What is the tax declaration form for individuals with income from transfer, inheritance, gifting of real estate in Vietnam?

What is the tax declaration form for individuals with income from transfer, inheritance, gifting of real estate in Vietnam?

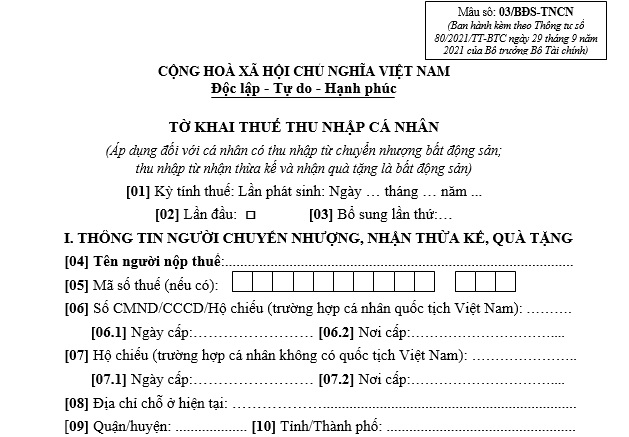

The tax declaration for individuals receiving income from the transfer, inheritance, or gifts of real estate is the Personal Income Tax Declaration Form No. 03/BDS-TNCN issued with Appendix 2 of Circular 80/2021/TT-BTC:

>> Download the tax declaration for individuals with income from the transfer, inheritance, or gifts of real estate

What are cases of tax exemption from personal income tax on real estate transfers in Vietnam?

Based on Clause 4, Article 4 of Decree 65/2013/ND-CP, the regulation on tax-exempt income is as follows:

Tax-exempt Income

1. Income from the transfer of real estate (including future housing and construction projects as regulated by real estate business laws) between: spouses; biological parents and children; adoptive parents and adopted children; parents-in-law and daughters-in-law; parents-in-law and sons-in-law; paternal grandparents and grandchildren; maternal grandparents and grandchildren; siblings.

2. Income from the transfer of housing, homestead land use rights, and assets attached to homestead land of individuals in the case where the transferor has only one house or homestead land use right in Vietnam.

Individuals transferring the only house or homestead land use right in Vietnam under this clause must meet the following conditions:

a) At the time of transfer, the individual owns or uses only one house or one lot of land (including cases where a house or construction work is attached to that lot);

b) The individual has owned or used the house or homestead land for at least 183 days by the time of transfer;

c) The house or homestead land use rights are transferred in their entirety;

The determination of ownership or use rights of the house or homestead land is based on the certificate of ownership or land use rights. Individuals owning or transferring the house or homestead land must declare and be responsible before the law for the accuracy of their declaration. If the competent authority finds false declarations, tax exemption will not be granted and penalties will be imposed according to law.

3. Income from the value of land use rights given to individuals by the State without payment or with a land levy reduction according to legal provisions.

4. Income from inherited real estate*, and gifts received as real estate (including housing and future construction projects as regulated by real estate business laws) between: spouses; biological parents and children; adoptive parents and adopted children; parents-in-law and daughters-in-law; parents-in-law and sons-in-law; paternal grandparents and grandchildren; maternal grandparents and grandchildren; siblings.*

...

Thus, individuals are exempt from personal income tax on the transfer, inheritance, or gifting of real estate in the following cases:

Transfer, inheritance, or gifting of real estate between: spouses; biological parents and children; adoptive parents and adopted children; parents-in-law and daughters-in-law; parents-in-law and sons-in-law; paternal grandparents and grandchildren; maternal grandparents and grandchildren; siblings.

What are regulations on tax period for income from real estate transfers in Vietnam?

Based on Article 7 of the Personal Income Tax Law 2007 (amended by Clause 3, Article 1 of the Amended Personal Income Tax Law 2012) which regulates the tax period as follows:

Tax Period

1. The tax period for resident individuals is regulated as follows:

a) The annual tax period applies to income from business; income from salaries and wages;

b) The tax period for each occurrence of income applies to income from capital investment; income from capital transfer, except for income from security transfer; income from real estate transfer*; income from winnings; income from royalties; income from franchising; income from inheritance; income from gifts;*

c) The tax period for each transfer or annually applies to income from security transfers.

2. The tax period for non-resident individuals is calculated for each occurrence of income for all taxable income.

Thus, according to the above regulations, the tax period for income from real estate transfers is calculated for each occurrence of income.