What are prohibited acts in VAT deduction and refund in Vietnam according to the Law on VAT 2024?

What are prohibited acts in VAT deduction and refund in Vietnam according to the Law on VAT 2024?

Pursuant to Article 13 of the Law on VAT 2024, which comes into effect on July 1, 2024, the prohibited acts in VAT deduction and refund include the following 8 groups of behaviors:

- Purchasing, giving, selling, advertising, brokering the purchase and sale of invoices.

- Creating false transactions involving the purchase, sale of goods, provision of services, or transactions that are not legally conformable.

- Issuing invoices for selling goods, providing services during business suspension, except for issuing invoices to customers for contracts signed before the suspension notice date.

- Using illegal invoices and documents or illegally using invoices and documents according to the regulations of the Government of Vietnam.

- Failing to transfer electronic invoice data to the tax authorities as required.

- Tampering with, misusing, unauthorized access, or destruction of information systems related to invoices and documents.

- Giving, receiving, or brokering bribes or undertaking other acts related to invoices and documents to qualify for tax deduction, refund, tax theft, or evasion of VAT.

- Colluding, covering up, or establishing connections between tax officials, tax authorities, and businesses or importers, and among these parties for illegal use of invoices and documents to obtain tax deductions, refunds, or tax theft, or evasion of VAT.

What are prohibited acts in VAT deduction and refund in Vietnam according to the Law on VAT 2024? (Image from the Internet)

Vietnam: What does the VAT refund claim include?

Based on the provisions in Article 28 of Circular 80/2021/TT-BTC (amended by Article 2 of Circular 13/2023/TT-BTC), a VAT refund application dossier includes:

(1) A request form for returning state budget receipts as per form No. 01/HT issued with appendix 1 of Circular 80/2021/TT-BTC.

(2) Relevant documents according to the refund case. To be specific:

- For Investment Project Refund:

+ A copy of the Investment Registration Certificate or Investment Certificate or Investment License for cases requiring procedures for issuing investment registration certificates;

+ For projects involving construction: A copy of the land use rights certificate or the land allocation decision or lease contract from competent authorities; construction permit;

+ A copy of the capital contribution certificate;

+ For investment projects of businesses in conditional business lines during the investment phase, as regulated by investment and sector-specific laws, licensed by competent authorities for conditional business lines as stipulated at clause 3 Article 1 of Decree 49/2022/ND-CP: A copy of one of the following: license, certificate, or document of confirmation, approval for the investment business line.

+ Invoice and proof list of goods and services purchased according to form No. 01-1/HT issued with appendix 1 of this Circular, except where the taxpayer has submitted electronic invoices to the tax authorities;

+ The project management board establishment decision, investment project management assignment decision of the project owner, organizational and operational regulations of the branch or project management board (if the branch or management board handles the refund).

- For Goods and Services Export Refund:

+ Invoice and proof list of goods and services purchased according to form No. 01-1/HT issued with appendix 1 of Circular 80/2021/TT-BTC, except where the taxpayer has already sent electronic invoices to the tax authorities;

+ The customs declaration list of cleared export goods as per form No. 01-2/HT issued with appendix I of Circular 80/2021/TT-BTC for goods exported and cleared as per the customs law.

- For Programs, Projects Using Non-Refundable Official Development Assistance (ODA) Funds:

+ In case non-refundable ODA funds are directly managed and implemented by the program/project owner:

++ A copy of the international treaty or non-refundable ODA agreement or exchange document on commitment and receipt of non-refundable ODA funds; a copy of the Decision approving the project document or program investment decision and the project document or feasibility study report approved.

++ A request for confirmation of legal expenditure of non-productive capital for non-productive expenses and investment capital payment for project investment from the project owner as regulated.

++ Invoice and proof list of purchased goods/services according to form No. 01-1/HT issued with appendix I of this Circular.

++ A copy of the document confirming from the managing agency of the ODA program/project for the program/project owner regarding the provision form as non-refundable ODA eligible for VAT refund and not receiving counterpart funds from the state budget for VAT payment.

++ In case the program/project owner delegates part or the entire program/project to other units or organizations for management and implementation according to legal regulations on managing and using non-refundable ODA which hasn't been detailed in the documents specified in c.1.1, c.1.4 clause 2 Article 28 of Circular 80/2021/TT-BTC, besides documents according to points c.1.1, c.1.2, c.1.3, c.1.4 clause 2 Article 28 of Circular 80/2021/TT-BTC, there must be an additional copy of the document on the delegation of program/project management and implementation by the program/project owner for the unit/organization requesting refund.

++ If the main contractor files for tax refund, besides documents stipulated in c.1.1, c.1.2, c.1.3, c.1.4 clause 2 Article 28 of Circular 80/2021/TT-BTC, there must also be a copy of the contract between the project owner and the main contractor specifying a payment price excluding VAT.

Taxpayers only need to submit the documents specified at c.1.1, c.1.4, c.1.5, c.1.6 clause 2 Article 28 of Circular 80/2021/TT-BTC for the initial refund application or when amendments or supplements are made.

+ In case non-refundable ODA funds are directly managed and implemented by the donor:

++ Documents as per point c.1.1, c.1.3 clause 2 Article 28 of Circular 80/2021/TT-BTC;

++ If the donor appoints a Representative Office or an organization to manage and implement the program/project (except as stipulated at point c.2.3 clause 2 Article 28 of Circular 80/2021/TT-BTC) but this is not detailed in documents specified at point c.1.1 clause 2 Article 28 of Circular 80/2021/TT-BTC, then additional documents must be:

+++ A copy of the document delegating the management and implementation of a non-refundable ODA program/project from the donor to the appointed Representative Office or organization.

+++ A copy of the document from a competent agency on the establishment of the donor's Representative Office or the appointed organization.

++ If the main contractor files for tax refund, besides documents stipulated at point c.2.1 clause 2 Article 28 of Circular 80/2021/TT-BTC, there must be a copy of the contract between the donor and the main contractor, or a summary contract certified by the donor including details such as contract number, signing date, contract duration, scope, contract value, payment method, payment value excluding VAT.

Taxpayers only need to submit documents specified at point c.1.1, c.2.2, c.2.3 clause 2 Article 28 of Circular 80/2021/TT-BTC for the initial refund application or when amendments or supplements occur.

- For Domestic Goods and Services Purchase with Non-Refundable Aid not under ODA:

+ A copy of the Decision approving the program, project document, non-project aid, and program, project, non-project document as stipulated in point a clause 2 Article 24 of Decree 80/2020/ND-CP;

+ A request for valid expenditures confirmation of non-productive capital for non-productive expenses and investment capital payment from the project owner (in case of receiving non-refundable aid from the state budget) according to point b clause 2 Article 24 of Decree 80/2020/ND-CP and point a clause 10 Article 10 of Decree 11/2020/ND-CP.

+ Invoice and proof list of goods/service purchases according to form No. 01-1/HT issued with appendix I of Circular 80/2021/TT-BTC.

Taxpayers only need to submit the documents specified at point d.1 of this clause for the initial refund application or when amendments or supplements occur.

- For Domestic Goods and Services Purchase with Emergency International Aid for Disaster Relief and Recovery in Vietnam:

+ A copy of the Decision on acceptance of emergency aid for relief (in case of emergency aid for relief) or the Decision on policy for receiving emergency international aid for disaster recovery and the emergency aid document for disaster recovery as per regulations.

+ Invoice and proof list of purchased goods/services according to form No. 01-1/HT issued with appendix I of Circular 80/2021/TT-BTC.

Taxpayers only need to submit the documents specified at point đ.1 of this clause for the initial refund application or when amendments or supplements occur.

- For Diplomatic Immunity Tax Refunds:

+ A VAT listing for goods and services purchased for diplomatic missions according to form No. 01-3a/HT issued with appendix I of Circular 80/2021/TT-BTC confirmed by the State Protocol Department of the Ministry of Foreign Affairs, verifying input costs eligible for diplomatic immunity for tax refunds.

+ A public employee listing for diplomatic employees eligible for VAT refund according to form No. 01-3b/HT issued with appendix I of Circular 80/2021/TT-BTC.

- For Commercial Banks Acting as VAT Refund Agents for Departing Foreign Guests:

Invoice proof listing for VAT refund to foreigners exiting according to form No. 01-4/HT issued with appendix I of Circular 80/2021/TT-BTC.

- VAT Refund upon the Decision of Competent Authorities as per Legal Regulations: Competent authorities' decision.

Note: VAT refund as per international treaties; residual input VAT not deducted in ownership transfer, business conversion, merger, consolidation, division, separation, dissolution, bankruptcy, termination of operations is conducted under provisions of Articles 30 and 31 of Circular 80/2021/TT-BTC.

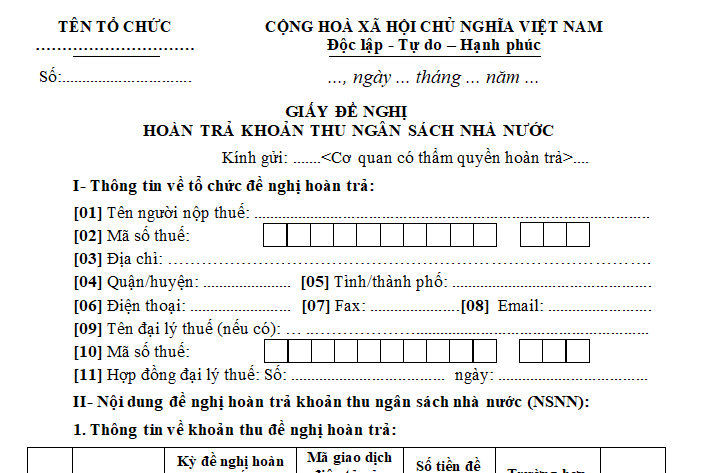

Which form is used for VAT refund claim in Vietnam according to Circular 80?

Form No. 01/HT issued with appendix I of Circular 80/2021/TT-BTC is as follows:

Download the 01/HT form for VAT refund claim here.