What is the latest application form for amendments to tax registration in Vietnam in 2025?

What is the latest application form for amendments to tax registration in Vietnam in 2025?

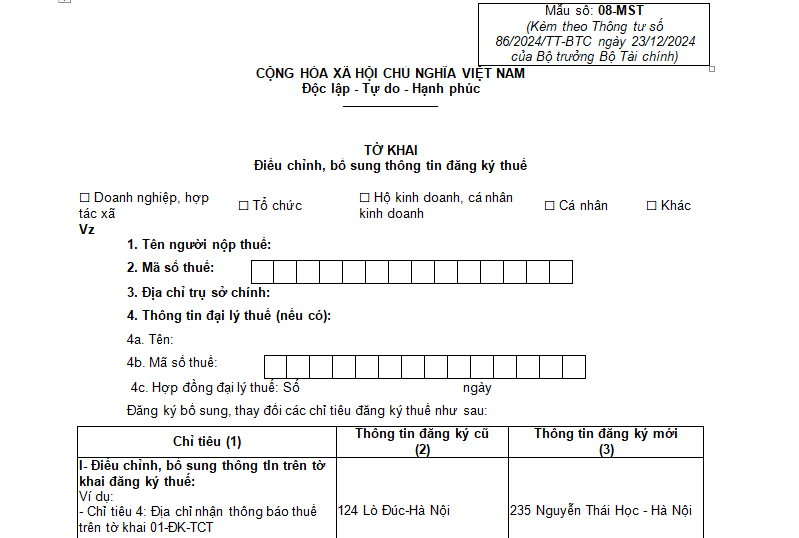

The latest application form for amendments to tax registration in 2025 is Form 08-MST as stipulated in Appendix II issued together with Circular 86/2024/TT-BTC (effective from February 6, 2025).

Download Form 08-MST Declaration for amendments to tax registration

Form 08-MST for amendments to tax registration is applied in cases of changes in tax registration for taxpayers who are organizations as stipulated in Article 10 Circular 86/2024/TT-BTC and taxpayers who are household businesses, families, or individuals as stipulated in Article 25 Circular 86/2024/TT-BTC.

What is the latest application form for amendments to tax registration in Vietnam in 2025? (Image from the Internet)

What does the application for amendments to tax registration include for household businesses in Vietnam from February 6, 2025?

Based on Article 25 Circular 86/2024/TT-BTC (effective from February 6, 2025), the application for amendments to tax registration for household businesses is stipulated as follows:

(1) household businesses, families, or individuals changing tax registration without altering the direct tax authority

- household business taxpayer registration under the one-stop shop mechanism, when there is a change in tax registration, shall change the tax registration concurrently with changing the business registration content with the business registration authority.

- Families or individuals engaged in production or business activities not required to register as household businesses through the business registration authority under the Government of Vietnam’s regulations on household businesses; individual businesses from bordering countries conducting the purchase, sale, or exchange of goods at border markets, border-gate markets, or border-gate economic zones must submit a dossier to change information to the direct tax authority, which includes:

+ Declaration for amendments to tax registration Form 08-MST issued together with Circular 86/2024/TT-BTC.

+ A photocopy of the valid passport of the individual if the information on this document has changed concerning individuals where the tax authority issues a tax code as per point a, clause 4, Article 5 Circular 86/2024/TT-BTC.

(2) household businesses registering taxpayer information under the one-stop shop mechanism when changing address to another province or city directly under the Central Government or changing address to a different district but within the same province or city directly under the Central Government thereby changing the direct tax authority must proceed as follows:

- At the place of departure:

+ Declaration for amendments to tax registration Form 08-MST issued together with Circular 86/2024/TT-BTC.

+ Upon receipt of the Notice of relocation, Form 09-MST issued together with Circular 86/2024/TT-BTC from the tax authority at the place of departure, household businesses must register to change the head office address at the business registration authority as per the law on business registration.

(3) Families, individuals engaged in production or business activities not required to register household businesses according to the Government of Vietnam’s regulations on household businesses; individuals from bordering countries conducting trade activities at border markets or economic zones change address to another province or city or to a different district but within the same province or city changing the direct tax authority must:

- At the place of departure:

+ Declaration for amendments to tax registration Form 08-MST issued together with Circular 86/2024/TT-BTC.

- At the place of arrival:

+ Registration document for change of location at the tax authority to which the taxpayer is relocating, Form 30/ĐK-TCT issued together with Circular 86/2024/TT-BTC.

(4) For individuals stipulated at points k, l, n clause 2 Article 4 Circular 86/2024/TT-BTC, when changing tax registration of themselves and dependents (including cases of changing the direct tax authority), shall submit the dossier to the income-paying organization or the Tax Department, Regional Tax Department where the individual is registered for permanent or temporary residence (if the individual does not work at the income paying organization or does not authorize the income-paying organization) as follows:

- application for amendments to tax registration submitted through the income-paying organization includes:

+ The authorization document Form 41/UQ-ĐKT issued together with Circular 86/2024/TT-BTC (for cases where the authorization document to the income-paying organization has not been previously issued).

In cases where the individual or dependents fall under the tax code issuance by the tax authority under point a clause 4 Article 5 Circular 86/2024/TT-BTC, they must also submit a photocopy of the passport which records the change in tax registration for the individual or dependents.

The income-paying organization is responsible for consolidating the individual's amended information into the Taxpayer Registration Declaration Form 05-ĐK-TH-TCT and the changed information of dependents into the Taxpayer Registration Declaration Form 20-ĐK-TH-TCT issued together with Circular 86/2024/TT-BTC submitted to the direct tax authority of the income-paying organization.

- application for amendments to tax registration directly submitted to the tax authority includes:

+ Declaration for amendments to tax registration Form 08-MST or Form 20-ĐK-TCT issued together with Circular 86/2024/TT-BTC.

In cases where the individual or dependents fall under the tax code issuance by the tax authority according to point a clause 4 Article 5 Circular 86/2024/TT-BTC, they must also submit a copy of the valid passport of the individual or dependents if there is a change in tax registration on this document.

(5) For non-resident foreign individuals in Vietnam as stipulated in point e clause 2 Article 4 [Circular 86/2024/TT-BTC](https://lawnet.vn/vb/Thong-tu-86-2024-TT-BTC-dang-ky-thue-8A03