Which form is the VAT declaration for investment projects in Vietnam? Which goods and services not eligible for VAT reduction in Vietnam in 2024?

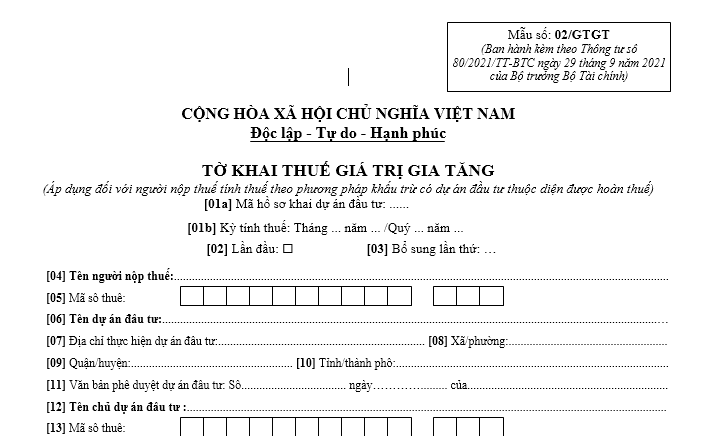

Which form is the VAT declaration for investment projects in Vietnam?

According to Form 02/GTGT, stipulated in Appendix 2 issued with Circular 80/2021/TT-BTC, the VAT declaration (applicable to taxpayers calculating tax by the deduction method with investment projects eligible for a tax refund) is as follows:

>>> Download VAT declaration for investment projects.

Which form is the VAT declaration for investment projects in Vietnam? Which goods and services not eligible for VAT reduction in Vietnam in 2024? (Image from Internet)

What are regulations on VAT reduction rates in Vietnam under Decree 72?

Pursuant to Clause 2, Article 1 of Decree 72/2024/ND-CP, the VAT reduction rates under Decree 72 are stipulated as follows:

- Businesses calculating VAT by the deduction method are applicable for an 8% VAT rate for goods and services stipulated in Clause 1, Article 1 of Decree 72/2024/ND-CP.

- Businesses (including household businesses and individual businesses) calculating VAT by the percentage method on revenue are eligible for a 20% reduction in the percentage rate for calculating VAT when issuing invoices for goods and services eligible for a VAT reduction as stipulated in Clause 1, Article 1 of Decree 72/2024/ND-CP.

Moreover, VAT reduction will be carried out according to the following procedures:

- For businesses stipulated in point a, Clause 2, Article 1 of Decree 72/2024/ND-CP, when issuing VAT invoices for providing goods and services subject to VAT reduction, the VAT rate line should state "8%"; VAT amount; total amount payable by the buyer.

Based on the VAT invoice, businesses selling goods and services declare output VAT, businesses purchasing goods and services declare input VAT deduction according to the reduced tax amount stated on the VAT invoice.

- For businesses stipulated in point b, Clause 2, Article 1 of Decree 72/2024/ND-CP, when issuing sales invoices for providing goods and services subject to VAT reduction, in the "Amount" column, record the full amount of goods and services before reduction, in the "Total goods and services amount" line, record according to the amount reduced by 20% of the percentage rate on revenue, and note: "reduced by... (amount) corresponding to 20% of the percentage rate for calculating VAT according to Resolution 142/2024/QH15."

Which goods and services not eligible for VAT reduction in Vietnam in 2024?

The groups of goods and services not eligible for VAT reduction in 2024 are stipulated in Clause 1, Article 1 of Decree 72/2024/ND-CP on the policy of VAT reduction as follows:

* VAT reduction for groups of goods and services currently applying a 10% tax rate, except for the following groups of goods and services:

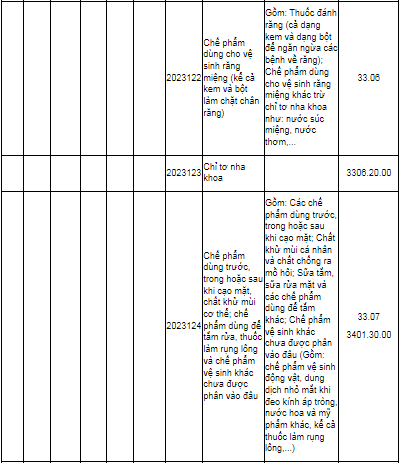

[1] Telecommunications, financial activities, banking, securities, insurance, real estate businesses, metals and fabricated metal products, mining products (excluding coal mining), coke, refined petroleum, chemical products. Details in Appendix 1 issued with this Decree. (Download Appendix 1)

[2] Goods and services subject to special consumption tax. Details in Appendix 2 issued with this Decree. (Download Appendix 2)

[3] Information technology according to the law on information technology. Details in Appendix 3 issued with this Decree. (Download Appendix 3)

[4] VAT reduction for each type of goods and services stipulated in Clause 1, Article 1 of Decree 72/2024/ND-CP is uniformly applied in the stages of import, production, processing, and commercial business.

For mined coal sold (including cases where mined coal is screened, classified through a closed process before being sold), it is eligible for VAT reduction.

Coal products are listed in Appendix 1 issued with this Decree

(Download Appendix 1), at stages other than extraction, do not receive VAT reduction.

General corporations, economic groups conducting a closed process before selling are also eligible for VAT reduction for mined coal sold.

In cases where goods and services specified in Appendices 1, 2, and 3 issued with this Decree fall under non-VAT subjects or subjects subject to 5% VAT according to the VAT Law, they shall be carried out according to the VAT Law and are not eligible for VAT reduction.

Therefore, it can be seen that goods and services subject to the previous 10% VAT rate will have a 2% VAT reduction but exclude the aforementioned cases.

In particular, dental floss is a product within the group of goods and services not eligible for VAT reduction.

Thus, dental floss will not benefit from a VAT reduction.