What is the form for notification of payment of land and housing registration fee by tax authority in Vietnam according to Decree 126?

What is the form for notification of payment of land and housing registration fee by tax authority in Vietnam according to Decree 126?

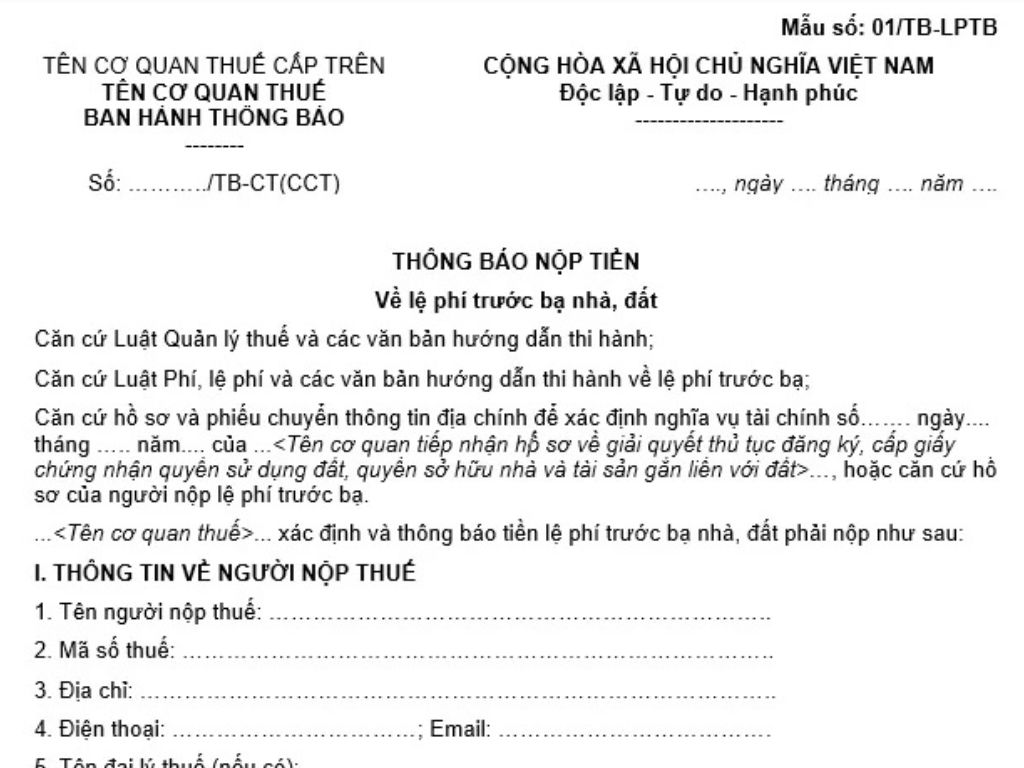

The Form for the notification of payment of land and housing registration fee by the tax authority is currently applied according to Form No. 01/TB-LPTB in Appendix 2 issued with Decree 126/2020/ND-CP.

Download the Form for the notification of payment of land and housing registration fee by the tax authority according to Decree 126 here

What is the form for notification of payment of land and housing registration fee by tax authority in Vietnam according to Decree 126? (Image from the Internet)

Where to submit the application for declaration of land and housing registration fee in Vietnam?

Based on point e, clause 7, Article 11 of Decree 126/2020/ND-CP, the regulation is as follows:

Location for submitting the tax declaration dossier for taxpayers with tax obligations arising from land-related revenues as stipulated in point c, clause 4, Article 45 of the Tax Management Law is as follows:

...

e) land and housing registration fee: Organizations and individuals registering for land use rights, housing ownership, and other assets attached to land (including cases exempt from registration fees) shall submit the registration fee declaration dossier at the one-stop shop where the real estate is located.

8. Location for submitting the tax declaration dossier for individual taxpayers with tax obligations arising from income from wages and salaries subject to personal income tax finalization as stipulated in point d, clause 4, Article 45 of the Tax Management Law is as follows:

a) Individuals directly filing taxes monthly or quarterly as stipulated in clause 1, Article 8, Article 9 of this Decree, including:

a.1) Resident individuals receiving income from wages and salaries paid by organizations and individuals in Vietnam subject to personal income tax but without tax withholding, shall submit the tax declaration dossier to the tax authority directly managing the income-paying organization or individual.

a.2) Resident individuals receiving income from wages and salaries paid from abroad shall submit the tax declaration dossier to the tax authority managing the location where the individual performs work in Vietnam. If the individual's work location is not in Vietnam, the individual shall submit the tax declaration dossier to the tax authority where the individual resides.

...

Thus, based on the aforementioned regulation, organizations and individuals with tax obligations arising from land-related revenues must submit the land and housing registration fee at the one-stop shop where the real estate is located when registering for land use rights, housing ownership, and other assets attached to land (including cases exempt from registration fees).

What is the deadline for paying the land and housing registration fee to the tax authority in Vietnam?

Based on clause 8, Article 18 of Decree 126/2020/ND-CP, the regulation on the deadline for paying the land and housing registration fee to the tax authority is as follows:

Tax payment deadlines for amounts payable to the state budget from land, water resource exploitation rights, mineral resources, usage of marine areas, registration fee, and license fee

...

8. registration fee: The deadline for paying the registration fee is no later than 30 days from the date of issuance of the notification, except in cases where the taxpayer is recorded as owing the registration fee.

9. License fee:

a) The deadline for paying the license fee is no later than January 30 each year.

b) For small and medium enterprises transitioning from household businesses (including dependent units and business locations of the enterprise) at the end of the exemption period (the fourth year from the year of enterprise establishment), the deadline for paying the license fee is as follows:

b.1) If the exemption period ends in the first 6 months of the year, the deadline for paying the license fee is no later than July 30 of the year when the exemption period ends.

b.2) If the exemption period ends in the last 6 months of the year, the deadline for paying the license fee is no later than January 30 of the year following the year when the exemption period ends.

c) If business households and individuals who have ceased production and business activities later resume operations, the deadline for paying the license fee is as follows:

c.1) If beginning operations in the first 6 months of the year: no later than July 30 of the year of resumption.

c.2) If beginning operations in the last 6 months of the year: no later than January 30 of the year following the year of resumption.

Thus, the deadline for paying the land and housing registration fee to the tax authority is no later than 30 days from the date of issuance of the notification.

*Note: Except in cases where the taxpayer is recorded as owing the registration fee.