What is the Form 20-DK-TCT on taxpayer registration declaration for dependants in Vietnam according to the Circular 86?

What is the Form 20-DK-TCT on taxpayer registration declaration for dependants in Vietnam according to the Circular 86?

Based on subpoint c.2 of point c, clause 1, subpoint c.2 of point c, clause 2, Article 22 of Circular 86/2024/TT-BTC (effective from February 6, 2025) prescribing the initial taxpayer registration dossier for individual households as follows:

Location for submitting and the initial taxpayer registration dossier

- For households and individuals specified at points i, k, l, n, clause 2, Article 4 of this Circular in cases of using a personal identification number instead of a tax code as prescribed in clause 5, Article 5 of this Circular.

...

c) In the case of individuals specified at points k, n, clause 2, Article 4 of this Circular who pay personal income tax not through an income paying agency or do not authorize the income payer for taxpayer registration.

...

c.2) taxpayer registration dossier:

- For individuals with taxable income: taxpayer registration declaration form No. 05-DK-TCT issued with this Circular.

- For dependants: taxpayer registration declaration form No. 20-DK-TCT issued with this Circular.

...

- For individuals specified at points i, k, l, n, clause 2, Article 4 of this Circular where the tax authority issues a tax code as prescribed in point a, clause 4, Article 5 of this Circular.

...

c) In the case of individuals specified at points k, n, clause 2, Article 4 of this Circular who pay personal income tax not through an income paying agency or do not authorize the income payer for taxpayer registration.

...

c.2) taxpayer registration dossier:

- For individuals with taxable income:

+ taxpayer registration declaration form No. 05-DK-TCT issued with this Circular and a valid passport copy of the individual.

A copy of the appointment document from the employing organization in the case of a foreign individual not residing in Vietnam as prescribed by personal income tax law assigned to work in Vietnam but receiving income abroad.

- For dependants:

+ taxpayer registration declaration form No. 20-DK-TCT issued with this Circular;

+ A valid passport copy of the dependent or a copy of other valid legal personal identification documents (if no passport is available).

...

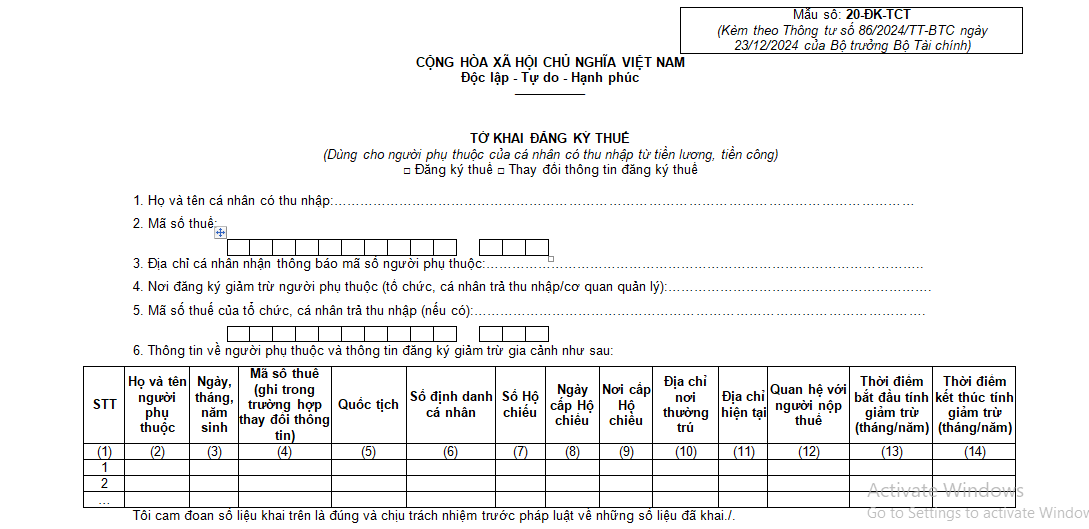

Thus, the taxpayer registration declaration for dependants is Form No. 20-DK-TCT issued in Annex 2 attached to Circular 86/2024/TT-BTC.

To be specific, Form 20-DK-TCT taxpayer registration declaration for dependants is structured as follows:

Download Form 20-DK-TCT taxpayer registration declaration for dependants.

What is the Form 20-DK-TCT on taxpayer registration declaration for dependants in Vietnam according to the Circular 86? (Image from the Internet)

Where is the location for submitting the initial taxpayer registration dossier for dependants of individuals not authorizing the income payer for taxpayer registration in Vietnam?

Based on point c, clause 1, point c, clause 2, Article 22 of Circular 86/2024/TT-BTC (effective from February 6, 2025) prescribing the location for submitting the initial taxpayer registration dossier for dependants of individuals not authorizing the income payer for taxpayer registration as follows:

(1) Case of individuals using an identification number instead of a tax code

- At the Tax Department where the individual works for resident individuals with income from salary or wages paid by International organizations, Embassies, or Consulates in Vietnam, but such organizations have not deducted tax.

- At the Tax Department where the work arises in Vietnam for individuals with income from salaries or wages paid by overseas organizations or individuals.

- At the Tax Sub-Department or Regional Tax Sub-Department where the individual resides in other cases.

(2) Case of individuals being issued a tax code by the tax authority

- At the Tax Department where the individual works for resident individuals with income from salary or wages paid by International organizations, Embassies, or Consulates in Vietnam, but such organizations have not deducted tax.

- At the Tax Department where the work arises in Vietnam for individuals with income from salaries or wages paid by overseas organizations or individuals.

What is the time limit for initial taxpayer registration in Vietnam?

Based on Article 33 of the Law on Tax Administration 2019, the time limit for initial taxpayer registration is prescribed as follows:

- Taxpayers who register taxpayers simultaneously with business registration, cooperative registration, or business registration will have the taxpayer registration time limit as the business registration time limit according to the provisions of the law.

- Taxpayers who register directly with the tax authority will have a taxpayer registration time limit of 10 working days from the following days:

+ Being granted a business registration certificate, establishment, and activity license, investment registration certificate, or establishment decision;

+ Beginning business activities for organizations not subject to business registration or business households, individuals subject to business registration but not yet granted a business registration certificate;

+ Arising responsibility for tax deduction and payment on behalf; organizations paying on behalf of individuals under business cooperation contracts;

+ Signing a contract to undertake foreign contractors or subcontractors paying tax directly with the tax authority; signing an oil and gas contract or agreement;

+ Arising obligation for personal income tax;

+ Arising requirement for tax refund;

+ Arising other obligations with the state budget.

- Organizations and individuals paying income have the responsibility to register taxpayers on behalf of individuals with income no later than 10 working days from the day of arising tax obligations in case the individual does not have a tax code; register on behalf of the dependants of the taxpayer no later than 10 working days from the day the taxpayer registers for family tax deduction according to legal provisions in case the dependent does not have a tax code.