What is the application form for tax incentive program for automobile supporting industry in Vietnam?

What is the application form for tax incentive program for automobile supporting industry in Vietnam?

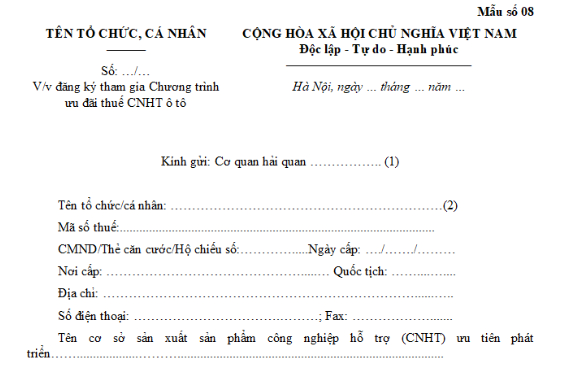

The application form for tax incentive program for automobile supporting industry follows the Form No. 08 in Appendix 2 issued along with Decree 26/2023/ND-CP as follows:

>> Download the application form for tax incentive program for automobile supporting industry as per Form No. 08

What is the application form for tax incentive program for automobile supporting industry in Vietnam? (Image from the Internet)

What are the requirements for imported materials, supplies, and components participating in the 2024 tax incentive program for automobile supporting industry in Vietnam?

Based on Clause 3, Article 9 of Decree 26/2023/ND-CP, imported materials, supplies, and components must meet the following conditions when participating in the 2024 tax incentive program for automobile supporting industry:

- Imported materials, supplies, and components (including materials, supplies, and components already imported since the effective date of this Decree but remaining in stock from previous incentive periods transferred to subsequent incentive periods for the production and assembly of automotive supporting products; excluding imported materials, supplies, and components used but defective) used for the production, processing, and assembly of automotive supporting products named in the List of prioritized supporting industrial products for the automotive industry stipulated in Section 4, Appendix issued with Decree No. 111/2015/ND-CP on the development of supporting industries and its amendments, if any.

If the products are merely assembled with simple devices like screws, bolts, nuts, or rivets without going through any production or processing to become finished products, they are not eligible for the tax incentive program for automobile supporting industry.

- Imported materials, supplies, and components not yet produced domestically as specified by the enterprises mentioned in Clause 2, Article 9 of Decree 26/2023/ND-CP are to be directly imported or imported under consignment or authorization. The determination of domestic non-production of materials, supplies, and components is based on the regulations of the Ministry of Planning and Investment on the List of domestically produced materials, supplies, and semi-finished products.

Enterprises stipulated in Clause 2, Article 9 of Decree 26/2023/ND-CP that meet the regulations in points a, b, c of this clause and the regulations in clauses 4, 5, 6, 7, 8, Article 9 of Decree 26/2023/ND-CP are eligible for a preferential import tax rate of 0% on imported materials, supplies, and components for the production and processing (assembly) of automotive supporting industry products during the incentive period.

What are registration procedures to participate in the 2024 tax incentive program for automobile supporting industry in Vietnam?

Based on Clause 5, Article 9 of Decree 26/2023/ND-CP as follows:

Preferential import tax rates for materials, supplies, and components used for the production, processing (assembly) of prioritized supporting industry products for the automotive manufacturing and assembly sector until December 31, 2024 (referred to as the tax incentive program for automobile supporting industry)

...

5. Dossiers and procedures for registering for the tax incentive program for automobile supporting industry

a) The application dossier for participation in the tax incentive program for automobile supporting industry includes:

a.1) application form for tax incentive program for automobile supporting industry according to Form No. 08 in Appendix II issued with this Decree: 01 original copy;

a.2) Investment certificate or Investment registration certificate or Enterprise registration certificate or Business registration certificate (applicable for cases stipulated in point a, clause 2 of this Article): 01 certified copy;

a.3) Notification document on the production and processing (assembly) facilities; machinery and equipment at the production and processing (assembly) facility to the customs authority according to Form No. 09 in Appendix II issued with this Decree (applicable for cases stipulated in point a, clause 2 of this Article): 01 original copy. Land use rights certificate issued by the competent authority to the enterprise or land use rights certificate issued by the competent authority to the landowner and the land lease, loan contract, or factory lease in case of rented or borrowed land for production use: 01 certified copy;

a.4) Certificate of eligibility to produce and assemble automobiles issued by the Ministry of Industry and Trade (applicable for cases stipulated in point b, clause 2 of this Article): 01 certified copy.

b) Registration procedures for the tax incentive program for automobile supporting industry

Enterprises submit the application dossier to register for the tax incentive program for automobile supporting industry directly or via the electronic data system of the customs authority or by post to the customs authority where the enterprise is headquartered or where the production and processing (assembly) facility is located to register for participation immediately after this Decree comes into effect or at any time during the year. The participation date commences from the date of the registration letter for the tax incentive program for automobile supporting industry.

...

Thus, the registration procedure for the 2024 tax incentive program for automobile supporting industry can be carried out by submitting the application directly, via the customs authority's electronic data system, or by post to the customs authority where the enterprise is headquartered or where the production and processing (assembly) facility is located.