What is the Land price list for District 1, Ho Chi Minh City 2025? Which entities are land use tax payers in Vietnam in 2025?

What is the Land price list for District 1, Ho Chi Minh City 2025?

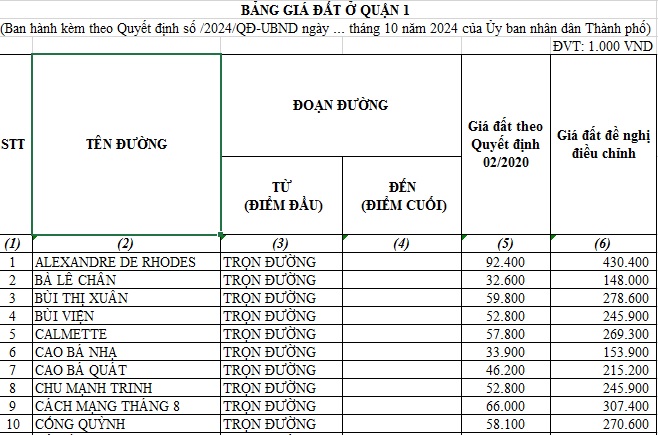

On October 21, 2024, the People's Committee of Ho Chi Minh City issued Decision 79/2024/QD-UBND, amending and supplementing Decision 02/2020/QD-UBND regarding the Land price list of Ho Chi Minh City. Decision 79/2024/QD-UBND stipulates the Land price list of Ho Chi Minh City to be applied until December 31, 2025.

The latest Land price list for District 1, Ho Chi Minh City, has been adjusted according to Decision 79/2024/QD-UBND as follows:

See detailed Land price list for District 1, Ho Chi Minh City 2025 here...Download

See more:

>>> Land price list on Cách Mạng Tháng 8, District 1, Ho Chi Minh City

What is the Land price list for District 1, Ho Chi Minh City 2025? (Image from the Internet)

Which entities are land use tax payers in Vietnam in 2025?

Land use tax includes: Agricultural land use tax and non-agricultural land use tax.

(1) Entities subject to agricultural land use tax

Pursuant to Article 1 of Decree 74-CP and Article 1 of the 1993 Agricultural Land Use Tax Law, individuals and organizations using agricultural production land are required to pay agricultural land use tax, including:

- Individuals, households, private entities.

- Individuals, organizations using agricultural land in areas dedicated to the societal utilities of communes.

- Enterprises operating in agriculture, forestry, fisheries, including forestry farms, state farms, stations, enterprises, and other businesses, public service providers, state agencies, social organizations, armed forces units, and other units using land for aquaculture, agricultural-forestry production.

(2) Entities subject to non-agricultural land use tax

According to Article 4 of the 2010 Law on Non-agricultural Land Use Tax, entities subject to non-agricultural land use tax are as follows:

- Taxpayers are organizations, households, individuals with land use rights subject to the non-agricultural land use tax as stated.

- In cases where organizations, households, individuals have not been granted a Certificate of Land Use Rights, Ownership of Houses, and Other Assets attached to the land (hereinafter referred to as the Certificate), the person currently using the land is the taxpayer.

- Taxpayers in specific cases are determined as follows:

- If the State leases land for investment projects, the land lessee is the taxpayer;

- If the person with land use rights leases the land under a contract, the taxpayer is determined by the agreement within the contract. If the contract does not specify the taxpayer, then the person with land use rights is the taxpayer;

- If the land has been certified but is under dispute, before the dispute is resolved, the person using the land is the taxpayer. Tax payment is not a basis for resolving land use right disputes;

- If multiple individuals share a land parcel, the taxpayer is the legal representative of those sharing the parcel;

- If land use rights are contributed as capital forming a new legal entity with land use rights subject to the aforementioned tax, the new legal entity is the taxpayer.

How is the tax price for non-agricultural land use calculated in Vietnam?

Pursuant to Article 6 of the 2010 Law on Non-agricultural Land Use Tax, the tax price for non-agricultural land use is prescribed as follows:

(1) The tax price for land is determined by multiplying the taxable land area by the price per square meter of land.

(2) The taxable land area is determined as follows:

- The taxable land area is the actual land area used.

In cases of multiple residential parcels, the taxable land area is the sum of the taxable areas of the parcels.

For lands assigned or leased by the State for industrial park construction, the taxable land area does not include the area used for shared infrastructure construction;

- For multi-level residential buildings, condominiums, including those used both for living and business, the taxable land area is determined by the allocation ratio multiplied by the floor area used by each organization, household, individual.

The allocation ratio is determined by dividing the land area for constructing multi-level residential buildings, condominiums by the total floor area used by organizations, households, individuals.

In cases where multi-level residential buildings, condominiums have basement levels, 50% of the basement area used by organizations, households, individuals is added to the floor area for calculating the allocation ratio;

- For underground constructions, the allocation ratio is 0.5 times the construction land area divided by the total construction area used by organizations, households, individuals.

(3) The price per square meter of land is based on the Land price list corresponding to the intended use and is stabilized on a five-year cycle.