What is the Form 41/UQ-DKT Power of Attorney for tax registration in Vietnam from February 6, 2025?

What is the Form 41/UQ-DKT Power of Attorney for tax registration in Vietnam from February 6, 2025?

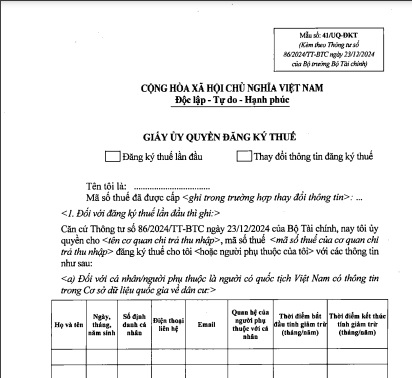

Form number 41/UQ-DKT Power of Attorney for tax registration from February 6, 2025 is issued in Appendix 2 promulgated together with Circular 86/2024/TT-BTC (document effective from February 6, 2025)

Form number 41/UQ-DKT Power of Attorney for tax registration from February 6, 2025 appears as follows:

Download Form 41/UQ-DKT Power of Attorney for tax registration PDF file...Here

Download Form 41/UQ-DKT Power of Attorney for tax registration Word file...Here

What does the initial tax registration dossier for individuals authorizing the income payer for tax registration include?

According to point b, clause 1, point b, clause 2 Article 22 of Circular 86/2024/TT-BTC regulating the initial tax registration dossier for individuals authorizing the income payer for tax registration as follows:

(1) In the case of individuals using identification numbers instead of TINs

- The tax registration dossier of the individual or dependent includes: Power of Attorney Form number 41/UQ-DKT issued together with Circular 86/2024/TT-BTC.

- The income payer is responsible for compiling the individual's tax registration information into tax registration declaration form number 05-DK-TH-TCT issued together with Circular 86/2024/TT-BTC, compiling dependent's tax registration information into tax registration declaration form number 20-DK-TH-TCT issued together with Circular 86/2024/TT-BTC, submitting to the tax authority managing the income payer directly.

The income payer uses the individual's personal identification number, or that of dependents, for withholding, declaring, and paying taxes as per legal regulations.

(2) In the case of individuals being issued TINs by the tax authority

- The tax registration dossier of the individual or dependent includes:

+ Power of Attorney Form number 41/UQ-DKT issued together with Circular 86/2024/TT-BTC;

+ A valid copy of the individual's or dependent’s passport or a valid copy of other legal personal identification documents (if there is no passport).

- The income payer is responsible for compiling the individual's tax registration information into tax registration declaration form number 05-DK-TH-TCT issued together with Circular 86/2024/TT-BTC, compiling dependent's tax registration information into tax registration declaration form number 20-DK-TH-TCT issued together with Circular 86/2024/TT-BTC, submitting to the tax authority managing the income payer directly.

The income payer uses the TIN issued by the tax authority for the individual or dependent for withholding, declaring, and paying taxes as per legal regulations.

Where to submit the initial tax registration dossier for individuals authorizing the income payer for tax registration in Vietnam?

According to point b, clause 1, point b, clause 2 Article 22 of Circular 86/2024/TT-BTC regulating the location for submitting the initial tax registration dossier for individuals authorizing the income payer for tax registration as follows:

(1) In the case of individuals using identification numbers instead of TINs

- At the income payer.

- In the case an individual pays personal income tax at multiple income-paying agencies within the same tax period, the individual only authorizes tax registration at one income payer and notifies the individual's personal identification number and that of the dependents to other income-paying agencies for use in withholding, declaring, and paying taxes.

(2) In the case of individuals being issued TINs by the tax authority

- At the income payer.

- In the case an individual pays personal income tax at multiple income-paying agencies within the same tax period, the individual only authorizes tax registration at one income payer to be issued a TIN by the tax authority. The individual notifies their TIN and that of the dependents to other income-paying agencies for use in withholding, declaring, and paying taxes.