What are instructions for completing the tax declaration for fixed tax payers changing tax calculation methods in Vietnam (Form 01/CNKD)?

May the household business paying fixed tax change methods of tax calculation in Vietnam?

Pursuant to the provisions at point c, clause 3, Article 13 of Circular 40/2021/TT-BTC as follows:

Tax management for fixed tax payers

...

3. Deadline for submitting tax returns

The deadline for submitting tax returns for fixed tax payers is stipulated at point c, clause 2, clause 3 of Article 44 of the Law on Tax Administration. Specifically:

...

b) In cases where a fixed tax household starts a new business (including households converting to the fixed method), or fixed tax household converts to the declaration method*, or the industry changes, or scale changes occur within the year, the deadline to submit the tax return is no later than the 10th day from the start of operations, conversion of tax calculation method, change of industry, or change of business scale.*

...

And at point b.6, clause 4, Article 13 of Circular 40/2021/TT-BTC it is stipulated:

Tax management for fixed tax payers

...

4. Determination of revenue and fixed tax rate

...

b) Adjusting revenue and fixed tax rate

If a fixed tax household requests an adjustment in revenue or fixed tax rate due to a change in business activities, the tax authority will adjust the fixed tax rate according to clause 3 of Article 51 of the Law on Tax Administration from the time the change occurs. Specifically, as follows:

...

b.6) Fixed tax household converts to the declaration method then the household must submit an adjusted and supplementary fixed tax declaration using form 01/CNKD issued with this Circular. The tax authority will base adjustments on this declaration to reduce the fixed tax rate during the transition period.

...

Thus, the fixed tax household (a household business paying tax using the fixed method) can change to the declaration method.

When a fixed tax household changees to the declaration method, it must submit an adjusted and supplementary fixed tax declaration form using Form 01/CNKD issued with Circular 40/2021/TT-BTC. The tax authority will adjust the predetermined tax amount based on the adjusted and supplementary declaration for the transition period.

May the household business paying fixed tax change methods of tax calculation in Vietnam? (Image from the Internet)

What are instructions for completing the tax declaration for fixed tax payers changing tax calculation methods in Vietnam (Form 01/CNKD)?

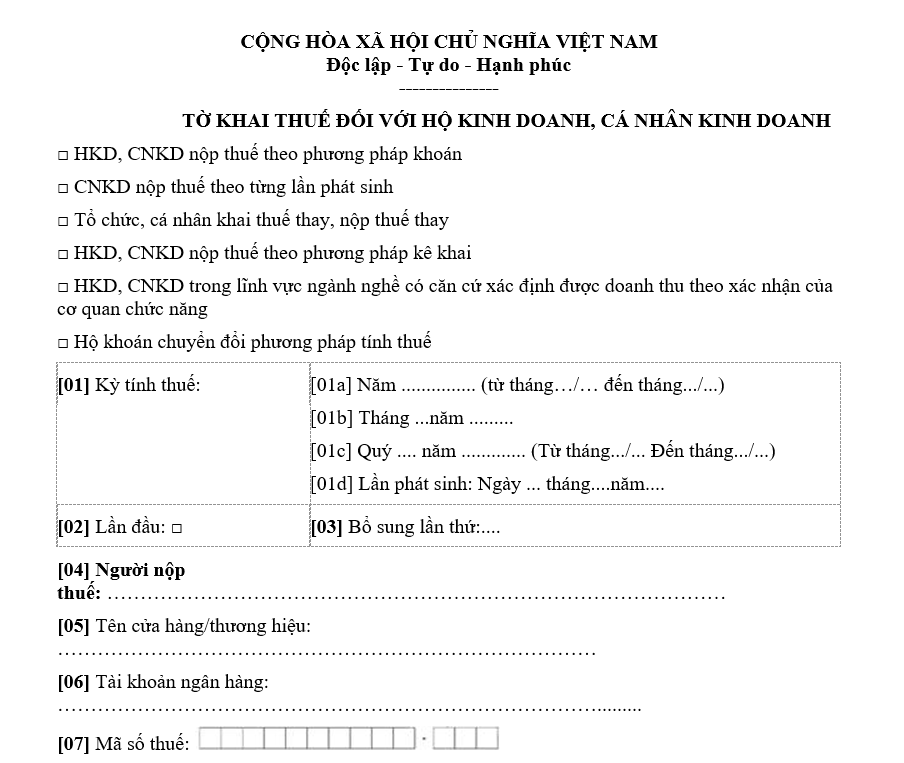

The tax declaration form for fixed tax payers changing to the declaration method is Form 01/CNKD issued with Circular 40/2021/TT-BTC.

Guidance on completing the tax declaration for fixed tax payers changing to the declaration method (Form 01/CNKD) is as follows:

- Mark X in the box "Fixed tax household changing tax calculation methods."

- Indicator [01a] should only be filled out by household businesses paying tax using the fixed method.

- Indicator [08a] should only be marked if the information on indicator [08] differs from the previous declaration.

- Indicator [12a] should only be marked if the information in indicators [12b], [12c], [12d], [12đ] differs from the previous declaration.

- For revenue and output indicators: If it is a fixed tax household, declare the estimated average monthly revenue and output for the year.

- Household businesses operating under a cooperative model with an organization shall have the organization declare on their behalf, accompanying Form 01/CNKD Appendix Detailed List of Household Businesses, and not have to declare indicators from [04] to [18].

DOWNLOAD >>> Tax declaration for fixed tax payers changing tax calculation methods (Form 01/CNKD)

Shall household businesses paying tax by the declaration method settle tax?

The tax method for household businesses paying tax by the declaration method is stipulated in Article 5 of Circular 40/2021/TT-BTC as follows:

Tax calculation method for household businesses and individual businesses paying tax by the declaration method

1. The declaration method applies to large-scale household businesses and individual businesses; and businesses not meeting large-scale criteria but choose to pay tax by the declaration method.

2. Household businesses and individual businesses paying tax by the declaration method must declare taxes monthly, except for new businesses or those meeting criteria for quarterly tax declarations as regulated in Article 9 of Decree 126/2020/ND-CP dated October 19, 2020, by the Government of Vietnam.

3. If household businesses and individual businesses paying tax by the declaration method recognize revenue inconsistencies, the tax authority will determine tax revenue according to Article 50 of the Tax Administration Law.

4. Household businesses and individual businesses paying tax by the declaration method must implement accounting, invoicing, and documentation policies. However, businesses operating in fields that can substantiate revenue through official confirmations are exempt from accounting policies.

5. Household businesses and individual businesses paying tax by the declaration method are not required to settle tax.

Therefore, household businesses paying tax by the declaration method are not required to settle tax.