What is the Form for the tax registration application for sole proprietorships operating in specialized fields in Vietnam for 2025 (Form 01-DK-TCT)?

What is the Form for the tax registration application for sole proprietorships operating in specialized fields in Vietnam for 2025 (Form 01-DK-TCT)?

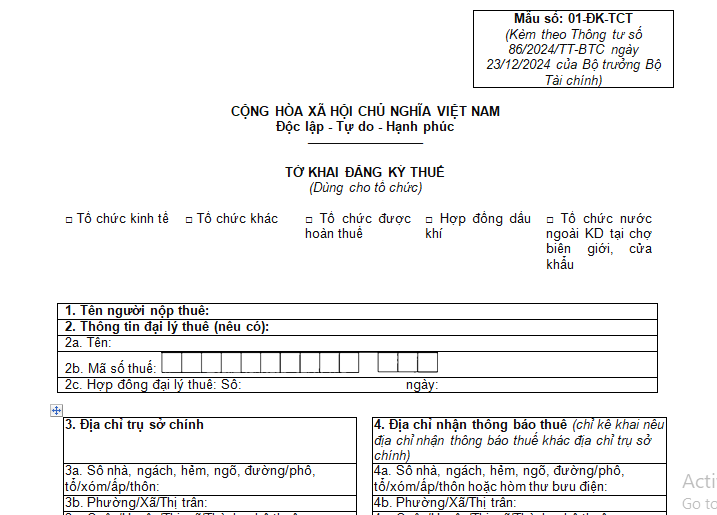

Currently, the tax registration application for sole proprietorships operating in specialized fields is used according to Form No. 01-DK-TCT issued together with Circular 105/2020/TT-BTC.

However, from February 06, 2025, the tax registration application for sole proprietorships operating in specialized fields will apply according to the new Form - Form No. 01-DK-TCT issued together with Circular 86/2024/TT-BTC.

DOWNLOAD >>> Form No. 01-DK-TCT

Note: This Declaration Form applies to sole proprietorships operating in specialized fields that are not required to register their business through the business registration authority under the provisions of specialized law (applicable to directly tax registration with the tax authority).

What is the Form for the tax registration application for sole proprietorships operating in specialized fields in Vietnam for 2025 (Form 01-DK-TCT)? (Image from the Internet)

What are guidelines for filling in the tax registration application for sole proprietorships operating in specialized fields in Vietnam for 2025 (Form 01-DK-TCT)?

According to Circular 86/2024/TT-BTC, the contents of the tax registration application for sole proprietorships operating in specialized fields (Form No. 01-DK-TCT) should be filled out as follows:

The taxpayer, being a sole proprietorship operating in a specialized field, must check the "Economic Organization" box before declaring detailed information. Specifically:

-

Taxpayer's Name: Clearly and fully write in uppercase the name of the organization according to the Establishment Decision or Establishment License and Operation or equivalent document issued by a competent authority (for Vietnamese organizations).

-

Tax Agent Information: Provide complete information of the tax agent in cases where the Tax Agent contracts with the taxpayer to carry out tax registration procedures on behalf of the taxpayer according to the Tax Administration Law regulations.

-

Headquarters Address: Clearly provide house number, alley, lane, street/road, village/hamlet, ward/commune, district/district-level town/city under the province, province/city of the taxpayer, phone number, Fax number (if any); clearly note area code - phone number/Fax number according to address information such as:

- Headquarters address of the taxpayer as an organization.

- The taxpayer must accurately and fully declare email information. This email address is used as an electronic transaction account with the tax authority regarding electronic tax registration documents.

-

Tax Notification Address: If the taxpayer is an organization with an address for receiving tax authority notifications different from the headquarters address in criterion 3 above, clearly state the tax notification address for tax authority contact.

-

Establishment Decision: (Not applicable)

-

Establishment License and Operation or Equivalent Documents issued by a competent authority: Clearly state the number, issuance date, and issuing authority for the Establishment License and Operation or equivalent documents issued by a competent authority (for taxpayer as a Vietnamese organization).

-

Main Business Activity: Write according to the business activity on the Establishment License and Operation or equivalent document issued by a competent authority (for taxpayer as a Vietnamese organization).

Note: Record only 1 actual main business activity.

-

Charter Capital: State according to investment capital on the Establishment License and Operation or equivalent document issued by a competent authority (specify currency type).

-

Start Date of Operation: Declare the date the taxpayer actually begins operation if different from the tax code issuance date.

-

Economic Type: Mark X on 1 box "sole proprietorship."

-

Accounting method for determining business results: Mark X on one of the two boxes “Independent” or “Dependent”. If selecting the “Independent” box, then mark “Has Consolidated Financial Statements” if required to prepare and submit consolidated financial statements to the tax authority according to regulations.

-

Fiscal Year: Clearly state from the start date, month of the accounting year to the end date, month of the financial year according to the calendar year or fiscal year of the taxpayer.

-

Information on the taxpayer's direct superior unit (if any): Clearly state the name, tax code of the direct superior management unit of the taxpayer as an organization.

-

Information on the owner of the sole proprietorship: Provide detailed information on the owner of the sole proprietorship. If the owner is a Vietnamese national, declare the personal identification number in criterion 14d and do not need to declare criterion 14đ, 14e.

The tax authority automatically integrates the information “permanent address,” “current address” of the individual from the National Population database to enter into criteria 14đ, 14e.

-

VAT calculation method: Mark X in the corresponding box of this criterion.

-

Information on related units:

- If the taxpayer has dependent units, mark X in the "Has dependent units" box, then declare in the “List of dependent units” according to Form BK02-DK-TCT.

- If the taxpayer has a business location, dependent warehouse without business functions, mark X in the "Has business locations, dependent warehouses" box, then declare in the “List of business locations” according to Form BK03-DK-TCT.

- If the taxpayer has a contract with a foreign contractor, subcontractor, mark X in the “Has contract with foreign contractor, foreign subcontractor” box, then declare in the “List of foreign contractors; foreign subcontractors” according to Form BK04-DK-TCT.

- If the taxpayer has an oil and gas contractor, investor, mark X in the “Has oil and gas contractor, investor” box, then declare in the “List of contractors, investors in oil and gas” according to Form BK05-DK-TCT (for oil and gas contracts).

-

Other Information: Clearly state full name, personal identification number (for Vietnamese) or personal tax code (for foreigners), contact phone number, email of the General Director or Director, Chief Accountant or accounting in charge of the taxpayer according to legal regulations.

-

Status before restructuring the organization (if any): If the taxpayer is an organization that carries out tax registration due to division/strip/merge of the organization, or conversion from a dependent unit to an independent unit, mark X in one of the corresponding boxes of this criterion and clearly state the previously assigned tax code of the divided, split, merged organization, or converted dependent unit.

-

Part for the taxpayer or legal representative of the taxpayer to sign and clearly state the full name: The taxpayer or the legal representative of the taxpayer must sign and clearly state the full name in this section.

-

Taxpayer's stamp:

If the taxpayer has a stamp at the time of tax registration, it must be stamped in this section (except when submitting documents electronically). If the taxpayer does not have a stamp at the time of tax registration, no stamp is required on the tax registration application. When the taxpayer collects the results, stamping must be added for the tax authority.

- Tax Agent Staff: If the tax agent declares on behalf of the taxpayer, declare this information.

How does the tax authority receive tax registration documents from sole proprietorships operating in specialized fields?

According to Clause 1, Article 6 of Circular 86/2024/TT-BTC and Clause 2, Article 41 of Tax Administration Law 2019, the tax authority receives tax registration documents from sole proprietorships operating in specialized fields through the following methods:

- Receive documents directly at the tax authority;

- Receive documents sent via postal services;

- Receive electronic files via the tax authority's electronic transaction portal and from the national information system on business, cooperative, business registration.