What is the Form 01/LPMB on licensing fee declaration in Vietnam for 2025 under the Circular 80?

What is the Form 01/LPMB on licensing fee declaration in Vietnam for 2025 under the Circular 80?

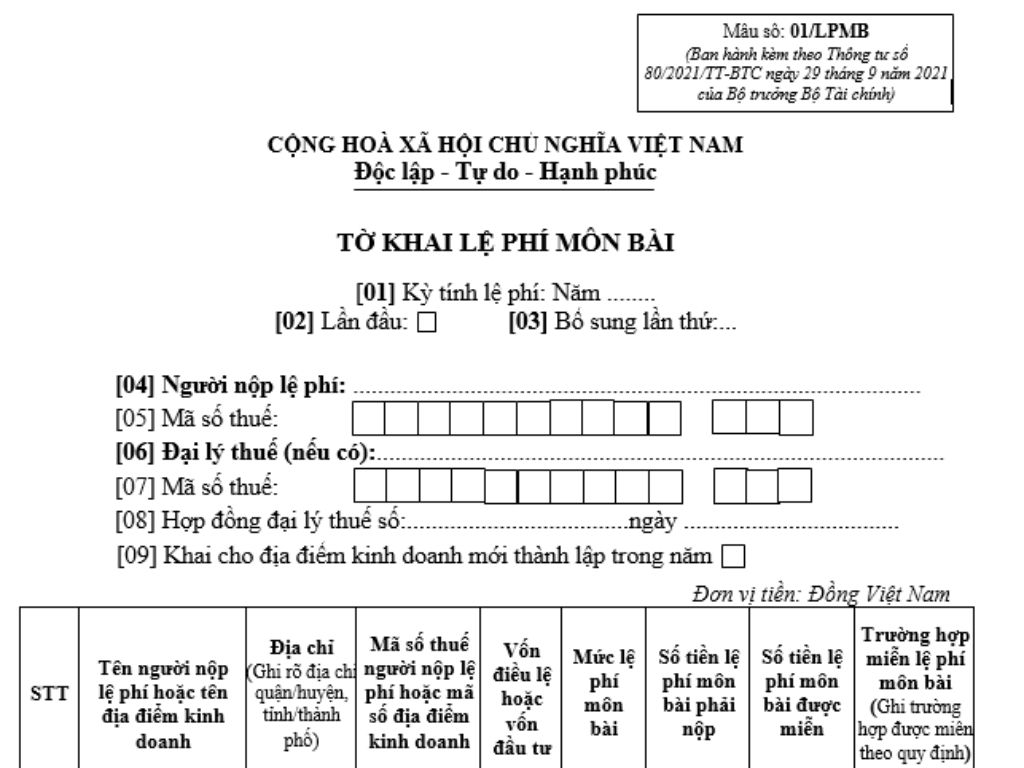

The latest licensing fee declaration form for 2024, previously known as the licensing fee return, is Form 01/LPMB in Appendix 2 issued under Circular 80/2021/TT-BTC.

Download the latest Word file of Form 01/LPMB licensing fee Declaration for 2025 according to Circular 80 here.

Instructions for Completing the licensing fee Declaration Form for 2025

- Indicator [01]: Declare the year the licensing fee is calculated.

- Indicator [02]: Check this box for the first-time declaration.

- Indicator [03]: Check this box if the taxpayer has submitted the declaration but later discovers there are changes in the declaration obligation and needs to re-declare the information for the declared tax period. Note that taxpayer should only select one of the two indicators [02] and [03], not both simultaneously.

- Indicators [04] to [05]: Declare information according to the taxpayer's registration.

- Indicators [06] to [08]: Declare tax agent information (if any).

- Indicator [09]: Check this box if taxpayer has declared licensing fee and then establishes a new business location.

What is the Form 01/LPMB on licensing fee declaration in Vietnam for 2025 under the Circular 80? (Image from Internet)

Which entities are licensing fee payers in Vietnam in 2025?

According to Article 2 of Decree 139/2016/ND-CP, entities required to pay licensing fee include:

- Enterprises established according to legal provisions.

- Organizations established under the Cooperative Law.

- Public service units established according to the law.

- Economic organizations of political organizations, socio-political organizations, social organizations, professional-social organizations, and people's armed units.

- Other organizations engaged in production and business activities.

- Branches, representative offices, and business locations of the organizations specified in Clauses 1, 2, 3, 4, and 5 of Article 2 Decree 139/2016/ND-CP (if any).

- Individuals, groups of individuals, and households engaged in production and business activities.

Which cases are exempted from licensing fee in Vietnam in 2025?

Based on Article 3 of Decree 139/2016/ND-CP (amended by Clause 1, Article 1 of Decree 22/2020/ND-CP), exemptions include:

- Individuals, groups of individuals, and households engaged in production and business activities with annual revenue not exceeding 100 million VND.

- Individuals, groups of individuals, and households engaged in irregular production and business activities without fixed locations according to the Ministry of Finance's guidance.

- Individuals, groups of individuals, and households engaged in salt production.

- Organizations, individuals, groups of individuals, and households engaged in aquaculture, fishing, and fishing support services.

- Communal cultural postal points; press agencies (print, audio, visual, electronic).

- Cooperatives, cooperative unions (including branches, representative offices, business locations) operating in the agricultural sector as per legal regulations on agricultural cooperatives.

- People's credit funds; branches, representative offices, and business locations of cooperatives, cooperative unions, and private enterprises operating in mountainous areas. Mountainous areas are defined according to the Committee on Ethnic Minority Affairs' regulations.

- Exemption from licensing fee for the first year of establishment or commencement of production and business activities (from January 1 to December 31) for:

+ Newly established organizations (with new tax code or business ID).

+ Households, individuals, and groups of individuals commencing production and business for the first time.

+ During the exemption period, if organizations, households, individuals, or groups of individuals establish branches, representative offices, or business locations, these too are licensing fee-exempt for the duration the organization, household, or individual is exempt.

- Small and medium enterprises (SMEs) transitioning from household businesses are exempt from licensing fee for up to 3 years from the first business registration certificate issuance date.

+ During the exemption period, if SMEs establish branches, representative offices, or business locations, these too are licensing fee-exempt for the same period as the SME.

+ Branches, representative offices, and business locations of SMEs (eligible for licensing fee exemption per Article 16 of the Law on Support for Small and Medium Enterprises 2017) established before this Decree takes effect will have their exemption period start from this Decree's effective date and extend throughout the SME's exemption period.

+ SMEs transitioning from household businesses before this Decree's effective date apply the licensing fee exemption according to Articles 16 and 35 of the Law on Support for Small and Medium Enterprises 2017.

- Public pre-school and public general education institutions.