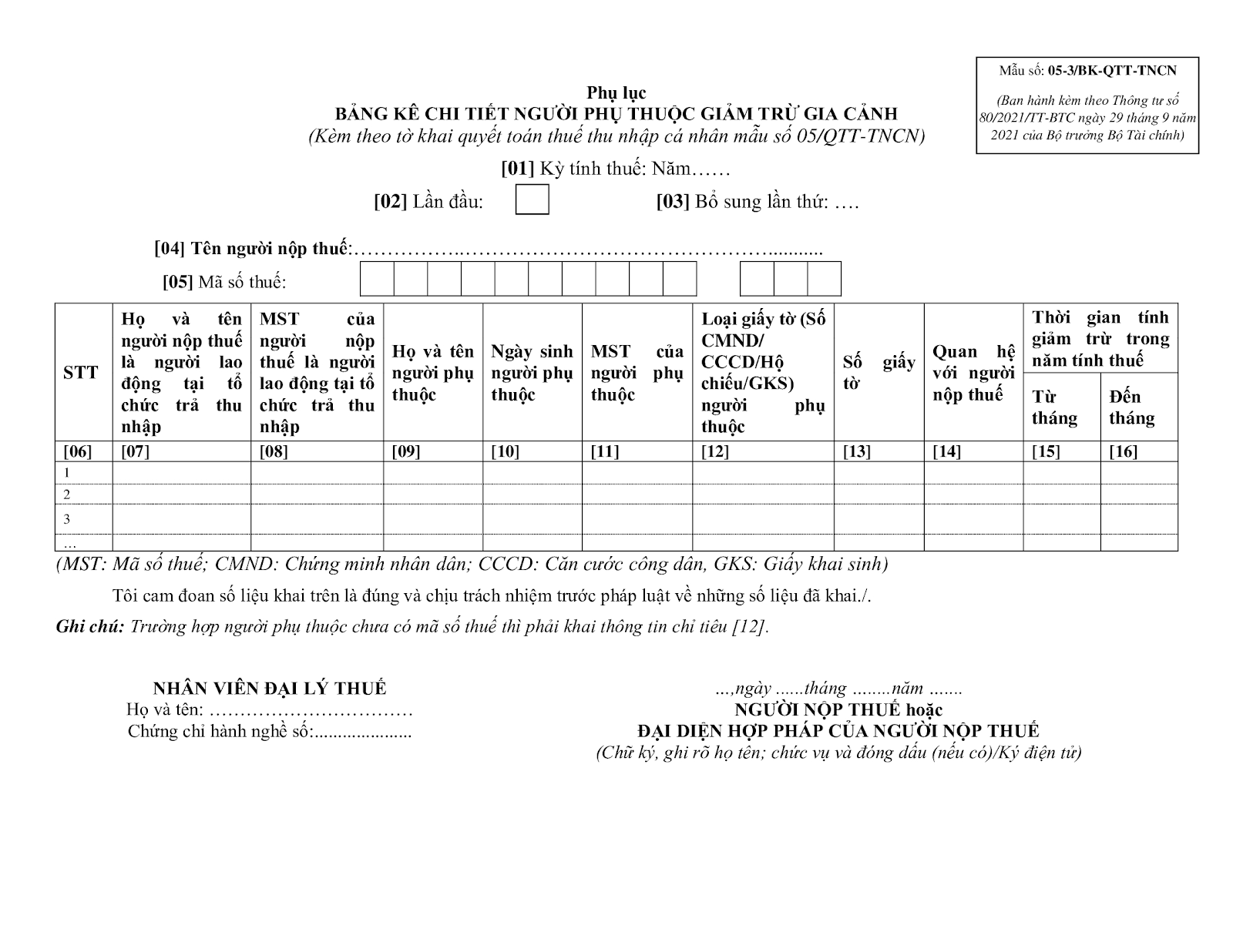

What is Appendix 05-3/BK-QTT-TNCN - List of personal exemptions for dependants in Vietnam?

Appendix 05-3/BK-QTT-TNCN - Detailed list of personal exemptions for dependants is issued with Circular 80/2021/TT-BTC as follows:

Download form 05-3/BK-QTT-TNCN: https://cdn.lawnet.vn/uploads/giao-duc/DVM/05-3-BK-QTT-TNCN.dochere