What are the regulations on the declaration and finalization of severance tax on mineral extraction in Vietnam?

What are the regulations on the declaration and finalization of severance tax on mineral extraction in Vietnam?

According to Article 9 of Circular 152/2015/TT-BTC, the declaration and finalization of severance tax on mineral extraction in Vietnam are stipulated as follows:

- Organizations and business households extracting natural resources shall send a notification to tax authorities of their methods of determining taxable prices of each type of resource extracted together with the declaration of severance tax of the first month in which natural resources are extracted. If the method is changed, the supervisory tax authority must be notified within the month in which the change is made.

- Taxpayers shall make monthly declaration of tax on the entire extraction quantity in the month (regardless of quantity in stock and undergoing processing).

- When making the annual/terminal declaration, the taxpayer must enclose a list of specific extraction quantities in the year at each mine with the declaration. Severance tax depends on the tax rate, extraction quantity, and taxable price. To be specific:

+ Taxable extraction quantity is the total quantity of natural resources extracted in the year, regardless of quantity in stock and undergoing processing.

If the sale quantity includes both natural resource-derived products and industrial products, the quantity of resources in natural resource-derived products and industrial products must be converted into extraction quantity according to the norms for use of natural resources determined by taxpayers themselves.

+ Taxable price is the average selling price of a unit of natural resource-derived products, which equals (=) total revenue from the sale of resources divided by (:) quantity of resources sold in the year.

What are the regulations on the declaration and finalization of severance tax on mineral extraction in Vietnam? (Image from the Internet)

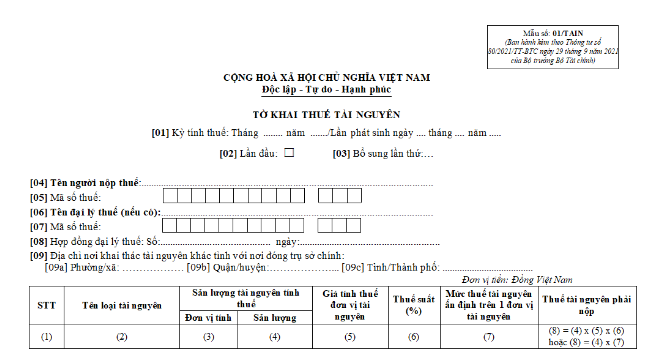

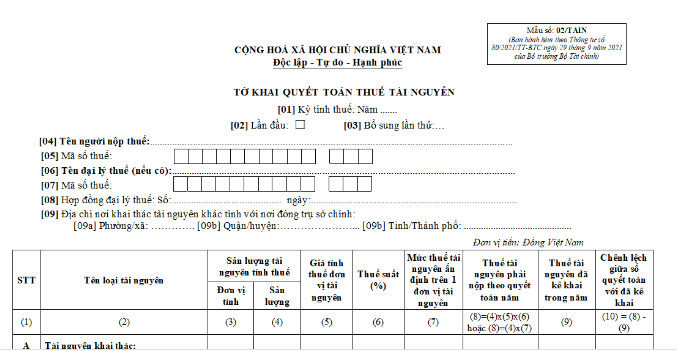

What are the newest severance tax declaration and severance tax finalization declaration forms in Vietnam?

The newest severance tax declaration and severance tax finalization declaration forms in Vietnam are Form 01/TAIN and Form 02/TAIN-VSP as stipulated in Appendix 2 issued together with Circular 80/2021/TT-BTC.

Download severance tax declaration form: Download

Download severance tax finalization declaration form: Download

What are the applicable severance tax rates in 2024 in Vietnam?

According to Article 7 of the severance tax Law 2009, the severance tax rates are stipulated as follows:

- The frame severance tax tariff is specified below:

|

No. |

Group or category of natural resource |

Severance tax rate (%) |

|

I |

Metallic minerals |

|

|

1 |

Iron and manganese |

7-20 |

|

2 |

Titan |

7-20 |

|

3 |

Gold |

9-25 |

|

4 |

Rare earths |

12-25 |

|

5 |

Platinum, silver and tin |

7-25 |

|

6 |

Wolfram and antimony |

7-25 |

|

7 |

Lead, zinc, aluminum, bauxite, copper and nickel |

7-25 |

|

8 |

Cobalt, molybdenum, mercury, magnesium and vanadium |

7-25 |

|

9 |

Other metallic minerals |

5-25 |

|

II |

Non-metallic minerals |

|

|

1 |

Soil exploited for ground leveling and work construction |

3-10 |

|

2 |

Rock, except rock used for lime baking and cement production; gravel; sand, except sand used for glass-making |

5-15 |

|

3 |

Soil used for brick-making |

5-15 |

|

4 |

Granite and refractory clay |

7-20 |

|

5 |

Dolomite and quartzite |

7-20 |

|

6 |

Kaolin, mica, technical quartz, and sand used for glass-making |

7-15 |

|

7 |

Pyrite, phosphorite, and stone for lime baking and cement production |

5-15 |

|

8 |

Apatite and serpentine |

3-10 |

|

9 |

Pit anthracite coal |

4-20 |

|

10 |

Open-cast anthracite coal |

6-20 |

|

11 |

Lignite and fat coal |

6-20 |

|

12 |

Other coals |

4-20 |

|

13 |

Diamond, ruby and sapphire |

16-30 |

|

14 |

Emerald, alexandrite and black precious opal |

16-30 |

|

15 |

Adrite, rodolite, pyrope, berine. Spinel and topaz |

12-25 |

|

16 |

Bluish-purple, greenish-yellow or orange crystalline quartz; chrysolite; white or scarlet precious opal; feldspar; birusa; and nephrite |

12-25 |

|

17 |

Other non-metallic minerals |

4-25 |

|

III |

Crude oil |

6-40 |

|

IV |

Natural gas and coal gas |

1-30 |

|

V |

Natural forest products |

|

|

1 |

Timber of group I |

25-35 |

|

2 |

Timber of group II |

20-30 |

|

3 |

Timber of groups III and IV |

15-20 |

|

4 |

Timber of groups V, VI, VII and VIII and of other categories |

10-15 |

|

5 |

Tree branches, tops, stumps and roots |

10-20 |

|

6 |

Firewood |

1-5 |

|

7 |

Bamboo of all kinds |

10-15 |

|

8 |

Sandalwood and calambac |

25-30 |

|

9 |

Anise, cinnamon, cardamom and liquorice |

10-15 |

|

10 |

Other natural forest products |

5-15 |

|

|

Natural aquatic resources |

|

|

1 |

Pearl, abalone and sea-cucumber |

6-10 |

|

2 |

Other natural aquatic resources |

1-5 |

|

VII |

Natural water |

|

|

1 |

Natural mineral water, natural thermal water and refined natural water, bottled or tinned |

8-10 |

|

2 |

Natural water used for hydropower generation |

2-5 |

|

3 |

Natural water used for production and business activities, except water mentioned at Points 1 and 2 of this group |

|

|

3.1 |

.Surface water |

1-3 |

|

3.2 |

Groundwater |

3-8 |

|

VIII |

Natural swallow's nests |

10-20 |

|

IX |

Other resources |

1-20 |

- Specific severance tax rates for crude oil. natural gas and coal gas shall be determined as partially progressive based on their daily exploited average output.

- Under Clauses 1 and 2 of Article 7 of the severance tax Law 2009, the National Assembly Standing Committee shall stipulate specific severance tax rates for each category of natural resource in each period on the following principles:

+ Ensuring conformity with the list of groups and categories of natural resource and within the severance tax rate bracket prescribed by the National Assembly:

+ Contributing to the state management of natural resources; protection, exploitation and rational, economical and effective use of natural resources:

+ Contributing to assuring state budget revenues and market stabilization.