Where to download Form 09-MST notice of taxpayer’s relocation in Vietnam according to Circular 86?

Where to download Form 09-MST notice of taxpayer’s relocation in Vietnam according to Circular 86?

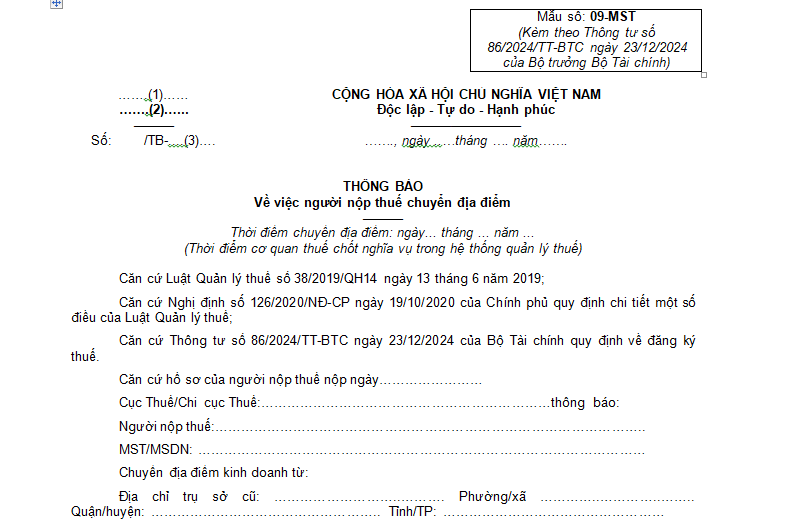

Form 09-MST is a notification form regarding the taxpayer’s change of location as stipulated in Appendix II promulgated together with Circular 86/2024/TT-BTC.

Form 09-MST notice of taxpayer’s relocation is as follows:

Download Form 09-MST notice of taxpayer’s relocation here....

Where to download Form 09-MST notice of taxpayer’s relocation in Vietnam according to Circular 86? (Image from the Internet)

How to change tax registration information for household and individual businesses in Vietnam from February 6, 2025?

Pursuant to Article 25 of Circular 86/2024/TT-BTC (effective from February 6, 2025), the procedures for changing tax registration information for household and individual businesses are as follows:

(1) Business households, family households, individual businesses changing tax registration information without changing the tax authority directly managing them

- Business household tax registration must follow the one-stop-shop interconnection mechanism when there are changes in tax registration information and must change tax registration information in conjunction with changes to business registration with the business registration authority.

- Family households, individuals operating in production, trade of goods, services according to government regulations but are not required to register business households through the business registration authority in accordance with the Government of Vietnam regulations on business households; individual businesses from countries sharing a land border with Vietnam undertaking buying, selling, exchanging goods at border markets, border gate markets, markets within border economic zones must submit the necessary documentation to change tax registration information to the directly managing tax authority, documents include:

+ Adjustment and supplementary declaration form of tax registration information, Form No. 08-MST issued together with Circular 86/2024/TT-BTC.

+ A copy of the valid passport of individuals if there is a change in information on this document for individual businesses falling under the case where the tax authority issues tax codes under the provisions at point a, clause 4, Article 5 of Circular 86/2024/TT-BTC.

(2) Business households with tax registration under the one-stop-shop interconnection mechanism changing their head office address to another province or centrally-run city, or changing the head office address to another district within the same province or centrally-run city resulting in a change in the directly managing tax authority should proceed as follows:

- At the place of departure

+ Adjustment and supplementary declaration form of tax registration information, Form No. 08-MST issued together with Circular 86/2024/TT-BTC.

+ After receiving the notice of taxpayer’s relocation, Form No. 09-MST issued together with Circular 86/2024/TT-BTC from the tax authority at the departing location, the business household must proceed with registering the change of head office address at the business registration authority in accordance with legal regulations on business household registration.

(3) Family households and individuals engaged in the production and trading of goods and services according to legal regulations but not required to register business households through the business registration authority in accordance with the Government of Vietnam regulations about business households; individual businesses from countries sharing a land border with Vietnam that engage in buying, selling, exchanging goods at border markets, border gate markets, markets within border economic zones when changing the head office address to another province or centrally-run city or another district within the same province or centrally-run city resulting in a change in the directly managing tax authority

- At the place of departure

+ Adjustment and supplementary declaration form of tax registration information, Form No. 08-MST issued together with Circular 86/2024/TT-BTC.

- At the place of arrival

+ Documentation for location change registration at the tax authority where the taxpayer relocates, Form No. 30/DK-TCT issued together with Circular 86/2024/TT-BTC.

(4) For individuals as defined at points k, l, n clause 2 Article 4 Circular 86/2024/TT-BTC when there is a change in their tax registration information and that of their dependents (including cases where the direct managing tax authority changes) must submit documentation to the income payer or to the Tax Department, Regional Tax Department where the individual is permanently or temporarily registered (in case the individual neither works nor authorizes the income payer to register) as follows:

- Documentation for changes in tax registration information when submitted through the income payer includes:

+ Power of Attorney form No. 41/UQ-DKT issued together with Circular 86/2024/TT-BTC (if there has been no prior authorization document to the income payer).

In case the individual or their dependents fall under the category where the tax authority issues tax codes as per point a, clause 4 Article 5 of Circular 86/2024/TT-BTC, a copy of the passport with changes related to tax registration information of the individual or their dependents must be submitted.

The income payer is responsible for compiling individual information changes into the tax registration Form No. 05-DK-TH-TCT, changes in dependent information into the tax registration Form No. 20-DK-TH-TCT issued together with Circular 86/2024/TT-BTC to send to the tax authority managing the income payer directly.

- Documentation for changes in tax registration information when submitted directly to the tax authority includes:

+ Adjustment and supplementary declaration form of tax registration information, Form No. 08-MST or Form No. 20-DK-TCT issued together with Circular 86/2024/TT-BTC.

In case the individual or their dependents fall under the category where the tax authority issues tax codes as per point a, clause 4 Article 5 of Circular 86/2024/TT-BTC, a copy of the individual or dependent's valid passport with relevant changes to tax registration information must be submitted.

(5) For taxpayers who are foreign individuals not residing in Vietnam as defined at point e, clause 2 Article 4 Circular 86/2024/TT-BTC directly registering as taxpayers, they must submit documentation to change tax registration information in accordance with regulations under the Ministry of Finance's Circular guiding certain provisions of the Law on Tax Administration.

How long shall taxpayers notify tax authorities of a change in tax registration information in Vietnam?

Pursuant to Article 36 of The Tax Management Law 2019, taxpayers must notify tax authorities of changes in tax registration information within the following time frame:

- Taxpayers registering business, cooperatives, business households when there is a change in tax registration information must notify the change of tax registration information along with the change of business registration, cooperative registration, business registration according to legal regulations.

In cases where the taxpayer’s head office address changes leading to a change in the managing tax authority, the taxpayer must complete tax procedures with the directly managing tax authority as stipulated by this Law before registering for information change with the business registration, cooperative registration, business registration authority.

- Taxpayers who directly register with tax authorities must notify the direct managing tax authority within 10 working days from when the change in information occurs if there is any change in tax registration information.

- In cases where an individual authorizes an organization or individual paying income to register the change in tax registration information on behalf of the individual and their dependents, they must notify the income payer, individual no later than 10 working days from the day the change occurs; the income payer, individual must notify the tax management authority no later than 10 working days from when they receive the individual’s authorization.