What is the low-value import-export goods declaration form upon customs clearance in Vietnam?

What is the low-value import-export goods declaration form upon customs clearance in Vietnam?

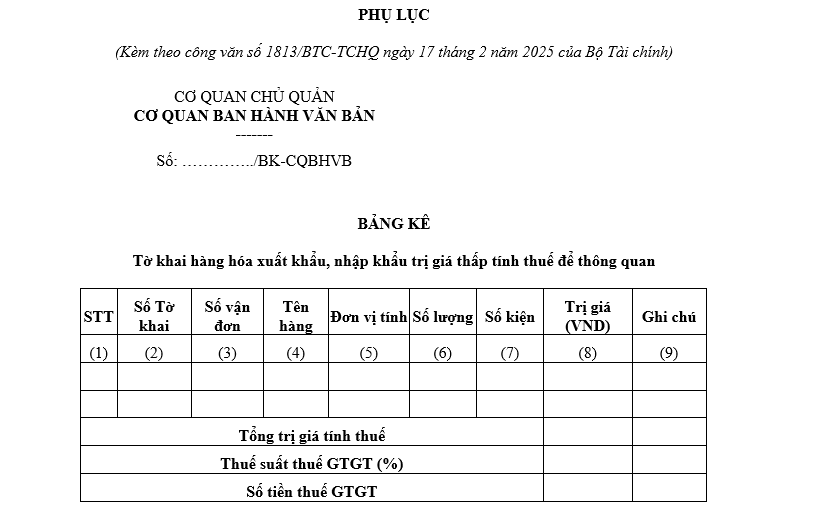

The low-value import-export goods declaration form for tax purposes upon customs clearance is a template guided by the Ministry of Finance as per the appendix issued with Official Dispatch 1813/BTC-TCHQ of 2025.

The low-value import-export goods declaration form for tax purposes upon customs clearance is as follows:

Download the low-value import-export goods declaration form for tax purposes upon customs clearance here

What is the low-value import-export goods declaration form upon customs clearance in Vietnam? (Image from the Internet)

When shall import-export goods be cleared in Vietnam?

Based on Clause 1, Article 37 of the Customs Law 2014, the regulations for customs clearance are as follows:

(1) Goods are cleared after customs procedures are completed.

(2) In cases where the customs declarant has completed the customs procedures but has not paid, or not paid in full, the taxes due within the stipulated period, the goods are cleared when a credit institution provides a guarantee for the tax amount due or when tax deferment according to the tax law is applied.

(3) In cases where the goods owner is subject to a customs administrative penalty in the form of a fine and the goods are permitted for export or import, the goods may be cleared if the fine has been paid or if a credit institution guarantees the payable amount to enforce the penalty decision by the customs authority or competent state agency.

(4) For goods requiring inspection, analysis, or assessment to determine compliance with export or import conditions, customs clearance is only executed after determining goods compliance based on inspection, analysis, or assessment conclusions, or a notice of inspection exemption by a specialized inspection agency as per legal regulations.

(5) Goods serving urgent needs; goods specifically used for security or national defense; diplomatic bags, consular bags, or luggage of agencies, organizations, or individuals entitled to privileges and immunities are cleared according to the provisions in Articles 50 and 57 of the Customs Law 2014.

Therefore, import-export goods are cleared after completing customs procedures.

When shall import-export duties be paid, before or after customs clearance in Vietnam?

According to Clause 1, Article 9 of the Law on Import and Export Duties 2016, it is regulated as follows:

Tax Payment Deadline

1. Exported and imported goods subject to tax obligations must pay taxes before customs clearance or goods release according to the Customs Law, except for cases stipulated in Clause 2 of this Article.

If a credit institution guarantees the taxes due, goods may be cleared or released, but the payer must pay late payment interest according to the Tax Administration Law from the date of clearance or goods release until the tax payment date. The maximum guarantee period is 30 days from the registration of the customs declaration.

If a credit institution has provided a guarantee but the guarantee period expires and the taxpayer has not paid taxes and late payment interest, the guarantor is responsible for paying the full amount of taxes and late payment interest on behalf of the taxpayer.

- Taxpayers granted priority policies under the Customs Law may pay taxes for customs declarations that have been cleared or goods released within the respective month, no later than the tenth day of the following month. If the taxpayer fails to pay taxes past this deadline, they must pay the full tax debt and late payment interest according to the Tax Administration Law.

Hence, according to the above regulation, import-export goods subject to import-export taxes must pay taxes before customs clearance.

Note: Taxpayers entitled to priority policies under the Customs Law can pay taxes for customs declarations that have been cleared or goods released within the month, no later than the tenth day of the following month. Missing this deadline requires the payer to settle any tax debt and late payment interest as stipulated by the Tax Administration Law.

What goods and services are subject to import-export duties in Vietnam?

Based on Article 2 of the Law on Import and Export Duties 2016, the subjects of import-export duties are defined as follows:

- Goods exported and imported through Vietnamese borders and checkpoints.

- Goods exported from the domestic market into non-tariff zones, and goods imported from non-tariff zones into the domestic market.

- Goods exported, imported on site, and goods exported, imported by enterprises with export, import, and distribution rights.

- Import-export tax does not apply to the following cases:

+ Goods in transit, transshipment;

+ Humanitarian aid, goods provided as non-refundable aid;

+ Goods exported from non-tariff zones to a foreign country; goods imported from a foreign country into a non-tariff zone and used only within the non-tariff zone; goods transferred between non-tariff zones;

+ Crude oil used to pay resource tax to the State when exported.