What is the fixed asset liquidation minutes form in Vietnam according to Circular 200/2014?

What is the fixed asset liquidation minutes form in Vietnam according to Circular 200/2014?

The fixed asset liquidation minutes is an important legal document in the process of handling assets that are no longer useful or unnecessary for the business operations of an enterprise. According to the regulations in Circular 200/2014/TT-BTC, the preparation of fixed asset liquidation minutes helps clarify the reasons, procedures, and liquidation value of the asset, while ensuring compliance with tax and accounting regulations.

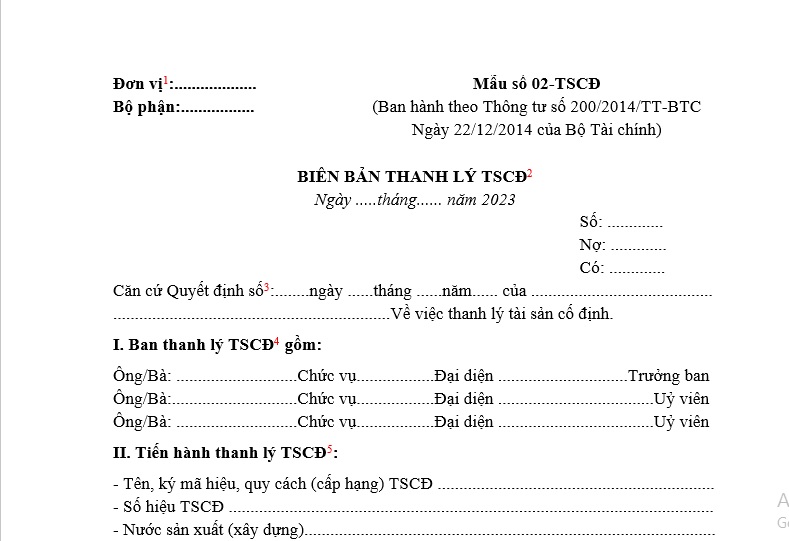

The template for the fixed asset liquidation minutes is form 02-TSCĐ issued together with Circular 200/2014/TT-BTC

The template for the fixed asset liquidation minutes according to Circular 200/2014...Download

How to fill out fixed asset liquidation minutes in Vietnam according to Circular 200/2014?

Below are detailed instructions on how to fill out the fixed asset liquidation minutes issued together with Circular 200/2014/TT-BTC:

(1) Clearly state the name of the unit (or stamp the unit), and the department using this document.

(2) - The fixed asset liquidation minutes is intended to confirm the liquidation of fixed assets and serve as the basis for recording the reduction of fixed assets in the accounting books.

- The liquidation minutes must be prepared by the asset liquidation committee and include full signatures with clearly stated names of the head of the liquidation committee, chief accountant, and the director of the enterprise.

(3) Record the serial number, time, and the entity making the decision to liquidate the fixed assets.

(4) Record the names, positions, and representatives of the members of the fixed asset liquidation committee.

(5) Record general indicators regarding the fixed assets subject to liquidation.

(6) Record the conclusions of the liquidation committee, and note the committee's comments on the asset liquidation.

(7) After liquidation is completed, based on calculations of total actual liquidation expenses and recovered value, record the liquidation expenses and recovered value (the value of spare parts and scrap recovered calculated at actual sale price or estimated sales price).

What is the fixed asset liquidation minutes form in Vietnam according to Circular 200/2014? (Image from the Internet)

Vietnam: What is a fixed asset? How many types of fixed asset are there?

Currently, there is no document that provides a general definition of fixed assets, but to be identified as a fixed asset, the asset must have a usage period of over 1 year and a value of 30 million VND or more... Although there is no general definition, Article 2 of Circular 45/2013/TT-BTC provides specific definitions for each type of fixed asset as follows:

(1) Tangible Fixed Assets: These are primary labor tools with physical form meeting the standards of tangible fixed assets, participating in many business cycles while maintaining their original physical form such as buildings, structures, machinery, equipment, vehicles...

(2) Intangible Fixed Assets: These are assets without physical form, representing an amount of value that has been invested that meets the standards of intangible fixed assets, participating in many business cycles, such as some costs directly related to the use of the land; costs for rights issuance, patents, copyrights...

(3) Financial Lease Fixed Assets: These are fixed assets that an enterprise leases from a financial leasing company. At the end of the lease period, the lessee has the option to purchase the leased asset or continue leasing under the conditions agreed in the financial lease contract. The total lease payment for a type of asset specified in the financial lease contract must be at least equivalent to the value of the asset at the time of signing the contract.

All leased fixed assets that do not meet the above provisions are considered as operational lease fixed assets.

(4) Similar Fixed Assets: These are fixed assets with similar functions within the same business field and equivalent value.

Are fixed assets not used for business activities deductible expenses in Vietnam?

According to Article 6 of Circular 78/2014/TT-BTC (as amended by Article 4 of Circular 96/2015/TT-BTC), the regulation is as follows:

Expenses that are deductible and non-deductible when determining taxable income

...

- Non-deductible expenses when determining taxable income include:

...

2.2. Depreciation expenses for fixed assets falling into one of the following cases:

a) Depreciation expenses for fixed assets not used for production and business activities of goods or services.

Fixed assets serving employees at the enterprise such as: shift rest houses, shift canteens, changing rooms, restrooms, medical rooms or stations for medical examination and treatment, training centers, libraries, kindergartens, sports zones and adequate equipment, furniture eligible as fixed assets installed in the aforementioned facilities; clean water reservoirs, parking facilities; vehicles for transporting employees, direct housing for employees; costs for constructing infrastructure facilities, and costs for purchasing machines and equipment being fixed assets used for organizing vocational education activities are deducted from expenses when determining taxable income.

b) Depreciation expenses for fixed assets without documentation proving the enterprise's ownership (except for financial lease purchased fixed assets).

c) Depreciation expenses for fixed assets not managed, tracked, accounted for in the accounting books of the enterprise according to the current fixed asset management and accounting policies.

Therefore, if an enterprise possesses fixed assets not used for production or business activities, they will not be allowed to deduct corporate income tax.