When is the public property electronic sales invoice used in Vietnam?

When is the public property electronic sales invoice used in Vietnam?

Based on Clause 3 Article 8 of Decree 123/2020/ND-CP, regulations are as follows:

Invoice Types

Invoices stipulated in this Decree include the following types:

1. Value-added tax invoice is an invoice dedicated for organizations declaring value-added tax using the credit method for the following activities:

a) Sale of goods, provision of services domestically;

b) International transportation activities;

c) Export to non-tariff zones and cases considered as export;

d) Export of goods, provision of services abroad.

2. Sales invoice is an invoice for organizations and individuals as follows:

a) Organizations and individuals declaring and calculating value-added tax using the direct method for the following activities:

- Sale of goods, provision of services domestically;

- International transportation activities;

- Export to non-tariff zones and cases considered as export;

- Export of goods, provision of services abroad.

b) Organizations and individuals in non-tariff zones when selling goods, providing services domestically, and when selling goods and providing services between organizations and individuals in non-tariff zones with each other, exporting goods, providing services abroad, with invoices clearly stating “For organizations and individuals in non-tariff zones.”

3. The public property electronic sales invoice is used when selling the following assets:

a) Public assets at agencies, organizations, units (including state-owned houses);

b) Infrastructure assets;

c) Public assets assigned by the State to enterprises for management not included as state capital in the enterprise;

d) Assets of projects using state capital;

đ) Assets confirmed as national public ownership;

e) Public assets recovered according to decisions of competent authorities or persons;

g) Materials and supplies recovered from handling public assets.

4. Electronic invoices for selling national reserve stocks are used when agencies or units within the national reserve system sell national reserve stocks as regulated by law.

5. Other types of invoices include:

a) Stamps, tickets, and cards with form and content stipulated in this Decree;

b) Air fare receipts; international transportation fee receipts; banking service fee receipts unless otherwise specified in point a of this clause with form and content generated according to international practices and relevant legal provisions.

6. Documents printed, issued, used, and managed like invoices include internal transfer notes and delivery notes for goods sent to agencies.

7. The Ministry of Finance provides guidance on invoice display templates for entities enumerated in Article 2 of this Decree for reference in implementation.

Thus, according to the above regulation, the public property electronic sales invoice is used in the following cases:

[1] Public assets at agencies, organizations, units (including state-owned houses);

[2] Infrastructure assets;

[3] Public assets assigned by the State to enterprises for management not considered part of state capital within enterprises;

[4] Assets of projects using state capital;

[5] Assets established under national public ownership status;

[6] Public assets recovered according to decisions of competent authorities or persons;

[7] Materials and supplies recovered from handling public assets.

When is the public property electronic sales invoice used in Vietnam? (Image from the Internet)

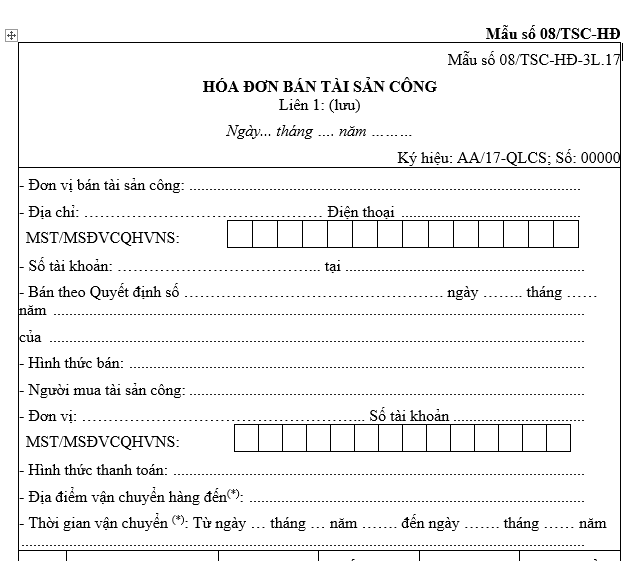

What is the current form of the public property electronic sales invoice in Vietnam?

According to the Appendix issued with Decree 123/2020/ND-CP, the current template for the public property electronic sales invoice is Template No. 08/TSC-HD, specifically as follows:

Download Current template for selling public asset electronic invoice.

What is the content of the public property electronic sales invoice in Vietnam?

According to Clause 16, Article 10 of Decree 123/2020/ND-CP, regulations are as follows:

Invoice Content

1. Name of the invoice, invoice sign, invoice template number. Specifically as follows:

a) The invoice name is the name of each invoice type specified in Article 8 of this Decree, as shown on each invoice, such as: VALUE-ADDED TAX INVOICE, VALUE-ADDED TAX INVOICE WITH TAX REFUND DECLARATION, VALUE-ADDED TAX INVOICE WITH RECEIPT, SALES INVOICE, PUBLIC ASSET SALES INVOICE, STAMP, TICKET, CARD, NATIONAL RESERVE SALES INVOICE.

...

14. Some cases where electronic invoices do not necessarily have all contents.

..

k) For construction, installation, production activities, defense security product supply of defense security enterprises serving national defense security activities per Vietnam Government regulations, the invoice may not necessarily include measurement units, quantity, unit price; goods and service names are recorded as supplying goods and services in accordance with contracts signed between parties.

15. Other content on invoices

Beyond the guidelines from clause 1 to clause 13 of this Article, businesses, organizations, households, and business individuals can add information about symbols or logos to display the seller's brand or representative image. Depending on the characteristics, nature of the transaction, and management requirements, invoices can include information about sales contracts, shipping orders, customer codes, and other information.

16. The content of the invoice for selling public assets follows the guidelines for preparing public asset sales invoices according to Template No. 08/TSC-HD issued along with Decree No. 151/2017/ND-CP dated December 26, 2017 of the Government of Vietnam detailing some articles of the Law on Management and Use of Public Property.

Thus, the content of the public asset sales invoice is prepared following the guidelines for the public asset sales invoice according to Template No. 08/TSC-HD Download.