What is the significance of the first two digits in the TIN structure in Vietnam?

What is the significance of the first two digits in the TIN structure in Vietnam?

According to Clause 1, Article 5 of Circular 105/2020/TT-BTC, the structure of the TIN is prescribed as follows:

N1N2N3N4N5N6N7N8N9N10 - N11N12N13

In which:

- The first two digits N1N2 represent the segment number of the TIN.

- The seven digits N3N4N5N6N7N8N9 are specified by a defined structure, increasing in order from 0000001 to 9999999.

- The digit N10 is the check digit.

- The three digits N11N12N13 are the serial numbers from 001 to 999.

- The hyphen (-) is a character used to separate the group of the first 10 digits from the last 3 digits.

Thus, the significance of the first two digits in the TIN structure is to represent the segment number of the TIN.

What is the significance of the first two digits in the TIN structure? (Image from the Internet)

What are regulations on the classification of structure of TIN in Vietnam?

According to Clause 3, Article 5 of Circular 105/2020/TT-BTC, the structure of the TIN is prescribed as follows:

- The 10-digit TIN is used for businesses, cooperatives, organizations with legal person status or organizations without a legal person that directly incur tax obligations; representatives of households, business households, and other individuals (hereinafter referred to as independent units).

- The 13-digit TIN and the hyphen (-) used to separate the first 10 digits and the last 3 digits are used for dependent units and other entities.

- Taxpayers that are economic organizations, other organizations as stipulated in points a, b, c, d, n Clause 2 Article 4 of Circular 105/2020/TT-BTC, possessing either legal person status or not but directly incurring tax obligations and bearing responsibility for all tax obligations before the law, are assigned a 10-digit TIN;

Dependent units established under the legal provisions of the aforementioned taxpayers that incur tax obligations and directly declare, pay taxes are assigned a 13-digit TIN.

- Foreign contractors and subcontractors according to point đ Clause 2 Article 4 of Circular 105/2020/TT-BTC registering to pay contractor tax directly with the tax authorities are assigned a 10-digit TIN for each contract.

In the case of foreign contractors forming a consortium with Vietnamese economic organizations to conduct business in Vietnam based on a bidding contract, and the parties to the consortium establishing a Joint Operating Body to handle accounting, hold a bank account, and be responsible for issuing invoices;

Or if the Vietnamese economic organization within the consortium is responsible for common accounting and profit sharing among consortium members, they are assigned a 10-digit TIN to declare and pay tax for the contract.

If foreign contractors, subcontractors have an office in Vietnam and have been declared and had contractor tax withheld by the Vietnamese side, the foreign contractors, subcontractors are assigned a 10-digit TIN to declare other tax obligations (except for contractor tax) in Vietnam and provide the TIN to the Vietnamese side.

- Foreign suppliers according to point e Clause 2 Article 4 of Circular 105/2020/TT-BTC without a TIN in Vietnam, when directly registering with tax authorities are assigned a 10-digit TIN.

Foreign suppliers use the assigned TIN to directly declare, pay tax or provide the TIN to organizations, individuals in Vietnam authorized by the foreign supplier or provide to commercial banks, intermediary payment service providers to perform tax withholding, payment, and declaration into the Statement of Tax Withholding for foreign suppliers in Vietnam.

- Organizations, individuals withholding and paying on behalf as stated in point g Clause 2 Article 4 of Circular 105/2020/TT-BTC are assigned a 10-digit TIN (hereafter referred to as a proxy TIN) to declare, pay tax on behalf of foreign contractors, subcontractors, foreign suppliers, organizations, and individuals with contracts or business cooperation documents.

Foreign contractors, subcontractors as specified in point đ Clause 2 Article 4 of Circular 105/2020/TT-BTC declared, paid on behalf of contractor tax by the Vietnamese side are assigned a 13-digit TIN according to the proxy TIN of the Vietnamese side to confirm completion of contractor tax obligations in Vietnam.

When a taxpayer changes taxpayer registration information, suspends, resumes operations, or deactivates the TIN and restores the TIN following taxpayer TIN regulations, the proxy TIN is updated correspondingly by the tax authorities according to the taxpayer's information and TIN status.

Taxpayers are not required to submit documents as per the regulations in Chapter 2 Circular 105/2020/TT-BTC regarding the proxy TIN.

- Operators, joint operating companies, joint venture enterprises, and organizations assigned by the Government of Vietnam to receive the oil and gas royalties of Vietnam from overlapping oil and gas fields as per point h Clause 2 Article 4 of Circular 105/2020/TT-BTC are issued a 10-digit TIN per oil and gas contract, agreement, or equivalent document.

Contractors, investors participating in oil and gas contracts are issued a 13-digit TIN according to the 10-digit TIN of each oil and gas contract to fulfill tax obligations for the oil and gas contract (including corporate income tax on income from transferring interests in oil and gas contracts).

The parent company - Vietnam National Oil and Gas Group, representing the host country, receiving shared profits from oil and gas contracts is assigned a 13-digit TIN according to the 10-digit TIN of each oil and gas contract to declare and pay taxes on shared profits per oil and gas contract.

- Taxpayers being households, business households, individual businesses, and other individuals as stated in points i, k, l, n Clause 2 Article 4 of Circular 105/2020/TT-BTC are assigned a 10-digit TIN to the representative of the household, business representative, individual and assigned a 13-digit TIN for the business locations of business households and individual businesses.

- Organizations, individuals under point m Clause 2 Article 4 of Circular 105/2020/TT-BTC having one or more authorized collection contracts with a tax authority are assigned one proxy TIN to remit collected funds from taxpayers into the state budget.

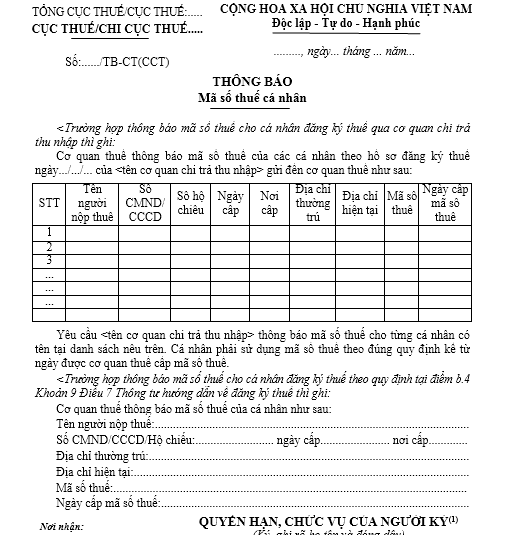

What is the latest personal TIN notification form in Vietnam for 2024?

The personal TIN notification is executed according to Form No. 14-MST issued with Circular 105/2020/TT-BTC.

Download The latest Personal TIN Notification Form 2024.