What is the application form for TIN reactivation in Vietnam from February 6, 2025?

What is the application form for TIN reactivation in Vietnam from February 6, 2025?

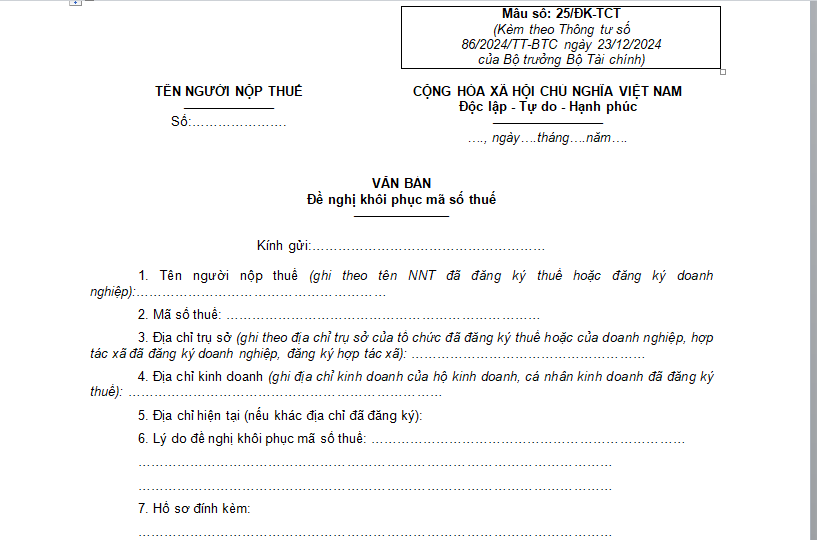

The application form for TIN reactivation applicable from February 6, 2025, is form 25/DK-TCT, as stipulated in Appendix 2 issued with Circular 86/2024/TT-BTC. The 25/DK-TCT form for requesting the TIN reactivation is as follows:

>>Download the 25/DK-TCT form for requesting the TIN reactivation applicable from February 6, 2025 here

What is the application form for TIN reactivation in Vietnam from February 6, 2025? (Image from the Internet)

What does the application for TIN reactivation for household businesses in Vietnam include from February 6, 2025, include?

Based on Article 33 of Circular 86/2024/TT-BTC (effective from February 6, 2025), the application for TIN reactivation for household businesses is regulated as follows:

- The application for TIN reactivation for household businesses taxpayer registration, along with business registration when their legal status is restored, comprises the information on the restoration of the legal status of household businesses sent by the business registration authority to the tax authority through the National Business Registration Information System.

+ In case household businesses are announced by the tax authority as not operating at the registered address, the tax authority updates the reason for status 06. After receiving the application requesting reactivation of the TIN for the business household, which is the written request for TIN reactivation form 25/DK-TCT issued with Circular 86/2024/TT-BTC, it must be submitted to the directly managing tax authority before the tax authority issues a Notice on terminating the validity of the TIN as regulated in points b, d clause 1 Article 19 of Circular 86/2024/TT-BTC.

- The application for TIN reactivation for household businesses taxpayer registration through the inter-agency one-stop mechanism after the tax authority announces non-operation at the registered address but has not revoked the Business Registration Certificate and the TIN validity has not been terminated. The submitted application includes a written request for reactivation form 25/DK-TCT issued with Circular 86/2024/TT-BTC, submitted to the directly managing tax authority before the tax authority issues a Notice on terminating the validity of the TIN as regulated.

- The application for TIN reactivation for individuals whose TIN validity has been terminated due to death, disappearance, or loss of civil act capacity includes a Court Decision to annul the Decision declaring the individual dead, missing, or losing legal capacity.

What are regulations on the processing of the application for TIN reactivation and returning the results in Vietnam from February 6, 2025?

Based on Article 34 of Circular 86/2024/TT-BTC (effective from February 6, 2025), the processing of the application for TIN reactivation and returning the results is regulated as follows:

(1) Processing the application for TIN reactivation for household businesses taxpayer registration along with business registration:

- When the tax authority receives transactions on the restoration of legal status for household businesses according to the Government of Vietnam's regulations on household businesses sent through the National Business Registration Information System, the tax authority reactivates the TIN for the taxpayer on the day the information is received in the taxpayer registration application system.

- In case household businesses are announced by the tax authority as not operating at the registered address, the tax authority updates the reason for status 06. After receiving the application requesting reactivation of the TIN for the business household, which is the written request for TIN reactivation form 25/DK-TCT issued with Circular 86/2024/TT-BTC, it must be submitted to the directly managing tax authority before the tax authority issues a Notice on terminating the validity of the TIN as regulated in points b, d clause 1 Article 19 of Circular 86/2024/TT-BTC.

(2) Processing the application for TIN reactivation for household businesses taxpayer registration through the inter-agency one-stop mechanism after the tax authority announces non-operation at the registered address but has not revoked the Business Registration Certificate and the TIN validity has not been terminated as regulated in points b, d clause 1 Article 19 of Circular 86/2024/TT-BTC.

(3) Processing the application for TIN reactivation for individuals whose TIN validity has been terminated due to death, disappearance, or loss of civil act capacity includes a Court Decision to annul the Decision declaring the individual dead, missing, or losing legal capacity:

When the tax authority receives a Court Decision to annul the Decision declaring the individual dead, missing, or losing legal capacity, the tax authority reactivates the TIN for the individual in the taxpayer registration application system within 03 (three) working days from receiving the Court decision.