What is the Form 04-DK-TCT - Tax registration application form for foreign contractors in Vietnam?

What is the Form 04-DK-TCT - Tax registration application form for foreign contractors in Vietnam?

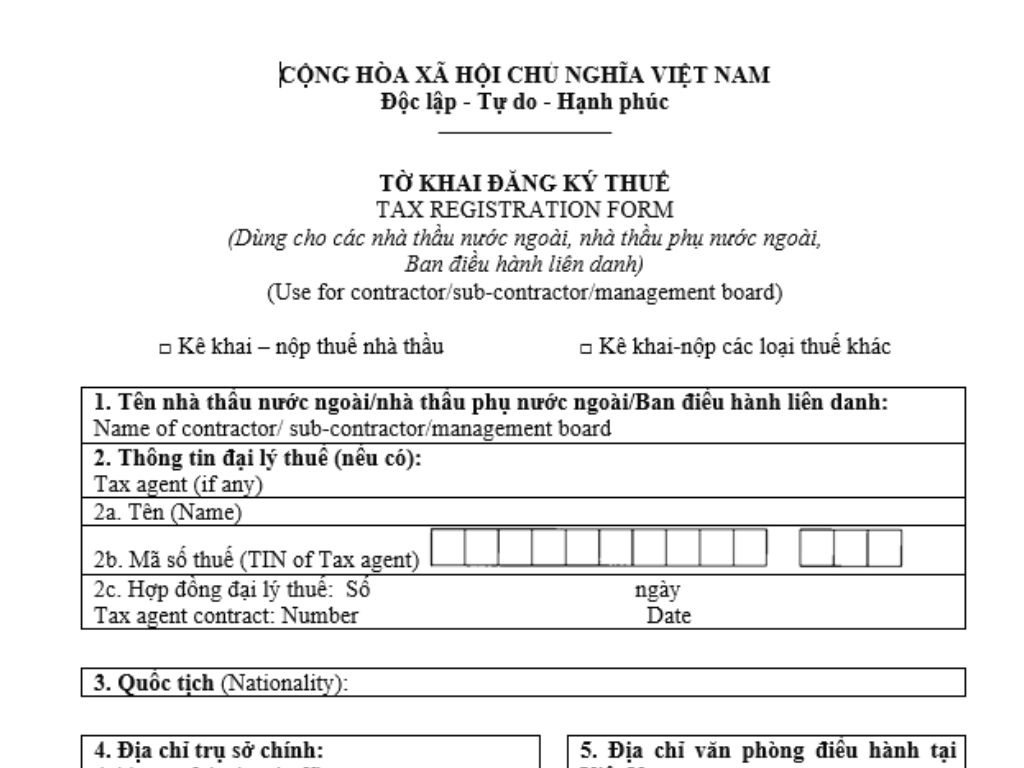

Form 04-DK-TCT is a tax registration application form used for foreign contractors, foreign subcontractors, and joint operation executive boards. Form 04-DK-TCT is specified in Appendix 2 issued together with Circular 86/2024/TT-BTC as follows:

The latest Form 04-DK-TCT for taxpayer registration used for foreign contractors can be downloaded here.

What is the Form 04-DK-TCT - Tax registration application form for foreign contractors in Vietnam? (Image from the Internet)

Vietnam: What does the initial tax registration application for foreign contractors include from February 6, 2025?

Based on Clause 4, Article 7 of Circular 86/2024/TT-BTC (effective from February 6, 2025) which stipulates the submission places and initial tax registration application:

Submission Place and Initial tax registration application

...

4. For taxpayers who are foreign contractors, foreign subcontractors stipulated at Point đ, Clause 2, Article 4 of this Circular directly declaring and paying contractor tax or other tax obligations except contractor tax deducted and paid by the Vietnamese party according to the law on tax administration, the initial tax registration application is submitted at the Tax Department where their office is located. The tax registration application includes:

- tax registration application form No. 04-DK-TCT issued with this Circular;

- List of foreign contractors, foreign subcontractors form No. BK04-DK-TCT issued with this Circular (if any);

- Copy of the Certificate of Registration for Operating Office or equivalent document issued by a competent authority (if any).

...

Thus, the tax registration application for foreign contractors includes the following documents:

- tax registration application form

- List of foreign contractors, foreign subcontractors

- Copy of Certificate of Registration for Operating Office or equivalent document issued by a competent authority (if any).

What are regulations on the receipt of tax registration application in Vietnam from February 6, 2025?

Based on Article 6 of Circular 86/2024/TT-BTC (effective from February 6, 2025) which stipulates the reception of tax registration application as follows:

- For paper dossiers:

+ In cases where tax registration applications are submitted directly to the tax authority, tax officials shall check the tax registration applications. If the dossier is complete as prescribed, the tax official shall accept and affix a receipt stamp on the tax registration application, clearly indicating the date of receipt, and the number of documents according to the list of dossier contents; issue a receipt slip and an appointment to return the results for dossiers where the tax authority must return results to the taxpayers; and handle the dossier within the deadline for each type of dossier received. If the dossier is incomplete as prescribed, the tax official will not accept and guide the taxpayer to complete the dossier.

+ In cases where tax registration applications are sent by postal service, the tax official shall affix a receipt stamp, note the date of receipt on the dossier, and enter it into the tax authority's correspondence book. If the dossier is incomplete and requires explanation or additional information, the tax authority shall notify the taxpayer using form No. 01/TB-BSTT-NNT in Appendix II issued together with Decree No. 126/2020/ND-CP dated October 19, 2020, of the Government of Vietnam detailing some articles of the Law on Tax Administration within 02 (two) working days from the date of receipt of the dossier.

- For electronic tax registration applications: The reception of dossiers is executed as prescribed in Articles 13 and 14 of Circular No. 19/2021/TT-BTC dated March 18, 2021 of the Ministry of Finance guiding electronic transactions in the field of taxation and Circular No. 46/2024/TT-BTC dated July 9, 2024, amending and supplementing some articles of Circular No. 19/2021/TT-BTC (hereinafter referred to as Circular No. 19/2021/TT-BTC).

- Receiving decisions, documents, or other papers related to taxpayer registration from competent state agencies

+ For decisions, documents, or other papers in paper form:

Tax officers shall receive and affix receipt stamps on the decisions, documents, or other papers of competent state agencies, noting the date of receipt in the decisions, documents, or other papers received.

In case the decisions, documents, or other papers are sent by postal service, the tax official shall affix a receipt stamp, note the date of receipt on the decisions, documents, or other papers received, and enter it into the tax authority's correspondence book.

+ For decisions, documents, or other papers in electronic form: The reception of decisions, documents, or other papers from competent state agencies electronically shall be implemented as prescribed regarding electronic transactions in the financial and tax sector.

Note: tax registration applications include initial tax registration application; dossier for changing taxpayer registration information; notification of temporary cessation of operations or business or resumption of business before the cessation period; dossier for termination of tax code validity; dossier for tax code restoration, received as prescribed in Clauses 2, 3, Article 41 of the Law on Tax Administration 2019.