What is the teacher payroll in Vietnam in 2025? When do teachers teaching in public schools pay PIT in Vietnam?

What is the teacher payroll in Vietnam in 2025?

Based on Clause 2, Article 3 of Decree 73/2024/ND-CP, the statutory pay rate for public employees is stipulated as follows:

Statutory Pay Rate

...

- From July 1, 2024, the statutory pay rate is 2,340,000 VND/month.

...

However, based on Clause 1, Article 3 of Resolution 159/2024/QH15 regarding the implementation of salary policy as follows:

On Implementing Salary Policy and Certain Social Policies

- No increase in public sector salaries, pensions, social insurance allowances, monthly allowances, and preferential allowances for people with meritorious services in 2025.

....

Additionally, based on Article 3 of Circular 07/2024/TT-BNV, the statutory pay rate for teachers teaching in public schools is calculated as follows:

| Salary Level = Statutory Pay Rate x Current Salary Coefficient |

Thus, in 2025, there will be no increase in public sector salaries, meaning the statutory pay rate for teachers teaching in public schools in 2025 will remain at 2,340,000 VND/month.

Consequently, the 2025 teacher payroll is determined as follows:

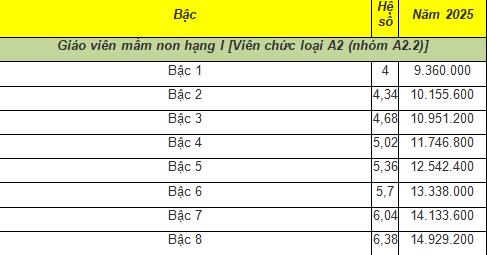

2025 teacher payroll: Preschool Teachers as per Circular 01/2021/TT-BGDDT

Download View the full 2025 salary schedule: Preschool Teachers.

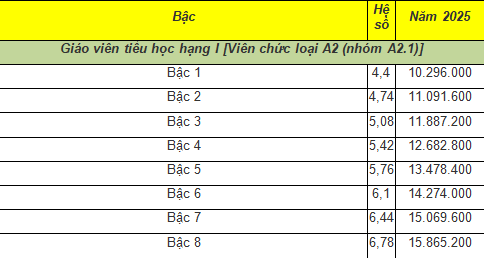

2025 teacher payroll: Primary School Teachers as per Circular 02/2021/TT-BGDDT

Download View the full 2025 salary schedule: Primary School Teachers.

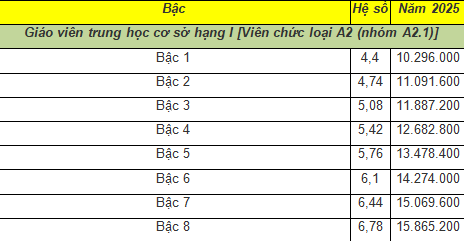

2025 teacher payroll: Lower Secondary School Teachers as per Circular 03/2021/TT-BGDDT

Download View the full 2025 salary schedule: Lower Secondary School Teachers.

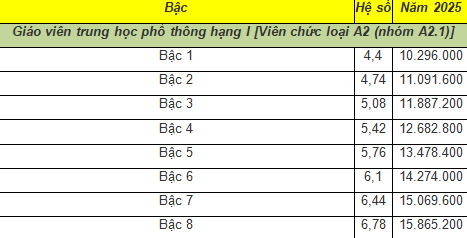

2025 teacher payroll: Upper Secondary School Teachers as per Circular 04/2021/TT-BGDDT

Download View the full 2025 salary schedule: Upper Secondary School Teachers.

Note: The above salary tables do not include allowances, bonuses, and other stipends!

What is the teacher payroll in Vietnam in 2025? When do teachers teaching in public schools pay PIT in Vietnam? (Image from the Internet)

When do teachers teaching in public schools pay PIT in Vietnam?

Based on Clause 2, Article 2 of Circular 111/2013/TT-BTC which stipulates taxable PIT income as follows:

Taxable Income

…

2. Income from salaries and wages

Income from salaries and wages is the income an employee receives from an employer, including:

a) Salaries, wages, and amounts of a salary or wage nature in any form, monetary or non-monetary.

b) Allowances and stipends, excluding the following:

b.1) Monthly preferential stipends and one-time allowances as prescribed by law for people with meritorious services.

…

Additionally, based on Article 1 of Resolution 954/2020/UBTVQH14 stipulating the family circumstance deduction as follows:

Family Circumstance Deduction

Adjusts the family circumstance deduction specified in Clause 1, Article 19 of the Law on Personal Income Tax No. 04/2007/QH12, as amended by Law No. 26/2012/QH13 as follows:

1. Deduction level for taxpayers is 11 million VND/month (132 million VND/year);

2. Deduction level for each dependent is 4.4 million VND/month.

Thus, income from salaries and wages of teachers teaching in public schools in Vietnam will be subject to PIT as regulated.

To be specific, teachers teaching in public schools must pay PIT when their salary reaches:

- Above 11 million VND/month for those without any dependents

- Above 15.4 million VND/month if registering for a family circumstance deduction for 01 dependent, and incrementally increasing with additional dependents.

Note: Income from salaries and wages mentioned above has deducted mandatory insurance contributions and other contributions like charity, humanitarian aid, etc.

What are regulations on the PIT payers in Vietnam?

Based on Article 2 of the Law on Personal Income Tax 2007, the definition of PITpayers is as follows:

- Residents with taxable income generated inside and outside the territory of Vietnam

- Non-residents with taxable income generated inside the territory of Vietnam.

Additionally, residents and non-residents are defined as follows:

- A resident is an individual who meets one of the following conditions:

+ Present in Vietnam for 183 days or more calculated in a calendar year or for 12 consecutive months from the first day of presence in Vietnam;

+ Having a regular residence in Vietnam, including having a registered permanent residence or a rented house in Vietnam under a lease contract.

- A non-resident is an individual who does not meet the conditions specified in Clause 2, Article 2 of the Law on Personal Income Tax 2007.

Where to submit PIT in Vietnam?

Based on Clause 1, Article 56 of the Law on Tax Administration 2019 which stipulates where to submit PIT as follows:

- At the State Treasury;

- At the tax administration authority where tax declaration documents are received;

- Through organizations authorized by the tax administration authority to collect taxes;

- Through commercial banks, other credit institutions, and service organizations as prescribed by law.