When a business ceases operations, shall resource royalty finalization be declared annually or monthly in Vietnam?

When a business ceases operations, shall resource royalty finalization be declared annually or monthly in Vietnam?

Based on point a, clause 6, Article 8 of Decree 126/2020/ND-CP, it is stipulated as follows:

Taxes declared monthly, quarterly, annually, separately, or for tax finalization

...

6. Types of taxes and fees for annual finalization and finalization up to the time of dissolution, bankruptcy, cessation of operations, contract termination, or business reorganization. In cases of business type conversion (excluding the equitization of state-owned enterprises) where the converting enterprise inherits all tax obligations of the converted enterprise, finalization up to the decision on conversion is not required; the enterprise finalizes at the year's end. Specifically:

a) Resource royalty.

...

Thus, according to the legal regulation, when ceasing operations, businesses must declare Resource royalty finalization on an annual basis.

Additionally, the procedure for declaring Resource royalty finalization should follow the guidance on the National Public Service Portal and clause 3, Article 15 of Circular 80/2021/TT-BTC as follows:

- Step 1: Organizations and individuals exploiting natural resources prepare Resource royalty finalization documents and submit them to their direct managing tax authority.

In cases where organizations and individuals, whose headquarters are in one province or city but engage in resource exploitation activities in others, should file their tax declaration documents at the Tax Department or Sub-department as determined by the Director of the Tax Department where the exploitation occurs.

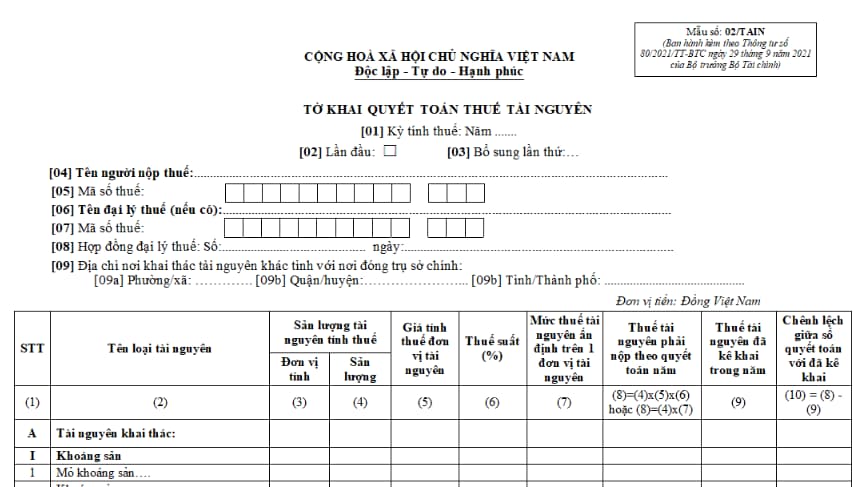

Organizations and individuals with hydropower production plants must prepare the Resource royalty finalization documents using Form No. 02/TAIN in Appendix 2 attached to Circular 80/2021/TT-BTC (Download), and submit them to the tax authority managing state budget revenues where the water resource exploitation activity occurs.

In cases where organizations and individuals engage in hydropower production but the hydropower plant’s reservoirs are located across multiple provinces, they should submit the Resource royalty finalization documents and the annex of tax allocation to the tax authority where the plant's head office is and pay allocated taxes to the provinces where the reservoirs are according to the regulations.

Deadline for submission: No later than the last day of the third month after the end of the calendar year or fiscal year, or the 45th day after ceasing operations, terminating contracts, or reorganizing businesses.

- Step 2. The tax authority acknowledges:

The tax authority handles and processes the submitted documents as per regulations, whether they are filed directly, sent via postal services, or submitted electronically through e-transactions on the Tax Department’s electronic portal or authorized state agency, or service provider T-VAN.

Additionally, the entity performing this can choose one of the following methods:

- Direct submission at the tax office headquarters;

- Or send via postal services;

- Or submit electronic documents through e-transactions to the tax office (via the electronic portal of the General Department of Taxation/competent state agency or service provider T-VAN).

Is it necessary to declare tax finalization at the end of the year if the enterprise inherits all tax obligations? (Image from the Internet)

What does the resource royalty finalization for resource exploitation establishments include?

Based on sub-item 5.2, Item 5, Appendix 1 attached to Decree 126/2020/ND-CP, the Resource royalty finalization for resource exploitation establishments includes:

- Resource royalty finalization declaration form No. 02/TAIN (Download) in Appendix 2 attached to Circular 80/2021/TT-BTC

- Annex for allocating the Resource royalty payable to localities entitled to the revenue from hydropower production - Form No. 01-1/TAIN (Download) attached to Circular 80/2021/TT-BTC

What is the latest resource royalty finalization form in Vietnam for 2025?

Currently, the Resource royalty Finalization Declaration Form is No. 02/TAIN in Appendix 2 attached to Circular 80/2021/TT-BTC. Specifically:

Download the Resource royalty Finalization Declaration Form

What Are the Bases for Resource royalty Calculation?

According to Article 4 of the Resource royalty Law 2009, it is stipulated as follows:

Bases for Tax Calculation

The bases for Resource royalty calculation are taxable resource output, taxable value, and tax rate.

Referencing Article 4 of Circular 152/2015/TT-BTC, it provides specific guidance as follows:

- The bases for Resource royalty calculation are taxable resource output, Resource royalty price, and Resource royalty rate.

- Determine the payable Resource royalty in the period:

Payable Resource royalty in the period = Taxable resource output x Taxable unit price x Resource royalty rate

+ In cases where the state authority sets the payable Resource royalty rate on a unit of extracted resource, the payable Resource royalty is calculated as follows:

Payable Resource royalty in the period = Taxable resource output x Set Resource royalty rate on a unit of extracted resource

The setting of Resource royalty is based on the data from the Tax Authority, in compliance with the regulations for tax determination under tax administration laws.