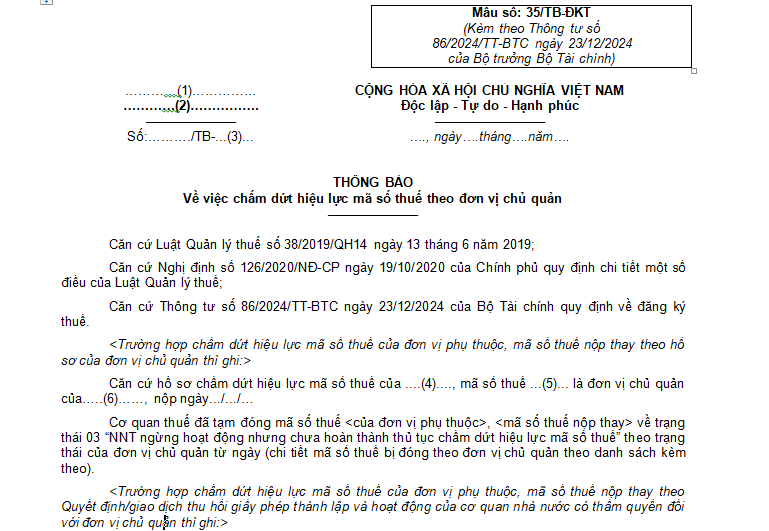

What is the Form No. 35/TB-DKT - Notice of TIN deactivation by the managing unit in Vietnam as per Circular 86?

What is the Form No. 35/TB-DKT - Notice of TIN deactivation by the managing unit in Vietnam as per Circular 86?

Form No. 35/TB-DKT is a notification form regarding the TIN deactivation by the managing unit stipulated in Appendix II issued along with Circular 86/2024/TT-BTC (effective from February 6, 2025).

Form No. 35/TB-DKT is presented as follows:

Download Form 35/TB-DKT: notification form regarding the TIN deactivation by the managing unit.

What is the Form No. 35/TB-DKT - Notice of TIN deactivation by the managing unit in Vietnam as per Circular 86? (Image from the Internet)

What are cases of TIN deactivation in Vietnam?

Based on Clauses 1 and 2 of Article 39 Law on Tax Administration 2019, the cases for TIN deactivation are specified as follows:

(1) Taxpayers with taxpayer registration along with business registration, cooperative registration, or business registration, will deactivate TIN validity under the following circumstances:

- Cessation of business activities or dissolution, bankruptcy;

- Revocation of business registration certificate, cooperative registration certificate, or business registration certificate;

- Division, merger, or consolidation.

(2) Taxpayers with direct taxpayer registration with the tax authority shall deactivate TIN validity under the following circumstances:

- Cessation of business activities, no longer incurring tax obligations for non-business organizations;

- Revocation of business registration certificate or equivalent license;

- Division, merger, or consolidation;

- Notification by the tax authority that the taxpayer is not operating at the registered address;

- Individuals deceased, missing, or incapacitated as per legal regulations;

- Foreign contractors upon the conclusion of a contract;

- Contractors, investors participating in petroleum contracts upon contract conclusion or assignment of all contractual interests.

What is the application for TIN deactivation for organizations with direct taxpayer registration with the tax authority from February 6, 2025?

Based on Clause 1 of Article 14 Circular 86/2024/TT-BTC (effective from February 6, 2025), the dossier for TIN deactivation for organizations with direct taxpayer registration with the tax authority is as follows:

The dossier for TIN deactivation for organizations with direct taxpayer registration with the tax authority is a written request to deactivate TIN validity Form No. 24/ĐK-TCT issued along with Circular 86/2024/TT-BTC in accordance with Articles 38, 39 Law on Tax Administration 2019 and other documents as follows:

- For economic organizations, other organizations as stipulated at Points a, b, c, d, n Clause 2 Article 4 Circular 86/2024/TT-BTC:

+ For the managing unit, the dossier includes one of the following documents: A copy of the dissolution decision, a copy of the division decision, a copy of the merger contract, a copy of the consolidation contract, a copy of the decision to revoke the operation registration certificate by a competent authority, a copy of the deactivation of operation notification, or a copy of the conversion decision.

(i) In cases where the managing unit has subsidiaries already assigned a 13-digit TIN, the managing unit must issue a written notification of operation deactivation to subsidiaries to require the subsidiaries to perform procedures to deactivate their TIN validity with the tax authority managing the subsidiary before deactivating the managing unit's TIN validity.

(ii) In cases where subsidiaries deactivate TIN validity but are unable to fulfill tax obligations to the state budget according to the Law on Tax Administration and guiding documents, the managing unit must submit a declaration of commitment taking responsibility for assuming all subsidiary tax obligations to the tax authority managing the subsidiary, and continue to fulfill the subsidiary's tax obligations with the tax authority responsible for managing the subsidiary's tax obligations after the subsidiary's TIN validity has been deactivated.

+ For subsidiaries, the dossier includes one of the following documents: A copy of the decision or notification of subsidiary operation deactivation, a copy of the decision to revoke the operation registration certificate of a competent authority for the subsidiary.

- For contractors, investors participating in petroleum contracts, or the parent company - Vietnam National Oil and Gas Group representing the host country receiving a share of profits from petroleum contracts; foreign contractors, foreign subcontractors as stipulated at Points đ, h Clause 2 Article 4 Circular 86/2024/TT-BTC (excluding foreign contractors, foreign subcontractors issued a TIN under the provisions of Point e Clause 4 Article 5 Circular 86/2024/TT-BTC), the dossier includes: A copy of the contract liquidation document, or a copy of the document on transferring all capital contributions participating in the petroleum contract for investors participating in the petroleum contract.