What is the application form for tax registration for dependants in Vietnam according to Form 20-DK-TCT?

Application form for tax registration for dependants According to Form 20-DK-TCT?

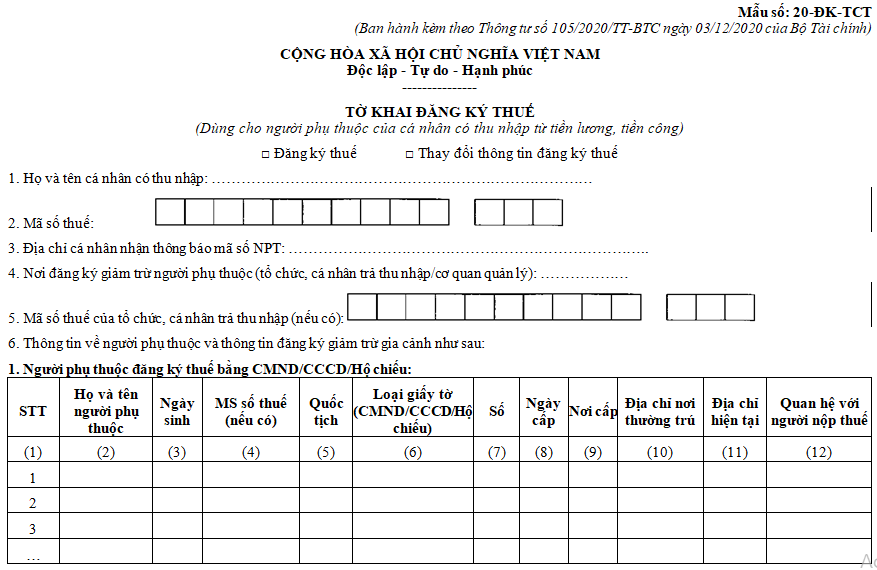

The application form for tax registration for dependant as stipulated in Form 20-DK-TCT is issued in conjunction with Circular 105/2020/TT-BTC.

Download the application form for tax registration for dependant according to Form 20-DK-TCT here.

What is the application form for tax registration for dependants in Vietnam according to Form 20-DK-TCT? (Image from the Internet)

Vietnam: What do the documents proving dependants include?

Based on the provisions at Point g, Clause 1, Article 9 of Circular 111/2013/TT-BTC as amended by Article 1 Circular 79/2022/TT-BTC, the documents proving dependants include:

(1) For children:

Under 18 years, the dossier includes:

- A photocopy of the Birth Certificate and a photocopy of the ID Card or Citizenship Card (if any).

Above 18 years with disabilities and unable to work, the dossier includes:

- A photocopy of the Birth Certificate and a photocopy of the ID Card or Citizenship Card (if any).

- A photocopy of the Disability Certificate according to the legal regulations on persons with disabilities.

- Children studying at all educational levels in Vietnam or abroad at universities, colleges, vocational schools, including children over 18 years still attending high school (including the period waiting for university exam results from June to September of 12th grade), without income or with an average monthly income from all sources not exceeding 1,000,000 VND, the dossier includes:

+ A photocopy of the Birth Certificate.

+ A photocopy of a Student Card or a self-declaration confirmed by the school or other documents proving attendance at a university, college, professional secondary school, high school, or vocational school.

- In case of an adopted child, an illegitimate child, or a stepchild, besides the documents mentioned, the dossier needs additional documents proving the relationship such as a photocopy of the decision recognizing the adoption, decision recognizing paternity, maternity, or child recognition by a competent authority.

(2) For spouse, the dossier includes:

- A photocopy of the ID Card or Citizenship Card.

- A photocopy of the Residence Information Confirmation or Notification of Personal Identifier and information in the National Database on Population or other documents proving the marital relationship issued by authorities or a photocopy of the Marriage Certificate.

In case the spouse is of working age, besides the mentioned documents, the dossier needs additional documents proving the dependant's inability to work such as a photocopy of the Disability Certificate according to the legal regulations on persons with disabilities, or a photocopy of medical records in case of individuals suffering from diseases rendering them unable to work (like AIDS, cancer, chronic kidney failure, etc.).

(3) For biological parents, parents-in-law, stepparents, legal adoptive parents, the dossier includes:

- A photocopy of the ID Card or Citizenship Card.

- Legal documents to determine the dependant relationship with the taxpayer such as a photocopy of the Residence Information Confirmation or Notification of Personal Identifier and information in the National Database on Population or other documents issued by authorities, birth certificate, decision recognizing paternity, maternity, or child recognition by a competent authority.

In case of working age, besides the mentioned documents, the dossier needs additional documents proving disability and inability to work such as a photocopy of the Disability Certificate according to legal regulations on persons with disabilities, or a photocopy of medical records for individuals suffering from diseases rendering them unable to work (like AIDS, cancer, chronic kidney failure, etc.).

(4) For other individuals as guided in section d.4, Point d, Clause 1, this Article, the dossier includes:

- A photocopy of the ID Card, Citizenship Card, or Birth Certificate.

- Legal documents to determine maintenance responsibility according to legal regulations.

In case the dependant is of working age, besides the mentioned documents, the dossier needs additional documents proving inability to work such as a photocopy of the Disability Certificate according to legal regulations on persons with disabilities, or a photocopy of medical records for individuals suffering from diseases rendering them unable to work (like AIDS, cancer, chronic kidney failure, etc.).

Legal documents at section g.4.2, Point g, Clause 1, this Article is any legal document that determines the relationship of the taxpayer with the dependant, such as:

- A photocopy of the document determining the maintenance obligation according to legal regulations (if any).

- A photocopy of the Residence Information Confirmation or Notification of Personal Identifier and information in the National Database on Population or other documents issued by authorities.

- A self-declaration by the taxpayer according to the form issued with Circular 80/2021/TT-BTC and Decree 126/2020/ND-CP dated October 19, 2020, of the Government of Vietnam detailing some articles of the Law on Tax Administration, confirmed by the People's Committee of the commune where the taxpayer resides that the dependant is living together.

- A self-declaration by the taxpayer according to the form issued with Circular 80/2021/TT-BTC and Decree 126/2020/ND-CP dated October 19, 2020, of the Government of Vietnam detailing some articles of the Law on Tax Administration, confirmed by the People's Committee of the commune where the dependant is residing that the dependant is currently residing in the locality and has no one to maintain them (if not living together).

(5) In case of a foreign resident individual, if there is no dossier as instructed for specific cases mentioned above, similar legal documents must be provided to serve as a basis for proving dependants.

(6) For taxpayers working in economic organizations, administrative, and public service agencies who have parents, spouse, children, and others eligible to be considered as dependants clearly declared in the taxpayer's CV, the dependant proof dossier is done according to the guidance in (1), (2), (3), (4), (5) or only requires the dependant Registration Form issued with Circular 80/2021/TT-BTC confirmed by the head of the unit on the left side of the form.

The head of the unit is only responsible for the following contents: name of the dependant, year of birth, and their relationship with the taxpayer; other contents are self-declared by the taxpayer, who is responsible for them.

(7) From the date the tax authority announces the completion of data connection with the National Database on Population, taxpayers are not required to submit the above-mentioned documents proving dependants if the information in those documents is already in the National Database on Population.

What is the current personal exemption rate in Vietnam?

The current personal exemption is adjusted by Article 1 of Resolution 954/2020/UBTVQH14 as follows:

Personal exemption

Adjustment of the personal exemption stipulated at Clause 1, Article 19 of the Law on Personal Income Tax No. 04/2007/QH12, as amended and supplemented by Law No. 26/2012/QH13, is as follows:

- The deduction for the taxpayer is 11 million VND/month (132 million VND/year);

- The deduction for each dependant is 4.4 million VND/month.

Thus, the current personal exemption is as follows:

- For the taxpayer: 11 million VND/month (132 million VND/year);

- For each dependant: 4.4 million VND/month.