Which entities use the agricultural land use tax declaration form - Form 02/SDDNN in Vietnam?

Which entities use the agricultural land use tax declaration form - Form 02/SDDNN in Vietnam?

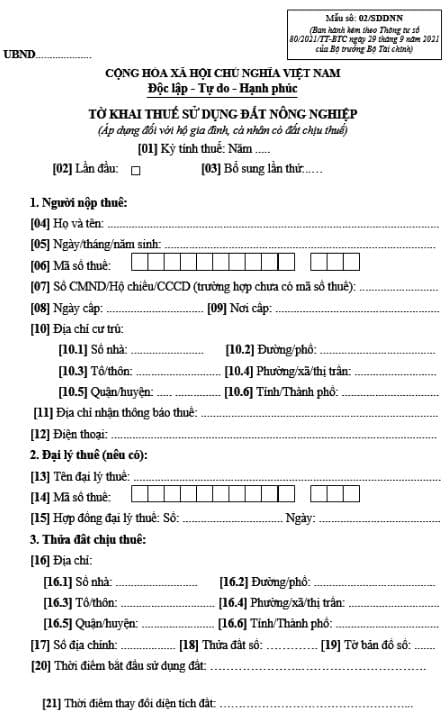

The agricultural land use tax declaration form - Form 02/SDDNN will be used by individuals and households with taxable land as stipulated in Appendix 2 issued together with Circular 80/2021/TT-BTC:

Download the agricultural land use tax declaration form - Form 02/SDDNN: Here

Which entities use the agricultural land use tax declaration form - Form 02/SDDNN in Vietnam? (Image from the Internet)

What are the agricultural land use tax payment methods in Vietnam?

According to sub-section 3, Section 4 Circular 89-TC/TCT in 1993, the payment of agricultural land use tax is regulated as follows:

IV. ORGANIZATION OF TAX payment

...

3. Tax payment.

a. Tax payment in cash: When collecting tax from residents, tax or treasury staff must check and compare the payable tax amount recorded on the notice with the amount the taxpayer brings for payment, while writing and issuing a receipt to the taxpayer and recording it in the tax payment monitoring book.

In cases where the taxpayer does not directly submit to the treasury, at the end of each day, the tax payment staff must compare the tax payment receipts with the collected tax amount and every 10 days must submit all collected tax amounts to the State Treasury. If the collected tax amount is 5 million VND or more, it must be submitted immediately to the State Treasury. Retaining tax money beyond this regulated amount without submitting to the State Treasury is considered an act of tax fund embezzlement.

b. Tax payment by bank transfer: Tax payment by bank transfer is processed by the taxpayer. Tax authorities must keep a record of taxpayers who pay by transfer for periodic reconciliation with the treasury and to remind taxpayers.

c. Tax payment in paddy (if applicable): The organization collecting paddy must directly receive it from taxpayers in the presence of a tax authority representative to issue tax receipts to taxpayers. The organization purchasing paddy for tax must settle with the State budget immediately during the tax payment season as prescribed by the Chairman of the Provincial People's Committee.

...

Thus, agricultural land use tax payment forms include payment in cash; payment by bank transfer, and payment in paddy.

How many times is agricultural land use tax paid per year in Vietnam?

According to Article 11 Decree 74-CP in 1993:

Article 11.

The agricultural land use tax year follows the calendar year from January 1 to December 31.

Tax is calculated annually but collected once or twice a year depending on the main crop of each type of plant in each locality.

Taxpayers can pay the tax before the due date, and during the first collection, they can pay the entire annual tax amount.

According to the proposal of the Director of the Tax Department, the Chairman of the Provincial or Municipal People's Committees directly under the Central Government prescribes the start and end times of the tax payment season and announces it to the public.

In special cases where the agricultural land use tax records for 1994 have not been completed by the first tax payment period, the Ministry of Finance will guide temporary collection procedures, which will be finalized according to the agricultural land use tax records at the end of 1994.

Thus, agricultural land use tax is paid once or twice a year depending on the main crop of each type of plant in each locality.

Taxpayers can pay the tax before the due date, and during the first collection, they can pay the entire annual tax amount.

What types of land are subject to agricultural land use tax in Vietnam?

According to Article 2 of the Agricultural Land Use Tax Law 1993 and Article 2 of Decree 74-CP of 1993, the types of land subject to agricultural land use tax include:

- Croplands: lands for annual crops, perennial crops, and grasslands.

- Land for annual crops: land for crops with a growth period (from planting to harvest) not exceeding 365 days such as rice, corn, vegetables, peanuts, or crops harvested multiple times without undergoing a basic construction period like sugarcane, banana, reed, sisal, lemongrass, pineapple.

- Land for perennial crops: land for crops with a growth cycle exceeding 365 days, planted once but harvested over many years and requiring a basic construction period like rubber, tea, coffee, oranges, tangerines, longans, oil palms, coconuts.

- Grassland: lands already utilized for growing grass to raise livestock.

- Aquaculture areas: lands specifically used for aquaculture or both aquaculture and cropping, but not used for any other purposes.

- Plantation land: lands that have been forested and assigned to organizations or individuals for management, care, and exploitation, excluding bare hills and mountains.

Owners of tax-liable lands under this provision are required to pay taxes even if the land is not currently in use.