What is the form of e-invoice for sale of public property in Vietnam in 2025? Is it mandatory to use e-invoices for the sale of public property in Vietnam?

What is the form of e-invoice for sale of public property in Vietnam in 2025?

Based on Clause 2, Article 95 of Decree 151/2017/ND-CP amended by Clause 60, Article 1 Decree 114/2024/ND-CP which regulates the model of invoices for the sale of public property as follows:

Invoice for Sale of public property

...

- e-invoice for the sale of public property:

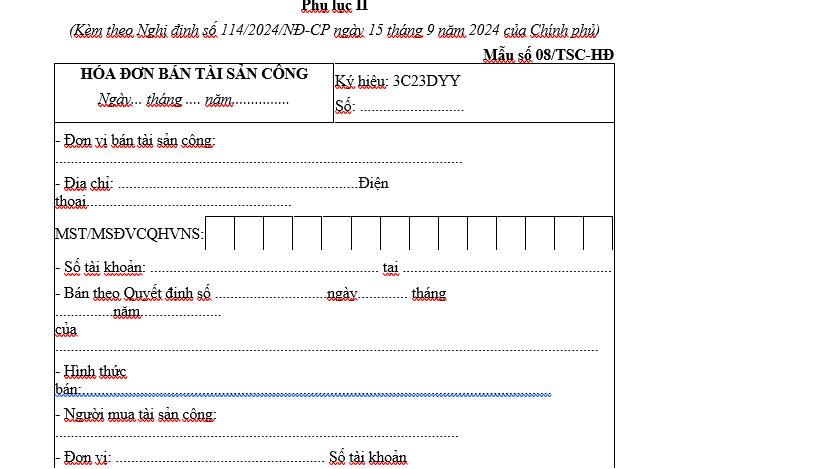

a) The e-invoice model for the sale of public property is implemented according to Model number 08/TSC-HĐ issued with this Decree.

...

Thus, the e-invoice model for the sale of public property is Model number 08/TSC-HĐ issued with Decree 114/2024/ND-CP.

Model number 08/TSC-HĐ is as follows:

Download Model 08/TSC-HĐ: e-invoice for the sale of public property

What is the form of e-invoice for sale of public property in Vietnam in 2025? Is it mandatory to use e-invoices for the sale of public property in Vietnam? (Image from the Internet)

Is it mandatory to use e-invoices for the sale of public property in Vietnam?

Based on Article 95 of Decree 151/2017/ND-CP amended by Clause 60, Article 1 of Decree 114/2024/ND-CP which regulates invoices for the sale of public property as follows:

Invoice for Sale of public property

...

- e-invoice for the sale of public property:

a) The e-invoice model for the sale of public property is implemented according to Model number 08/TSC-HĐ issued with this Decree.

b) The agency assigned to handle public property issues e-invoices through an e-invoice service provider (for agencies that are VAT taxpayers with a tax code) or through the General Department of Taxation's e-portal (for agencies not required to pay VAT with a tax code) per government regulations on invoices and documents for buyers when selling, transferring types of public property stipulated in Clause 1 of this Article. The agency tasked with managing public property makes sales invoices with a tax authority code as regulated for non-business organizations that have sales or service transactions; and is not required to pay for the use of e-invoices.

c) The tax authority provides electronically coded invoices for selling or transferring public property per occurrence to the agency designated to manage public property.

d) The preparation, adjustment, cancellation, and reporting on the management and use of e-invoices for selling public property are executed per government regulations on invoices and documents.

dd) The mandatory date to switch to using e-invoices for the sale of public property is January 1, 2025.

- The money recorded on the invoice for the sale of public property does not include VAT.

Therefore, based on the above regulation, starting January 1, 2025, individuals and organizations are required to switch to using e-invoices for the sale of public property.

What are regulations on the destruction of physical invoices for the sale of public property in Vietnam?

Based on Section 4 Official Dispatch 14590/BTC-QLCS in 2024 of the Ministry of Finance on the application for using e-invoices for the sale of public property and the destruction of unused paper invoices for the sale of public property as follows:

4. Provincial/City People's Committees direct the Departments of Finance:

a) Destroy unused physical invoices for the sale of public property remaining as of December 31, 2024; deadline for execution: before January 31, 2025.

b) The destruction of unused physical invoices for the sale of public property is performed according to the procedures set out in Article 27 of Decree No. 123/2020/ND-CP dated October 19, 2020, by the Government of Vietnam on invoices and documents.

c) Report the destruction results of invoices to the Ministry of Finance (Department of Public Asset Management) within 5 working days from the execution date of invoice destruction.

d) Report on the management and use of invoices for the sale of public property up to December 31, 2024, to the Ministry of Finance (Department of Public Asset Management) before January 31, 2025.

Additionally, as referenced in Article 27 of Decree 123/2020/ND-CP, the destruction of physical invoices for the sale of public property is conducted as follows:

(1) Enterprises, economic organizations, households, and individuals with invoices not in use must destroy the invoices. The deadline for invoice destruction is no later than 30 days from the date of notification to the tax authority. In cases where the tax authority has announced the invalidation of invoices (except for announcements due to tax debt enforcement measures), such entities are required to destroy invoices within 10 days from the date the tax authority announces or from the date the lost invoice is recovered.

- Invoices that have been issued by accounting units are to be destroyed according to accounting law.

- Invoices not issued but are evidence in legal cases are not destroyed but handled under the law.

(2) The destruction of invoices by enterprises, economic organizations, households, and business individuals is conducted as follows:

- Enterprises, economic organizations, households, and business individuals must prepare an inventory list of invoices to be destroyed.

- Enterprises, economic organizations must establish an Invoice Destruction Council. The Council must include a representative of the leadership and the accounting department of the organization. Households and individuals are not required to establish a Council when destroying invoices.

- All members of the Invoice Destruction Council must sign the invoice destruction minutes and are legally responsible in the event of any errors.

- The invoice destruction dossier includes:

+ The decision to establish the Invoice Destruction Council, except for households, business individuals;

+ Inventory list of invoices to be destroyed detailing: Name of the invoice, invoice form code, invoice symbol, the quantity of invoices from number... to number... or detailing each invoice number if the invoices for destruction are not continuous;

+ Invoice destruction minutes;

+ Notification of invoice destruction results must include: type, symbol, quantity of invoices destroyed from number to number, reason for destruction, date and time of destruction, method of destruction per Model number 02/HUY-HDG Appendix IA issued with Decree 123/2020/ND-CP.

The invoice destruction dossier is retained at the enterprise, economic organization, household, business individuals using the invoice. Particularly, the Notification of invoice destruction results is made in two copies, one for records, one submitted to the directly managed tax office no later than 5 days from the date of invoice destruction.

(3) Invoice destruction by tax authorities

- Tax authorities perform the destruction of invoices printed by the Tax Department that have been announced but not sold or not issued but won't be used.

- The General Department of Taxation is responsible for stipulating procedures for the destruction of invoices printed by the Tax Department.