What is the time limt for a taxpayer registered directly with the tax authority to notify changes in taxpayer registration information in Vietnam?

What is the time limt for a taxpayer registered directly with the tax authority to notify changes in taxpayer registration information in Vietnam?

According to Article 36 of the 2019 Law on Tax Administration, the regulations are as follows:

Notification of Changes in Taxpayer Registration Information

1. A taxpayer registered for taxpayer registration along with business registration, cooperative registration, or enterprise registration must notify changes in taxpayer registration information concurrently with changes in business registration, cooperative registration, or enterprise registration as per legal regulations.

In cases where the taxpayer changes the address of their headquarters leading to a change in the managing tax authority, the taxpayer must complete tax procedures with the directly managing tax authority according to this Law before registering changes in information with the business registration, cooperative registration, or enterprise registration authorities.

2. A taxpayer registered directly with the tax authority must notify the directly managing tax authority within 10 working days from the date the information change arises.

3. In cases where an individual authorizes an organization or individual paying income to register the change of taxpayer registration information for the individual and their dependents, they must notify the organization or individual paying income no later than 10 working days from the date the information change arises; the organization or individual paying income is responsible for notifying the managing tax authority no later than 10 working days from receiving the individual's authorization.

A taxpayer registered directly with the tax authority must notify the directly managing tax authority within 10 working days from the date the change in taxpayer registration information arises.

Thus, a taxpayer registered directly with the tax authority must notify within 10 working days.

What is the time limt for a taxpayer registered directly with the tax authority to notify changes in taxpayer registration information in Vietnam? (Image from the Internet)

What is the location to submit and the dossier for changes in taxpayer registration information in Vietnam?

According to Article 10 of Circular 105/2020/TT-BTC, the location for submission and the dossier for changes in taxpayer registration information are carried out according to Article 36 of the 2019 Law on Tax Administration and the following regulations:

(1). Change in taxpayer registration information without changing the directly managing tax authority

* Taxpayers as specified in points a, b, c, d, đ, e, h, i, n, Clause 2, Article 4 of Circular 105/2020/TT-BTC shall submit dossiers to the directly managing tax authority as follows:

- The dossier for changes in taxpayer registration information for taxpayers as specified in points a, b, c, đ, h, n, Clause 2, Article 4 of Circular 105/2020/TT-BTC includes:

+ Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC;

+ A copy of the Establishment and Operation License, or Certificate of Registration of dependent units, or Establishment Decision, or equivalent License issued by competent authorities if the information on these documents changes.

- The dossier for changes in taxpayer registration information for taxpayers as per point d, Clause 2, Article 4 of Circular 105/2020/TT-BTC includes: Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC.

- The dossier for changes in taxpayer registration information for foreign suppliers as specified in point e, Clause 2, Article 4 Circular 105/2020/TT-BTC shall be implemented according to the circular of the Ministry of Finance guiding certain provisions of the 2019 Law on Tax Administration.

- The dossier for changes in taxpayer registration information for business households, individual businesses as specified in point i, Clause 2, Article 4 of Circular 105/2020/TT-BTC, includes:

+ Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC or tax declaration dossiers according to tax management laws;

- A copy of the Business Registration Certificate if there is any change in the information on the Business Registration Certificate;

+ A copy of the Identity Card or a valid Citizen Identification Card for individuals with Vietnamese nationality; a valid Passport for individuals with foreign nationality and Vietnamese nationals residing abroad if there is any change in the information on these documents.

* Taxpayers who are contractors or investors in oil and gas contracts specified in point h, Clause 2, Article 4 of Circular 105/2020/TT-BTC when transferring capital contributions in economic organizations or transferring part of the interests in oil and gas contracts, must submit dossiers for changes in taxpayer registration information at the Tax Department where the operator is headquartered.

The dossier for changes in taxpayer registration information includes a Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC.

(2). Change in taxpayer registration information leading to a change in the directly managing tax authority

* Taxpayers registered for taxpayer registration along with business registration, cooperative registration, or enterprise registration, when transferring the head office address to another centrally-administered city or province or to another district within the same centrally-administered city or province leading to a change in the directly managing tax authority.

Taxpayers must submit dossiers for changes to the directly managing tax authority (where the tax is transferred) to complete tax procedures before registering head office address changes with the business registration or cooperative registration authority.

The dossier submitted to the tax authority at the place of departure includes a Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC.

Upon receiving the Notice of Location Transfer form 09-MST issued with Circular 105/2020/TT-BTC from the departing tax authority, the enterprise or cooperative executes the registration to change the head office address at the business registration authority or cooperative registration following the legal provisions on business registration and cooperative registration.

* Taxpayers subject to direct taxpayer registration with the tax authority according to points a, b, c, d, đ, h, i, n, Clause 2, Article 4 of Circular 105/2020/TT-BTC when transferring the headquarters address to another centrally-administered city or province, or transferring to another district but within the same centrally-administered city or province leading to a change in the directly managing tax authority shall proceed as follows:

- At the tax authority at the place of departure

Taxpayers shall submit dossiers for changes in taxpayer registration information to the directly managing tax authority (where the tax is transferred). The dossier for changes in taxpayer registration information is as follows:

+ For taxpayers according to points a, b, c, đ, h, n, Clause 2, Article 4 of Circular 105/2020/TT-BTC, includes:

++ Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC;

++ A copy of the Establishment and Operation License, or Business Registration Certificate or equivalent document issued by the competent authority if the address on these documents changes.

+ For taxpayers according to point d, Clause 2, Article 4 of Circular 105/2020/TT-BTC, includes: Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC.

+ For business households, individual businesses according to point i, Clause 2, Article 4 of Circular 105/2020/TT-BTC, includes:

++ Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC or tax declaration dossiers according to legal regulations for tax management;

++ A copy of the Business Registration Certificate issued by a competent authority at the new address (if available);

++ A copy of the Citizen Identification Card or valid Identity Card for individuals with Vietnamese nationality; a valid Passport for individuals with foreign nationality or Vietnamese nationals residing abroad in cases where there is a change in taxpayer registration information on these documents.

- At the tax authority at the new location

+ Taxpayers shall submit dossiers for changes in taxpayer registration information at the tax authority at the new location within 10 (ten) working days from the date the tax authority at the departure issues a Notice of Location Transfer form 09-MST issued with Circular 105/2020/TT-BTC. Specifically:

++ Taxpayers according to points a, b, d, đ, h, n, Clause 2, Article 4 of Circular 105/2020/TT-BTC shall submit dossiers at the Tax Department at the new headquarters.

++ Taxpayers who are cooperative alliances according to point b, Clause 2, Article 4 of Circular 105/2020/TT-BTC shall submit dossiers at the Regional Tax Branch or Tax Sub-department at the new headquarters.

++ Taxpayers according to point c, Clause 2, Article 4 of Circular 105/2020/TT-BTC shall submit dossiers at the Tax Department where they are headquartered (organizations established by central and provincial authority decisions); at the Tax Branch or Regional Tax Branch where they are headquartered (organizations established by district authority decisions).

+ Business households, individual businesses according to point i, Clause 2, Article 4 of Circular 105/2020/TT-BTC shall submit dossiers at the Tax Branch or Regional Tax Branch where the new business location is.

+ The dossier for changes in taxpayer registration information includes:

+ Registration document for location transfer at the tax authority where the taxpayer moves to form 30/DK-TCT issued with Circular 105/2020/TT-BTC.

+ A copy of the Establishment and Operation License, or Business Registration Certificate or equivalent document issued by competent authorities in case there is a change in the address on these documents.

(3). Taxpayers who are individuals according to points k, l, n, Clause 2, Article 4 of Circular 105/2020/TT-BTC with changes in taxpayer registration information for themselves and their dependents (including changes leading to a change in the directly managing tax authority) shall submit dossiers either through the income-paying organization or directly at the Tax Branch, Regional Tax Branch where the individual is registered for permanent or temporary residence (if the individual does not work at an income-paying organization) as follows:

* The dossier for changes in taxpayer registration information in case of submission through an income-paying organization includes: Authorization document (if there was no prior authorization for the income-paying organization) and copies of documents with changes related to the taxpayer registration information of the individual or dependents.

The income-paying organization shall aggregate the change information for individuals or dependents into the Declaration forms 05-DK-TH-TCT or 20-DK-TH-TCT issued with Circular 105/2020/TT-BTC and send it to the directly managing tax authority of the income-paying organization.

* The dossier for changes in taxpayer registration information in the case of direct submission at the tax authority includes:

- Declaration form for adjustment and supplementation of taxpayer registration information form 08-MST issued with Circular 105/2020/TT-BTC;

- A copy of the Citizen Identification Card or valid Identity Card for dependents with Vietnamese nationality; a valid Passport for dependents with foreign nationality or Vietnamese nationals living abroad in cases where there is a change in taxpayer registration information on these documents.

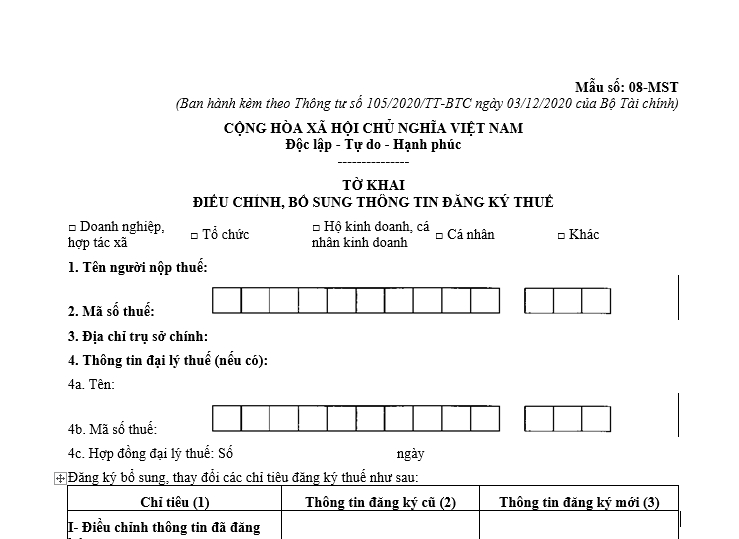

Which form is used for amending and supplementing taxpayer registration information in Vietnam?

The form for amending and supplementing taxpayer registration information is Form 08-MST issued with Circular 105/2020/TT-BTC.

Download the form for amending and supplementing taxpayer registration information.