What is the non-agricultural land use tax declaration form - Form 02/TK-SDDPNN applicable to organizations in Vietnam?

What is the non-agricultural land use tax declaration form - Form 02/TK-SDDPNN applicable to organizations in Vietnam?

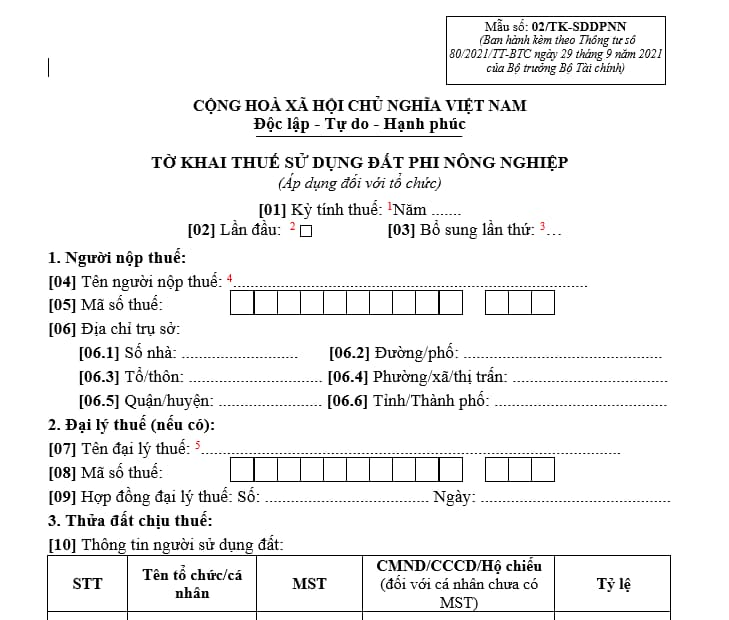

The non-agricultural land use tax declaration form - Form 02/TK-SDDPNN applicable to organizations in Vietnam is prescribed in Appendix 2 attached to Circular 80/2021/TT-BTC as follows:

Download the non-agricultural land use tax declaration - Form 02/TK-SDDPNN (applicable for organizations): Here

What is the non-agricultural land use tax declaration form - Form 02/TK-SDDPNN applicable to organizations in Vietnam? (Image from the Internet)

What are the regulations on declaring non-agricultural land use tax in Vietnam?

According to Article 8 of the Law on Non-Agricultural Land Use Tax 2010 on registration, declaration, calculation and payment of non-agricultural land use tax:

- Taxpayers shall register, declare, calculate and pay tax under the law on tax administration.

- Taxpayers shall register, declare, calculate and pay tax at tax offices of rural districts, urban districts, towns or provincial cities in which they have land use rights.

Taxpayers in deep-lying or remote areas difficult to access may register, declare, calculate and pay tax at commune-level People’s Committees. Tax offices shall create conditions for taxpayers to fulfill their obligations.

- When a taxpayer has the right to use many residential land plots, the taxable area is the total area of taxable residential-land plots within a province or centrally run city. Tax registration, declaration, calculation and payment are specified as follows:

+ Taxpayers shall register, declare, calculate and pay tax at tax offices of rural districts, urban districts, towns or provincial cities in which they have land use rights;

+ Taxpayers may choose the residential land quota applicable in a rural district, urban district, town or provincial city in which they have land use rights. A taxpayer who has one or more than one residential land plot in excess of the set quota may choose one place in which he/she has a residential land plot in excess of the set quota for determining the land plots’ area in excess of the set quota .

The applicable taxable price is the land price applied in each rural district, urban district, town or provincial city in which the land plot exists.

Taxpayers shall make general declarations according to a set form for determining the total area of residential land plots for which they have use rights and the paid tax amount, and send them to the tax office of the locality they have chosen for determining the residential land quota in order to pay the difference between the tax amount payable under Law on Non-Agricultural Land Use Tax 2010 and the paid tax amount.

What are the applicable non-agricultural land use tax rates for 2024 in Vietnam?

According to Article 7 of the Law on Non-Agricultural Land Use Tax 2010 on non-agricultural land use tax rates:

- Tax rates for residential land, including land used for commercial purposes, to be applied according to the Partially Progressive Tariff are specified as follows:

|

Tax grade |

Taxable land area (m2) |

Tax rate (%) |

|

1 |

Area within the set quota |

0.03 |

|

2 |

Area in excess of up to 3 times the set quota |

0.07 |

|

3 |

Area in excess of over 3 times the set quota |

0.15 |

- The residential land quota used as a basis for tax calculation is the new quota of residential land allocation set by provincial-level People’s Committees from the effective date of this Law.

When residential land quotas have been set before January 1, 2012, the following provisions shall be applied:

+ When the residential land quota set before January 1, 2012 is lower than the new quota of residential land allocation, the new quota will be used as a basis for tax calculation;

+ When the residential land quota set before the effective date of this Law is higher than the new quota of residential land allocation, the old quota will be used as a basis for tax calculation.

- Residential land of multi-story buildings with many households, condominiums or underground construction works is subject to the tax rate of 0.03%.

- Non-agricultural production and business land is subject to the tax rate of 0.03%.

- Non-agricultural land specified in Article 3 of Law on Non-Agricultural Land Use Tax 2010 which is used for commercial purposes is subject to the tax rate of 0.03%.

- Land used for improper purposes or land not yet used under regulations is subject to the tax rate of 0.15%. Land of a phased investment project as registered by the investor and approved by a competent state agency will not be regarded as unused land and is subject to the tax rate of 0.03%.

- Encroached or appropriated land is subject to the tax rate of 0.2% and has no applicable quota. Tax payment does not serve as a basis for recognizing taxpayers’ lawful land use rights for the encroached or appropriated land area.