What is the Form 01/ADT: Tax imposition decision issued by tax authorities in Vietnam?

What is the Form 01/ADT: Tax imposition decision issued by tax authorities in Vietnam?

Based on Clause 3, Article 16 of Decree 126/2020/ND-CP regarding the tax imposition decision of the tax authority as follows:

Authority, Procedure, and Tax Imposition Decision

...

3. Tax Imposition Decision

a) When imposing tax, the tax authority must issue a tax imposition decision according to Form No. 01/ADT in Appendix III issued with this Decree, and send it to the taxpayer within 03 working days from the date of the decision;

In case the taxpayer is subject to tax payment according to the notification of the tax authority, the tax authority is not required to issue a tax imposition decision according to this clause.

b) The taxpayer must pay the imposed tax amount according to the tax handling decision of the tax authority. If the taxpayer disagrees with the imposed tax amount, they must still pay that tax amount, while having the right to request an explanation from the tax authority or lodge a complaint or initiate legal proceedings regarding the tax imposition.

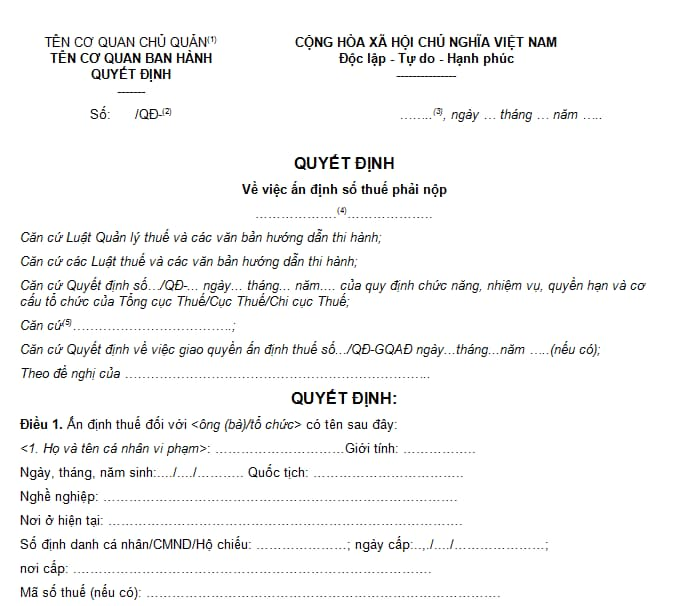

The tax imposition decision of the tax authority is issued according to Form No. 01/ADT in Appendix 3 issued with Decree 126/2020/ND-CP as follows:

Download Form 01/ADT: Here

What is the Form 01/ADT: Tax imposition decision issued by tax authorities in Vietnam? (Image from the Internet)

When does a tax authority issue a tax imposition decision in Vietnam?

According to Article 14 of Decree 126/2020/ND-CP, taxpayers in the following cases will be subject to tax imposition by the tax authority:

- Failing to register as a taxpayer as stipulated in Article 33 of the Law on Tax Administration 2019.

- Failing to declare tax or declaring tax incompletely, truthfully, and accurately as stipulated in Article 42 of the Law on Tax Administration 2019.

- Failing to provide supplementary tax documentation as requested by the tax authority or providing incomplete, dishonest, and inaccurate tax documentation that serves as the basis for tax calculation.

- Failing to reflect or reflecting incompletely, dishonestly, and inaccurately the data in the accounting books to determine tax liabilities.

- Failing to present accounting books, invoices, vouchers, and necessary documents related to determining the factors for tax calculation; determining the payable tax amount within the stipulated time or after the deadline for tax inspection, tax audit at the taxpayer's office.

- Failing to comply with the tax inspection decision within 10 working days from the date of the decision, unless the inspection period is postponed as regulated.

- Failing to comply with the tax audit decision within 15 days from the date of the decision, unless the audit period is postponed as regulated.

- Buying, selling, exchanging, and accounting the value of goods and services not according to the usual market transaction value.

- Buying, exchanging goods, services using illegal invoices, using fraudulent invoices while the goods and services are genuinely verified by investigative, inspection, or audit authorities and declared revenue and tax deductible expenses.

- Showing signs of absconding or dispersing assets to evade tax obligations.

- Conducting transactions that do not reflect the economic essence, not genuinely arising to reduce the taxpayer's tax obligations.

- Failing to comply with regulations on declaration obligations, determining transfer pricing or failing to provide information as stipulated regarding tax administration for enterprises arising in related-party transactions.

Which entity has the authority to issue a tax imposition decision in Vietnam?

Based on Article 16 of Decree 126/2020/ND-CP, the regulation is as follows:

Authority, Procedure, and Tax Imposition Decision

1. Authority to Impose Tax

The Director General of the General Department of Taxation; the Director of the Tax Department; the Head of the Tax Department have the authority to impose tax.

2. Tax Imposition Procedure

a) When imposing tax, the tax authority shall notify the taxpayer in writing about the tax imposition and issue a tax imposition decision. The tax imposition decision must specify the reason for tax imposition, the basis for tax imposition, the imposed tax amount, and the deadline for payment.

b) If the tax authority carries out tax imposition after tax inspection, tax audit, the reasons for tax imposition, the basis for tax imposition, the imposed tax amount, and the deadline for payment must be stated in the tax inspection, tax audit record, tax handling decision of the tax authority.

c) If the taxpayer is subject to tax imposition as regulated, the tax authority will impose administrative penalties and calculate late payment penalties according to the laws.

3. Tax Imposition Decision

a) When imposing tax, the tax authority must issue a tax imposition decision according to Form No. 01/ADT in Appendix III issued with this Decree, and send it to the taxpayer within 03 working days from the date of signing the tax imposition decision;

In the case where the taxpayer is subject to tax payment according to the notification of the tax authority, the tax authority is not required to issue a tax imposition decision according to this clause.

b) The taxpayer must pay the imposed tax amount according to the tax handling decision of the tax authority. If the taxpayer disagrees with the imposed tax amount, they must still pay that tax amount, while having the right to request an explanation from the tax authority or lodge a complaint or initiate legal proceedings regarding the tax imposition.

The following individuals have the authority to impose tax:

- Director General of the General Department of Taxation

- Director of the Tax Department

- Head of the Tax Department