What is the Certification form of annual income in Vietnam? What are the regulations on personal exemption in Vietnam?

What is the Certification form of annual income in Vietnam?

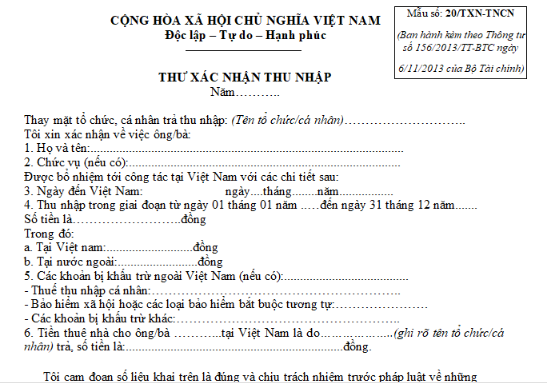

Based on the template issued together with Circular 156/2013/TT-BTC, the Certification form of annual income is form 20/TXN-TNCN.

However, Circular 156/2013/TT-BTC is no longer in effect, and there are currently no new regulations regarding a replacement Certification of annual income for the old form.

Refer to the Certification of annual income sample below:

>>> Download Certification of annual income Sample.

What is the Certification form of annual income in Vietnam? What are regulations on personal exemption in Vietnam? (Image from the Internet)

What are the regulations on personal exemption in Vietnam?

According to Article 1 Resolution 954/2020/UBTVQH14, the regulations are as follows:

personal exemption

To adjust the personal exemption as stipulated in Clause 1, Article 19 of the Law on Personal Income Tax No. 04/2007/QH12, amended and supplemented by Law No. 26/2012/QH13 as follows:

1. The deduction for the taxpayer is 11 million VND/month (132 million VND/year);

2. The deduction for each dependant is 4.4 million VND/month.

Thus, the personal exemption will have 2 levels as follows:

Level 1. The deduction for the taxpayer is 11 million VND/month (132 million VND/year);

Level 2. The deduction for each dependant is 4.4 million VND/month.

Additionally, to qualify as a dependant, certain conditions must be met according to points đ, e, Clause 1, Article 9 Circular 111/2013/TT-BTC, the individual must meet the following conditions:

- For individuals of working age, they must simultaneously meet the following conditions:

+ Be disabled, unable to work.

A disabled person unable to work is one covered under the laws on disabled persons and individuals with incurable illness preventing work (such as AIDS, cancer, chronic kidney failure, etc.).

+ Have no income or an average monthly income in the year from all sources not exceeding 1,000,000 VND.

- For individuals outside working age, they must have no income or an average monthly income in the year from all sources not exceeding 1,000,000 VND.

Additionally, the dependant deduction file will be executed according to sub-item 3, Section 3 of Official Dispatch 883/TCT-DNNCN 2022 from the General Department of Taxation guiding personal income tax finalization, including the following for the taxpayer's dependant deduction profiles:

- For individuals registering dependants directly at the tax authority:

+ dependant registration form as per form No. 07/DK-NPT-TNCN attached in Appendix 2 of Circular 80/2021/TT-BTC.

+ Documents proving dependency according to guidance at point g, Clause 1, Article 9, Circular 111/2013/TT-BTC.

+ In case the taxpayer directly supports the dependant, the municipal/ward People's Committee where the dependant resides must certify per form No. 07/XN-NPT-TNCN attached in Appendix 2 of Circular 80/2021/TT-BTC.

- For individuals registering personal exemptions through an organization or individual paying income, the dependant registration file for submission follows guidance at point a, sub-item 3, Section 3 of Official Dispatch 883/TCT-DNNCN 2022 submitted to the income-paying organization/individual. The income-paying organization/individual compiles according to the Appendix for consolidated registration for dependants for personal exemption form No. 07/THĐK-NPT-TNCN attached in Appendix 2 of Circular 80/2021/TT-BTC and submits it to tax authorities as prescribed.

How to determine dependants for personal exemption in Vietnam?

Based on Clause 3, Article 19 of the Law on Personal Income Tax 2007, a dependant is an individual whom the taxpayer has an obligation to support, including:

- Minor children; children with disabilities, unable to work;

- Individuals with no income or income not exceeding the regulated limit, including adult children studying at university, college, technical secondary school, or vocational training; incapable spouse; parents who are either beyond working age or incapable of working; other individuals without a refuge whom the taxpayer must directly support.

In addition, according to point d, Clause 1, Article 9 Circular 111/2013/TT-BTC, the dependants include:

[1] Children: biological children, legally adopted children, stepchildren, illegitimate children, wife's own children, husband's own children, specifically including:

- Children under 18 years of age (calculated by completed months).

- Children aged 18 and over who are disabled and unable to work.

- Children studying in Vietnam or abroad at the university, college, vocational, or technical secondary levels, including those over 18 studying in high school (including the period from June to September of the 12th-grade year pending university admission results) without income or an average monthly income in the year from all income sources not exceeding 1,000,000 VND.

[2] Spouse of the taxpayer

The spouse of the taxpayer is considered a dependant if meeting the conditions in section 3.

[3] Biological parents, in-laws (or parents of the spouse); step-parents; adoptive parents of the taxpayer must meet the conditions in section 3.

[4] Other individuals without a place of refuge that the taxpayer is directly supporting and meeting the conditions in section 3, including:

- Siblings of the taxpayer.

- Paternal grandparents; maternal grandparents; aunts, uncles, bio-siblings of the taxpayer.

- Nephews/nieces of the taxpayer including: children of siblings.

- Other individuals who require direct care according to regulatory authority.