What is the Form 18/TB-DKT - Notice of taxpayer’s TIN deactivation in Vietnam according to Circular 86?

What is the Form 18/TB-DKT - Notice of taxpayer’s TIN deactivation in Vietnam according to Circular 86?

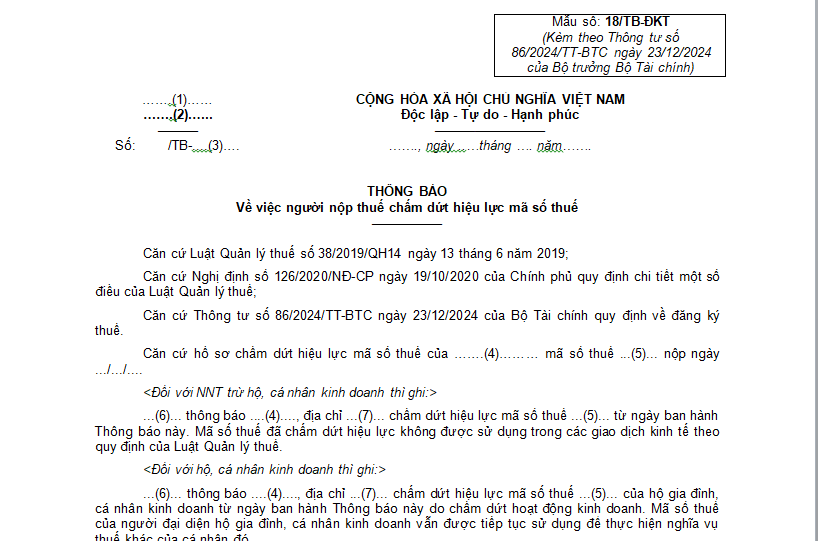

Form 18/TB-DKT is the notice form of taxpayer’s TIN deactivation as stipulated in Appendix II issued with Circular 86/2024/TT-BTC (effective from February 6, 2025). Form 18/TB-DKT is as follows:

Download Form 18/TB-DKT Notice on the deactivation of TIN Validity by a Taxpayer

What is the Form 18/TB-DKT - Notice of taxpayer’s TIN deactivation in Vietnam according to Circular 86? (Image from the Internet)

What does the application for TIN deactivation for organizations directly registering with the tax authority in Vietnam from February 6, 2025 include?

Based on Clause 1, Article 14 of Circular 86/2024/TT-BTC (effective from February 6, 2025), it is stipulated that the application for TIN deactivation for organizations directly registering with the tax authority includes a written request to deactivate the validity of the TIN using Form 24/DK-TCT issued with Circular 86/2024/TT-BTC and other documents as follows:

(1) For economic organizations and other organizations as specified in points a, b, c, d, n of Clause 2, Article 4 of Circular 86/2024/TT-BTC:

- For the managing unit, the application includes one of the following documents:

+ Copy of the dissolution decision, copy of division decision;

+ Copy of the merger agreement, copy of the consolidation agreement;

+ Copy of the decision to revoke the certificate of operation registration by the competent authority, copy of the notice of deactivation of operation, copy of the decision of transformation.

- If the managing unit has dependent units that have been assigned a 13-digit TIN, the managing unit must notify the dependent units to deactivate the TIN validity procedures with the tax authority managing the dependent unit before deactivating the TIN validity of the managing unit.

- In case the dependent unit deactivates the TIN validity without being able to fulfill the tax obligations to the state budget, the managing unit must provide a declaration of commitment to assume the responsibility of inheriting all the tax obligations of the dependent unit, sending it to the tax authority managing the dependent unit and continuing to fulfill the tax obligations of the dependent unit with the managing tax authority regarding the dependent unit's tax obligations after the TIN has been deactivated.

- For the dependent unit, the application includes one of the following documents:

+ Copy of the decision or notice to deactivate the dependent unit's operation;

+ Copy of the decision to revoke the operation registration certificate for the dependent unit by the competent authority.

(2) For contractors, investors in oil and gas contracts, the parent company - Vietnam Oil and Gas Group representing the host country receiving the divided profit from oil and gas contracts; foreign contractors, foreign sub-contractors as specified in point đ, h of Clause 2, Article 4 of Circular 86/2024/TT-BTC (excluding foreign contractors, foreign sub-contractors assigned a TIN under the provisions at point e of Clause 4, Article 5 of Circular 86/2024/TT-BTC), the application includes: A copy of contract liquidation documents or a copy of the document regarding the transfer of all capital contributions participating in oil and gas contracts for investors participating in oil and gas contracts.

How is the application for TIN deactivation for organizations directly registered with the tax authority in Vietnam processed from February 6, 2025?

Based on Clause 1, Article 16 of Circular 86/2024/TT-BTC (effective from February 6, 2025), regulations on processing the application for TIN deactivation for organizations directly registered with the tax authority are as follows:

(1) The directly managing tax authority shall:

(i) Issue a Notice on the suspension of activities for taxpayers and commencement of TIN validity deactivation procedures using Form 17/TB-DKT issued with Circular 86/2024/TT-BTC to be sent to the taxpayer within 02 (two) working days from the date the tax authority receives the complete application for TIN validity deactivation as prescribed.

Issue Notices to managing units and dependent units using Form 35/TB-DKT issued with Circular 86/2024/TT-BTC in the event the tax authority receives a application for TIN validity deactivation of the managing unit, but the dependent units have not yet implemented the TIN validity deactivation procedures.

(ii) Coordinate with the tax authority managing the revenue where the taxpayer incurs obligations to the state budget to finalize the taxpayer's obligations at the tax authority managing the revenue (fully submit tax declaration application, complete tax payment obligations, obligations on invoices, and handle overpaid taxes, uncredited VAT (if any)), and process tax obligation offsets or refunds in accordance with legal regulations.

(iii) Execute the procedures for offset or refunding against other tax obligations of the taxpayer in accordance with the Law on Tax Administration and its guiding documents.

- In cases where the dependent unit deactivates the TIN validity but cannot complete the pending obligations or is still in debt, or there is an overpayment, uncredited VAT after performing offsets or refunding against according to the provisions of the Law on Tax Administration and its guiding documents, if the managing unit has made a declaration of commitment to assume full responsibility for all tax obligations of the dependent unit, the customs office, or the directly managing tax authority of the dependent unit shall transfer the obligation of the dependent unit to the managing unit and issue a Notice on the transfer of taxpayer's tax obligation using Form 39/TB-DKT issued with Circular 86/2024/TT-BTC to be sent to the taxpayer, which is the managing unit, dependent unit, and the directly managing tax authority of the managing unit.

- In cases where the divided, merged, or consolidated unit deactivates the TIN validity but cannot complete the pending obligations or is still in debt, or there is an overpayment, uncredited VAT after performing offsets or refunding against according to the provisions of the Law on Tax Administration and its guiding documents, should new units established from the divided, merged, or consolidated unit agree on inheriting all tax obligations of the divided, merged, or consolidated unit, the customs office or directly managing tax authority of the divided, merged, or consolidated unit shall transfer the obligation to the new unit and issue a Notice on the transfer of taxpayer's tax obligation using Form 39/TB-DKT issued with Circular 86/2024/TT-BTC to be sent to the taxpayer, which is the divided, merged, or consolidated unit, the new units, and the tax authority directly managing the new units.

(iv) Request the Customs authority to confirm that the taxpayer has completed tax and other payments obligations to the state budget regarding import-export activities according to the regulations specified in the Ministry of Finance's Circulars on customs procedures; customs supervision and administration; export-import taxes and tax management for export-import goods and Circulars of the Ministry of Finance regulating electronic transactions in the tax domain within 03 days from the issuance date of the Notice on the taxpayer's suspension of activity and TIN validity deactivation procedures.

(v) Issue a Notice on the deactivation of taxpayer's TIN validity using Form 18/TB-DKT issued with Circular 86/2024/TT-BTC within 03 (three) working days from the date the taxpayer has completed tax obligations with the managing tax authority or the tax authority has completed transferring all tax obligations and other payments to the state budget from the dependent unit to the managing unit, from the divided, merged, or consolidated unit to the new unit.

(2) The tax authority managing the revenue shall:

- Perform the tasks specified in sections (ii) and (iii) above concerning revenue generated in the locality.

- Update the taxpayer's information once they have fulfilled the tax obligations concerning revenue under the tax authority's management into the Taxpayer Registration System on the same working day or by the start of the next working day at the latest after the taxpayer completes tax payment obligations at the revenue managing tax authority.