What is the Form 08-MST for Application form for amendments to tax registration in Vietnam?

What is the Form 08-MST - Application form for amendments to tax registration in Vietnam?

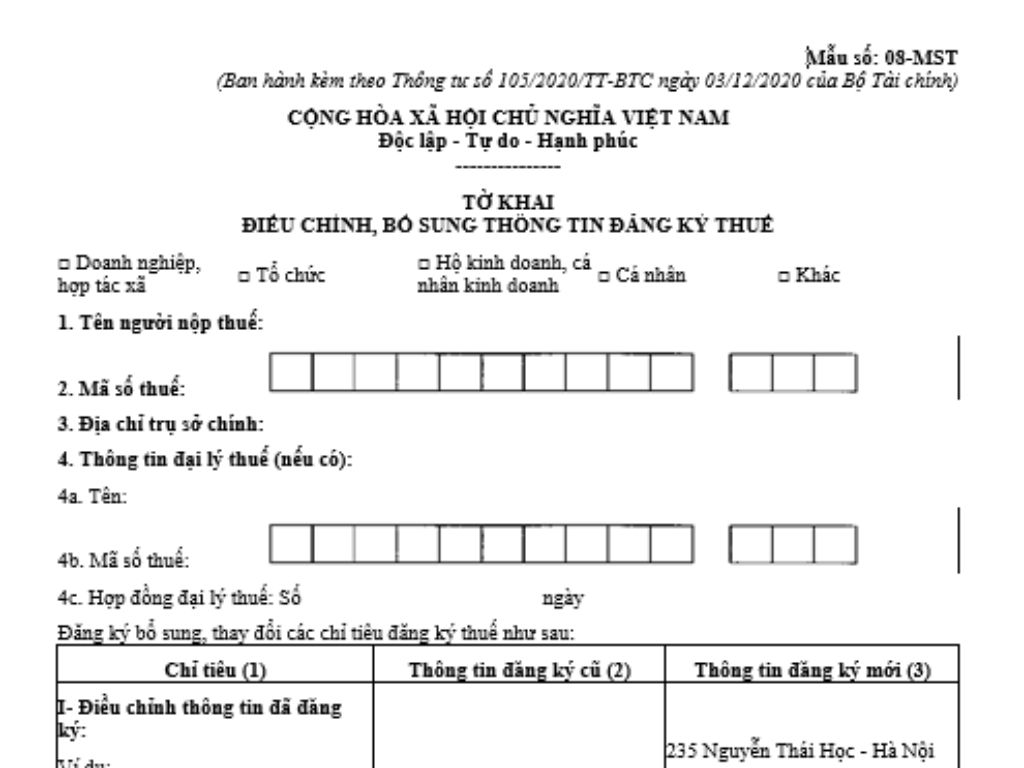

The latest Form 08-MST is stipulated in Circular 105/2020/TT-BTC, used in cases of amendments to taxpayer registration information. To be specific:

The latest Form 08-MST for amendments to taxpayer registration Download

What is the Form 08-MST for Application form for amendments to tax registration in Vietnam? (Image from the Internet)

How to notify changes in taxpayer registration information in Vietnam?

According to Article 36 of the Law on Tax Administration 2019 regulating the notification of changes in taxpayer registration information as follows:

- Taxpayers registering with business registration, cooperative registration, or business registration who have changes in taxpayer registration information must notify changes in taxpayer registration information along with changes in business registration, cooperative registration, or business registration contents according to legal regulations.

In the case a taxpayer changes the registered head office address leading to a change in the managing tax authority, the taxpayer must conduct tax-related procedures with the directly managing tax authority according to the Law on Tax Administration 2019 before registering the change with the business registration authority, cooperative registration, or business registration.

- Taxpayers registering directly with the tax authority must notify the directly managing tax authority within 10 working days from the date the change occurs.

- In case an individual authorizes an organization, an individual who pays income implements registration for change of taxpayer registration information for the individual and dependents, they must notify the organization or individual paying income no later than 10 working days from the date the change occurs; the organization or individual paying income is responsible for notifying the tax management authority no later than 10 working days from the date they receive the authorization from the individual.

What is the penalty for late notification of changes in taxpayer registration information in Vietnam?

According to Article 11 of Decree 125/2020/ND-CP stipulating as follows:

Penalty for Violations on Notification Deadline for Changes in Taxpayer Registration Information

1. A warning is issued for any of the following acts:

a) Notification of changes in the taxpayer registration content beyond the prescribed deadline from 01 to 30 days without changing the taxpayer registration certificate or tax identification number notification with extenuating circumstances;

b) Notification of changes in the taxpayer registration content beyond the prescribed deadline from 01 to 10 days making changes to the taxpayer registration certificate or tax identification number notification with extenuating circumstances.

2. A fine from 500,000 VND to 1,000,000 VND is imposed for notifying changes in the taxpayer registration content beyond the prescribed deadline from 01 to 30 days without changing the taxpayer registration certificate or tax identification number notification, except for penalties under point a, clause 1 of this Article.

3. A fine from 1,000,000 VND to 3,000,000 VND for any of the following acts:

a) Notification of changes in the taxpayer registration content beyond the prescribed deadline from 31 to 90 days without changing the taxpayer registration certificate or tax identification number notification;

b) Notification of changes in the taxpayer registration content beyond the prescribed deadline from 01 to 30 days making changes to the taxpayer registration certificate or tax identification number notification, except as prescribed at point b, clause 1 of this Article.

4. A fine from 3,000,000 VND to 5,000,000 VND for any of the following acts:

a) Notification of changes in the taxpayer registration content beyond the prescribed deadline from 91 days or more without changing the taxpayer registration certificate or tax identification number notification;

b) Notification of changes in the taxpayer registration content beyond the prescribed deadline from 31 to 90 days making changes to the taxpayer registration certificate or tax identification number notification.

5. A fine from 5,000,000 VND to 7,000,000 VND for any of the following acts:

a) Notification of changes in the taxpayer registration content beyond the prescribed deadline from 91 days or more making changes to the taxpayer registration certificate or tax identification number notification;

b) Failure to notify changes in information in the taxpayer registration documents.

6. The regulations in this Article do not apply to the following cases:

a) Individuals not engaged in business have been issued a personal income tax identification number slowly change information about ID card when issued a personal identification card;

b) Income-paying bodies delay notification of change in ID card information when the personal income tax individual is authorized for personal income tax finalization and is issued a personal identification card;

c) Notification of changes in taxpayer registration document information regarding taxpayer address beyond the prescribed deadline due to administrative boundary changes following a resolution of the Standing Committee of the National Assembly or a resolution of the National Assembly.

7. Remedial Measures: Must submit change dossiers for taxpayer registration content for the acts specified at point b, clause 5 of this Article.

excluding cases in Article 9 of Decree 125/2020/ND-CP, the failure to promptly notify changes in taxpayer registration information may be subject to administrative penalties as outlined above with the lowest penalty being a warning and the highest fine being 7 million VND.

Note: This monetary penalty applies to organizations, the penalty for individuals is 1/2 of the above-mentioned penalty.