What is the Form 08/CK-TNCN on personal income tax commitment form in Vietnam?

What is the Form 08/CK-TNCN on personal income tax commitment form in Vietnam?

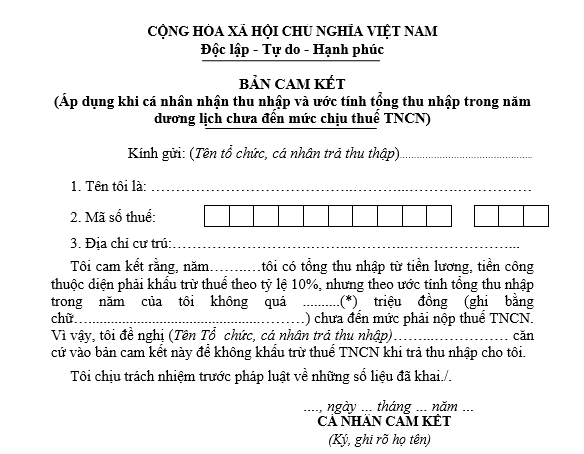

The latest personal income tax commitment form is Form 08/CK-TNCN, issued with Circular 80/2021/TT-BTC.

Form 08/CK-TNCN is structured as follows:

Download Form 08/CK-TNCN: personal income tax commitment

What is the Form 08/CK-TNCN on personal income tax commitment form in Vietnam? (Image from the Internet)

Who is eligible for the personal income tax commitment in Vietnam?

Based on point i, clause 1, Article 25 of Circular 111/2013/TT-BTC, the regulations on commitment of no personal income tax incurrence are as follows:

Tax Deduction and Tax Deduction Certificate

- Tax Deduction

Tax deduction is the process by which organizations or individuals paying income implement the deduction of tax payable from the income of the taxpayer before making the payment. Specifically:

...

i) Tax deduction for certain other cases

Organizations and individuals paying wages, remuneration, or other payments to resident individuals who do not have a labor contract (as guided at points c, d, clause 2, Article 2 of this Circular) or have labor contracts of less than three (03) months and have a total income payment from two million (2,000,000) VND or more per payment must deduct tax at a rate of 10% on the income before making the payment to the individual.

If an individual has only the income subject to tax deduction as mentioned above but estimates that their total taxable income, after personal exemption for dependents, does not reach the taxable level, the income-earning individual can make a commitment (using the form issued together with the tax management guidance document) to be sent to the income-paying organization so that the organization has a basis to temporarily refrain from withholding personal income tax.

Based on the income recipient's commitment, the paying organization will not deduct tax. At the end of the tax year, the paying organization must still consolidate the list and the income of individuals not reaching the deduction level (in the form issued together with the tax management guidance document) and submit it to the tax authority. The individual making the commitment must take responsibility for their commitment, and if fraud is detected, they will be dealt with according to the tax management law.

Individuals making commitments, as guided at this point, must have taxpayer registration and a tax code at the time of commitment.

...

According to the above regulations, the declaration of commitment of no personal income tax incurrence applies to individuals meeting the following conditions:

- Resident individuals without a labor contract or with a labor contract of less than three (03) months.

- Having a total income payment of two million VND or more per payment.

- Having only the income subject to tax deduction. If working at two or more places, they are not eligible to make the commitment.

- Must have taxpayer registration and a tax code at the time of commitment.

- Estimate that the total taxable income, after deducting personal and family circumstances, does not reach the taxable level (total income up to 132 million VND per year for those without dependents).

What is the personal exemption level for taxpayers in Vietnam?

According to Article 1 of Resolution 954/2020/UBTVQH14, the regulation is as follows:

Personal and Family Circumstances Deduction Levels

Adjustment to the personal and family deduction level stipulated in clause 1, Article 19 of the Personal Income Tax Law No. 04/2007/QH12, amended and supplemented by Law No. 26/2012/QH13, is as follows:

- The deduction level for taxpayers is 11 million VND per month (132 million VND per year);

- The deduction level for each dependent is 4.4 million VND per month.

Thus, the personal exemption level for taxpayers is currently 11 million VND per month (132 million VND per year).

Who is considered a personal income taxpayer in Vietnam?

Based on Article 2 of the Personal Income Tax Law 2007, individual personal income taxpayers are resident individuals with taxable income stipulated in Article 3 of the Personal Income Tax Law 2007 that arises within and outside the territory of Vietnam and non-resident individuals with taxable income stipulated in Article 3 of the Personal Income Tax Law 2007 that arises within the territory of Vietnam. Wherein:

- A resident individual is someone who meets one of the following conditions:

+ Present in Vietnam for 183 days or more within a calendar year or within 12 consecutive months from the first day of presence in Vietnam;

+ Have a permanent residence in Vietnam, including registered permanent residence or a leased house for residence in Vietnam as per a lease contract with a term.

- A non-resident individual is someone who does not meet the following conditions:

+ Present in Vietnam for 183 days or more within a calendar year or within 12 consecutive months from the first day present in Vietnam;

+ Have a permanent residence in Vietnam, including registered permanent residence or a leased house for residence in Vietnam per a lease contract with a term.