What is the TIN reactivation notice form in Vietnam under the Circular 86? What are procedures for processing TIN reactivation applications for organizations and delivering result in Vietnam?

What are cases of TIN reactivation in Vietnam?

Pursuant to Clauses 1 and 2 of Article 40 of the Law on tax administration 2019, taxpayers can have their TINs reactived in the following cases:

- Taxpayers registered alongside with business registration, cooperative registration, or business operation registration. If the legal status is reactived according to law regarding business registration, cooperative registration, or business registration, the TIN will concurrently be reactived.

- Taxpayers who are registered directly with a tax authority submit a application requesting the reactivation of the TIN to the tax authority managing them directly in the following cases:

+ A competent authority issues a document canceling the revocation of the business registration certificate or equivalent license;

+ Continued business operation is desired after a application terminating the TIN's validity has been submitted but the tax authority has not yet issued a termination notice;

+ The tax authority issues a notice of taxpayer inactivity at the registered address, but the business license has not been revoked and the TIN's validity has not been terminated.

Circular 86: What is the TIN reactivation notice form in Vietnam?

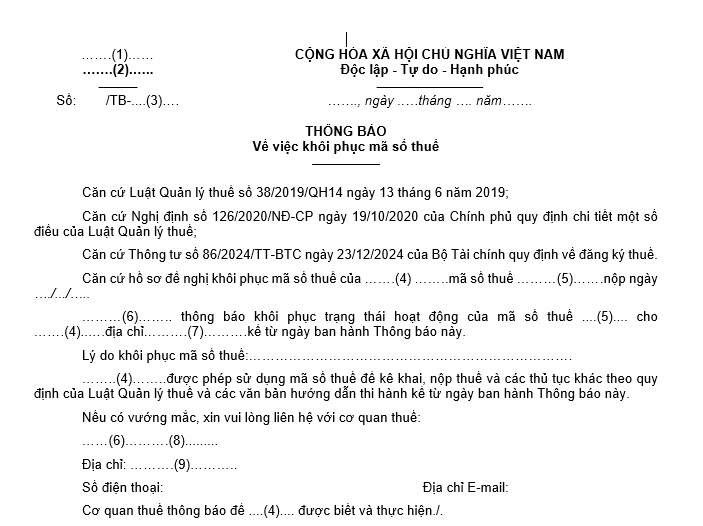

The TIN reactivation notice form is applied according to form 19/TB-DKT in Appendix 2 of the list of forms issued with Circular 86/2024/TT-BTC. The form is as follows:

Download the TIN reactivation notice form HERE.

Included within:

(1): Name of higher tax authority

(2): Name of lower tax authority

(3): CT (Tax Department) or CCT (Sub-department of Taxation)

(4): Taxpayer's name

(5): Business code/TIN of the taxpayer

(6): Name of tax authority issuing the notice

(7): Address of the taxpayer

(8): Department where the taxpayer can make contact

(9): Specify the address of the issuing tax authority

(10): Head of the tax authority or authorized representative as per regulations

Circular 86: What is the TIN reactivation notice form in Vietnam? (Image from the Internet)

What are procedures for processing TIN reactivation applications for organizations and delivering result in Vietnam?

According to Article 19 of Circular 86/2024/TT-BTC, the procedures for processing TIN reactivation applications for organizations and delivering results are divided into 2 cases as follows:

Case 1: For taxpayer applications

(1) Handling taxpayer TIN reactivation applications as stipulated in point a, Clause 1, Article 18 of Circular 86/2024/TT-BTC:

- Within 03 (three) working days from the date of receiving a complete application requesting TIN reactivation as per regulations, the tax authority shall:

+ Draft a Notice on the TIN reactivation form 19/TB-DKT, a Notice on the reactived TIN for managing entities, form 37/TB-DKT (if applicable) issued with Circular 86/2024/TT-BTC to be sent to taxpayers and subordinate units (if the TIN reactived belongs to the managing entity).

+ Reprint the taxpayer registration certificate or TIN notice for taxpayers if they have submitted the original to the tax authority with the application terminating the TIN's validity.

+ Update the taxpayer's TIN status on the taxpayer registration application system on the working day or at the latest by the next working day from the issuance of the Notice on TIN reactivation.

If the taxpayer's TIN status had been updated to '06' by the tax authority, on-site verification at the registered office address similar to Clause (2) is required before TIN reactivation.

(2) Handling taxpayer TIN reactivation applications as stipulated in point b, Clause 1, Article 18 of Circular 86/2024/TT-BTC:

- Within 10 working days from the date of receiving a complete application requesting TIN reactivation as per regulations, the tax authority compiles a list of outstanding tax declarations, invoice usage status, tax liabilities and other budgetary debts, and enforces penalties for tax and invoice violations up to the time the taxpayer submits the request for TIN reactivation, while also verifying the actual operational status at the business's registered office address and drafting the Verification Record form 15/BB-XMHĐ issued with Circular 86/2024/TT-BTC as per the reactivation request application (the taxpayer must sign to confirm the Verification Record).

In cases where the taxpayer has dependent units, the managing entity's tax authority notifies the dependent unit's tax authority to ensure tax obligations are fulfilled prior to TIN reactivation. If the dependent unit cannot meet tax obligations, the managing entity is responsible for fulfilling them before said reactivation.

- If the taxpayer changes the office address without registering the change with the tax authority or business registration authority, and if the taxpayer submits complete and conformable information change documentation, the tax authority will verify the actual operational status at the new office address as follows:

+ If the taxpayer's operational address is within the jurisdiction of the managing tax authority: the tax authority operates as per Clause (2.1).

+ If the operational address is outside the jurisdiction of the managing tax authority: The outgoing tax authority sends a request to the incoming tax authority to cooperate with local authorities for verification, drafting, and result submission to the outgoing tax authority.

+ For businesses, cooperatives, or joint-ventures registered under a one-stop-shop procedure with business registration that changed addresses but did not register this change with the business registration authority, the tax authority will assess risk to decide on verification at the new address or notify non-reactivation as stipulated in Clause (4).

- Within 03 working days from when the taxpayer complies with all administrative tax and invoice violations, and pays all tax liabilities and other state budget debts (including subordinate unit obligations, if applicable, except for cases exempted under Clause 4, Article 6 of Decree 126/2020/ND-CP), the tax authority shall:

+ Draft a Notice on TIN reactivation form 19/TB-DKT, a Notice on the reactived TIN for managing entities form 37/TB-DKT (if applicable) issued with Circular 86/2024/TT-BTC, sending it to taxpayers and subordinate units (if the TIN reactived belongs to the managing entity).

+ Update the taxpayer's TIN status on the taxpayer registration application system on the working day or at the latest by the next working day from the issuance of the Notice on TIN reactivation. For businesses, cooperatives, joint ventures, and their subdivisions, reactived TINs are updated to match the legal status in the national business registration information system upon ceasing the "Inactive at the registered address" status.

The tax authority publicly posts the Notice on TIN reactivation on the Tax Department's Electronic Portal as stipulated in Article 22 of Circular 86/2024/TT-BTC. Local State Management Agencies (including Customs, Business Registration Authorities (except for interlinked business and taxpayer registrations), Procuracy, Police, Market Management Authority, Establishment and Operating License-granting Agencies), and other organizations or individuals are responsible for consulting published taxpayer status and information for state management and other purposes.

(3) Handling taxpayer TIN reactivation applications as stipulated in points c, d, Clause 1, Article 18 of Circular 86/2024/TT-BTC

Within 10 working days from receiving a complete application requesting TIN reactivation according to regulations, the tax authority compiles a list of outstanding tax declarations, invoice usage status, tax liabilities, and other state budget dues, and enforces penalties for tax and invoice violations up to when the taxpayer submits the request for reactivation.

Within 03 working days from the taxpayer's compliance with all administrative tax and invoice violations, and payment of all tax liabilities and other state budget debts (except for exceptions in Clause 4, Article 6 of Decree 126/2020/ND-CP), the tax authority shall:

- Draft a Notice on TIN reactivation form 19/TB-DKT, a Notice on the reactived TIN for managing entities form 37/TB-DKT (if applicable) issued with Circular 86/2024/TT-BTC, sending it to taxpayers and subordinate units (if the code reactived is the managing entity).

- Reprint the taxpayer registration certificate or TIN notice for taxpayers in cases where the original was submitted as part of the TIN termination application.

- Update the taxpayer's TIN status on the taxpayer registration application system instantly or at latest by the next working day's start from issuing the Notice on TIN reactivation.

If the taxpayer's TIN had been updated to status '06', the tax authority must conduct verification at the registered office address per point b before reactivation.

(4) Tax authorities issue a Notice on non-reactivation of TINs form 38/TB-DKT with Circular 86/2024/TT-BTC to the taxpayer in the following cases:

- Taxpayers submit incomplete applications or those ineligible for TIN reactivation under Clause 1, Article 18 of Circular 86/2024/TT-BTC.

- Taxpayers fail to fulfill tax and invoice obligations to the tax authority within 30 days from notice listing missing declarations, invoice status, tax liabilities and state budget dues, including penalties as per points (2) and (3), without justification as outlined in Clause 4, Article 6 of Decree 126/2020/ND-CP.

- Taxpayers needing verification of operational status at registered addresses for reactivation as in points (1), (2), and (3), but verification shows non-operation or unapproved changes by tax authorities; or enterprises, cooperatives undertak risk assessment refusing reactivation at new addresses.

Case 2: Processing TIN reactivation applications for Enterprises, Cooperatives, Partnerships with Legal Status reactived per Law on Business and Cooperative Registration:

- Upon receiving information reactiving legal status for enterprises, cooperatives, partnerships, and dependants, the tax authority reactives the taxpayer's code the same day the National Business Registration System information is received.

- If the taxpayer has a non-operation notice at a registered address, the tax authority updates status to '06' reasons. After receiving the taxpayer's submission per point b, Clause 1, Article 18 Circular 86/2024/TT-BTC, further processing respectively follows point (2).