What is the Gregorian date for the 1st day of the 12th lunar month? Is the deadline for the first information disclosure for fixed tax payers of 2024 the 1st day of the 12th lunar month?

What is the Gregorian date for the 1st day of the 12th lunar month?

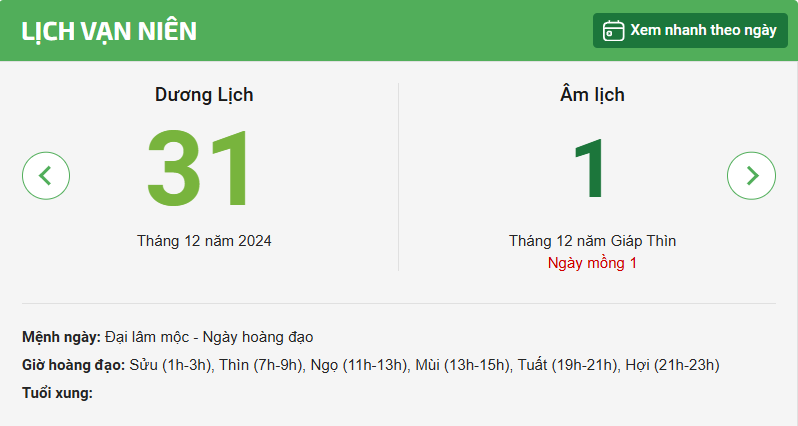

Based on the lunar calendar of 2024 and the Gregorian calendar of 2025, the 1st day of the 12th lunar month falls on Tuesday, January 31, 2025.

Note: Information about the Gregorian date for the 1st day of the 12th lunar month, 2025, is for reference only.

What is the Gregorian date for the 1st day of the 12th lunar month? Is the deadline for the first information disclosure for fixed tax payers of 2024 the 1st day of the 12th lunar month? (Image from the Internet)

What is the deadline for the first information disclosure for fixed tax payers in Vietnam in 2024?

According to Clause 5, Article 13 of Circular 40/2021/TT-BTC, the information disclosure of households required to pay tax in the first installment is stipulated as follows:

Tax management for fixed tax payers

...

- First information disclosure

The tax authority conducts the first information disclosure for reference, gathering opinions on estimated revenue, and estimated tax amount. The first information disclosure documents include: List of fixed tax payers not subject to VAT, not subject to personal income tax; List of fixed tax payers subject to tax. The first information disclosure is conducted as follows:

a) The Tax Sub-department publicly lists the first installment at the one-stop-shop department of the Tax Sub-department, the District People's Committee; at doors, gates, or convenient information access locations, appropriate locations of commune-level town, the head office of the commune, ward People's Committee; head office of the Tax Team; market management board for public supervision. The information disclosure period for the first installment is from December 20 to December 31 each year.

b) The Tax Sub-department sends the first information disclosure documents to the People's Council and the Vietnamese Fatherland Front at the district, commune, ward, commune-level town level, no later than December 20 each year, clearly stating the address, and time for receiving feedback (if any) from the People's Council and the Vietnamese Fatherland Front at district, commune, ward, commune-level town level. The feedback reception period at the Tax Sub-department (if any) is no later than December 31.

c) No later than December 20 each year, the Tax Sub-department sends to each fixed tax payer a Notice regarding the estimated revenue, tax amount according to form No. 01/TBTDK-CNKD attached with the public information form No. 01/CKTT-CNKD issued with this Circular, clearly stating the address, time for receiving feedback (if any) from fixed tax payers no later than December 31. Notices are sent directly to fixed tax payers (with taxpayer's signed acknowledgment of receipt) or sent via post using guaranteed delivery. The planned public information sent to fixed tax payers is compiled based on the locality, including individuals subject to tax and individuals not subject to tax. For markets, streets, neighborhoods with 200 or fewer fixed tax payers, the Tax Sub-department prints and distributes to each household the public table of fixed tax payers in the area. If markets, streets, neighborhoods have more than 200 fixed tax payers, the Tax Sub-department prints and distributes to each household not more than the public table of 200 fixed tax payers in the area. Specifically for markets with more than 200 fixed tax payers, the Tax Sub-department prints and distributes to each household the public table according to business sectors. If the tax authority has managed to publicly post the public table on the electronic information portal of the tax authority, it is not mandatory to send the public table according to form No. 01/CKTT-CNKD attached with the Notice of estimated revenue, tax amount form No. 01/TBTDK-CNKD issued with this Circular.

d) The Tax Sub-department is responsible for publicly announcing the listing location, address for receiving feedback (phone number, fax number, address at the one-stop-shop department, email address) regarding the information disclosure content for fixed tax payers to know.

đ) The Tax Sub-department is responsible for summarizing feedback on the first information disclosure content from the public, taxpayers, the People's Council, and the Vietnamese Fatherland Front at district, commune, ward, commune-level town level to consider adjusting, supplementing managed subjects, estimated revenue, and estimated tax before consulting the Tax Advisory Council.

Therefore, the period during which the Tax Sub-department conducts the listing of the first fixed tax payers for 2024 is from December 20, 2024, to January 31, 2025. Hence, it can be determined that the deadline for the first information disclosure for fixed tax payers for 2024 is January 31, 2025, which coincides with the 1st day of the 12th lunar month.

When is the deadline for submitting tax declaration dossiers for fixed tax payers in Vietnam?

According to Clause 3, Article 13 of Circular 40/2021/TT-BTC, the deadline for submitting tax declaration dossiers for fixed tax payers is stipulated as follows:

- The deadline for submitting tax declaration dossiers for fixed tax payers is no later than December 15 of the year preceding the taxable year.

- In the case of newly entering business fixed tax payers (including those switching to the estimated method), or fixed tax payers switching to the declaration method, or changing business lines, or changing business scale during the year, the deadline for submitting tax declaration dossiers is no later than 10 days from the start of business, or switch of tax calculation method, or change of business lines, or change of business scale.

- The deadline for submitting tax declaration dossiers for fixed tax payers using invoices issued by the tax authority for retail with single-issue occurrences is no later than 10 days from the day the revenue requiring invoices arises.